|

Proprietary Data Insights Financial Pros Top Medical Distribution Stock Searches December

|

|

Stock Analysis |

Cardinal Health Offers A Unique Opportunity |

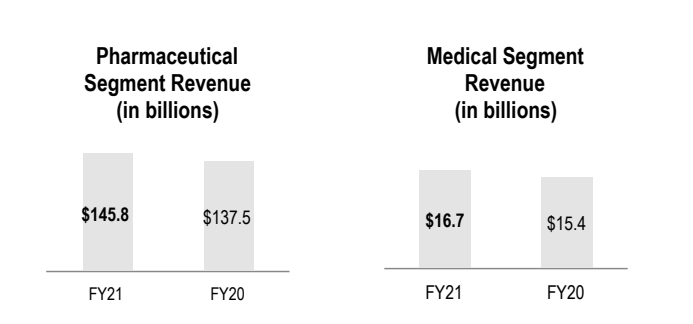

Healthcare is a massive $12 trillion global industry. In the US alone, Americans are expected to spend $8.3 trillion by 2040. Now more than ever, we need better and faster healthcare delivery. Behind the scenes, Cardinal Health (CAH) makes this happen. As a nationwide drug distributor and services provider, Cardinal Health creates the backbone of our healthcare network. Although revenue only grows at around 5% each year, that growth is consistent year to year as is more than $1 billion in cash flow and a healthy dividend. Two things caught our eye. First, share prices are well off their highs for the year but are almost as cheap as they were a decade ago. Second, CAH was the second most searched medical distribution ticker in the last month by financial pros. We know this stock isn’t likely to knock your socks off. However, there is a ton of value here and shares are priced quite nicely. Cardinal Health’s Business Based out of Dublin, Ohio, Cardinal Health is the 3rd largest drug distributor in the U.S. behind AmerisourceBergen and McKesson. The company operates two main segments:

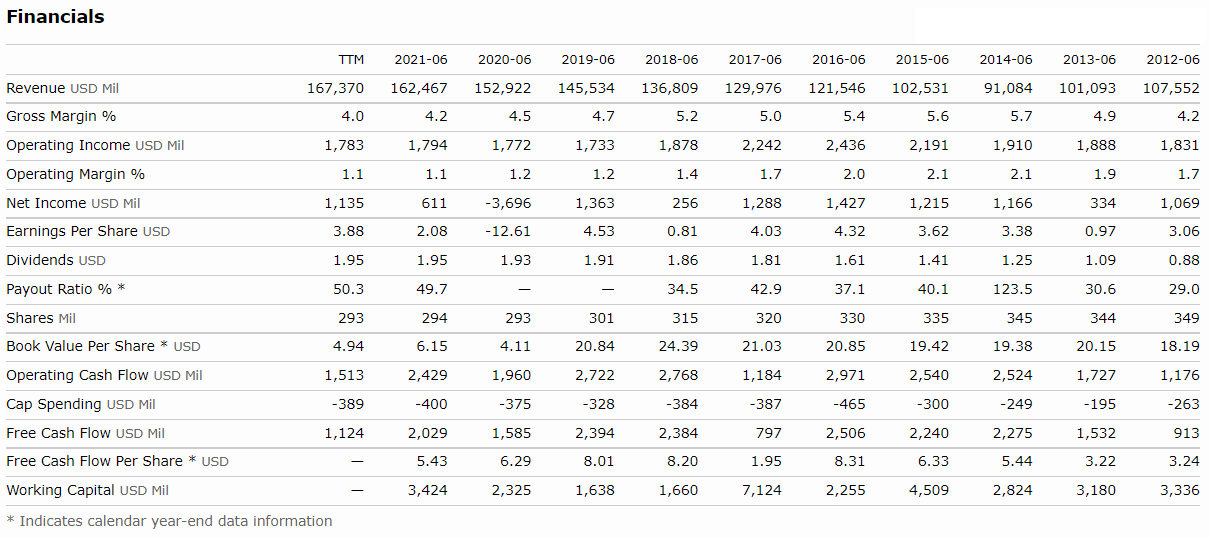

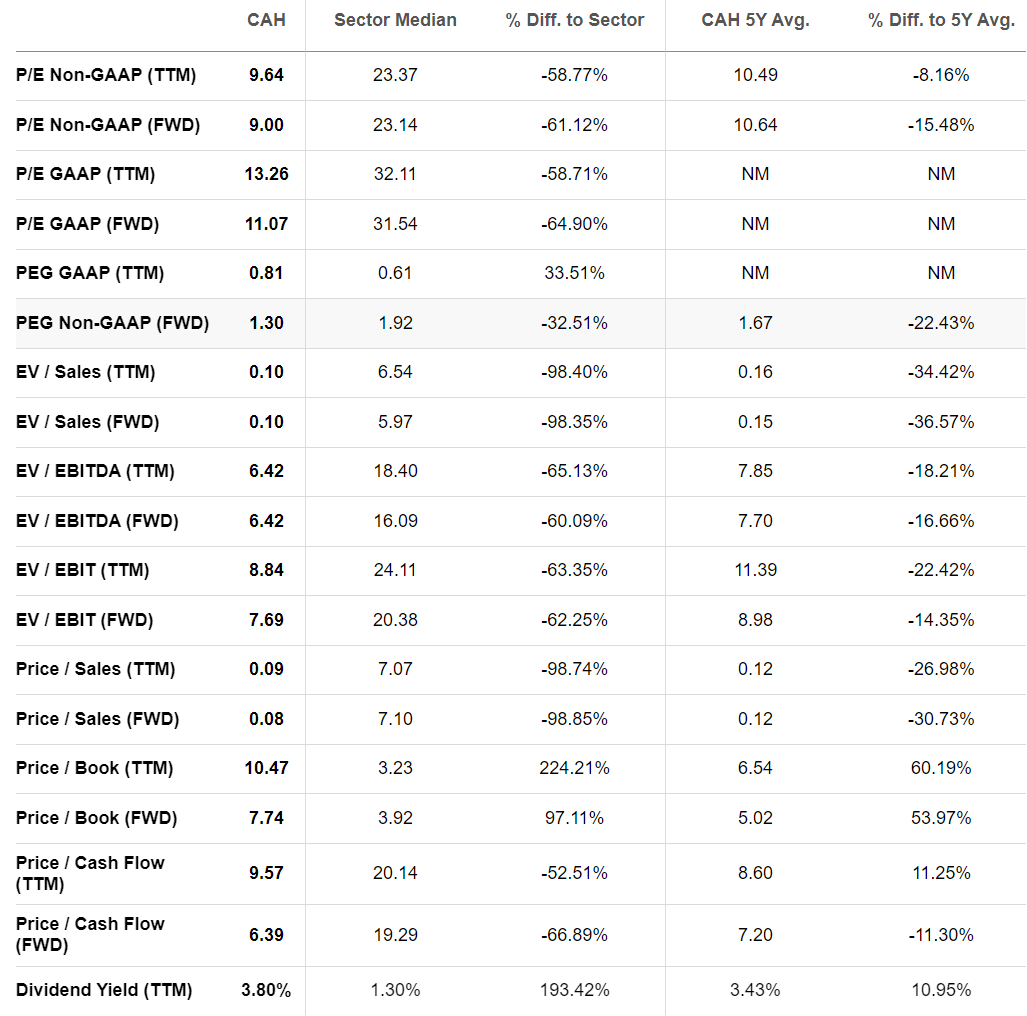

Recently, the company divested itself of its Cordis, a medical device diagnostic for vascular disease business, for $1 billion. This is expected to lower the Medical segment profits by $60-$70 million annually. Cardinal Health relies heavily on a few customers for its sales. For example, CVS Health makes up 20% of the company’s sales. Cardinal’s top 5 customers make up as much as 40% of its revenue. Nonetheless, the company has seen encouraging topline growth with 13% YoY revenue growth last quarter. With heavy demand for PPE and drug distribution, Cardinal is primed for one of its largest growth periods in years. Like many businesses, Cardinal Health struggled with supply chain problems over the past year. However, the company is pursuing long-term supply agreements and joint ventures to create more stable and reliable supply chains. Nonetheless, higher raw material and freight costs led to operating margins dropping from 1.48% in March to 1.02% the following quarters. That said, the company is making strategic investments in IT to make its distribution more efficient and improve margins. Financials We noted earlier that shares trade maybe 10%-20% higher than they did in 2011. Yet, revenues are up ~50%. Why? Because thin gross margins, which initially expanded, contracted in the following years. So, the current gross margins of 3.73% might seem like a problem. However, we, and the company, expect to raise prices in the coming year to offset the higher costs. Plus, as we read through the most recent report, management lays out why the margins compressed this year. As management noted int heir most recent quarterly call, they expect margins for medical supplies to decline further as supply chain costs weigh down profits. However, they do expect those to abate towards the end of 2022. Lastly, we want to note the company carries very little long-term debt at $5.3 billion, with half of that covered by cash and over $14 billion in inventory. This provides a great base to invest in operational improvements while returning capital to shareholders. Valuation As we mentioned earlier, Cardinal Health currently trades at an exceptional value relative to the healthcare sector and its own 5-year history.

Notably, the dividend yield is a whopping 3.8%, much higher than the sector average of 1.3% and its own 5-year average of 3.43%. While the price to trailing cash flow is higher than the company’s 5-year average, the price-to-forward cash flow looks just fine. Otherwise, Cardinal comes in at a fantastically low price-to-earnings multiple across the board. Our Opinion – 10/10 We believe markets will push Cardinal shares back below $50 as costs weigh on margins. However, management’s push to drive down operational costs and invest in technology coupled with price increases should ultimately improve margins. Cardinal is well-diversified and provides a health dividend program that can be reinvested to improve overall returns. |