|

Proprietary Data Insights Financial Pros Top Rental & Leasing Stock Searches December

|

What we’re watching

|

|

A look at industrial and construction equipment rental company United Rentals.

|

|

Stock Analysis |

The Case For United Rentals |

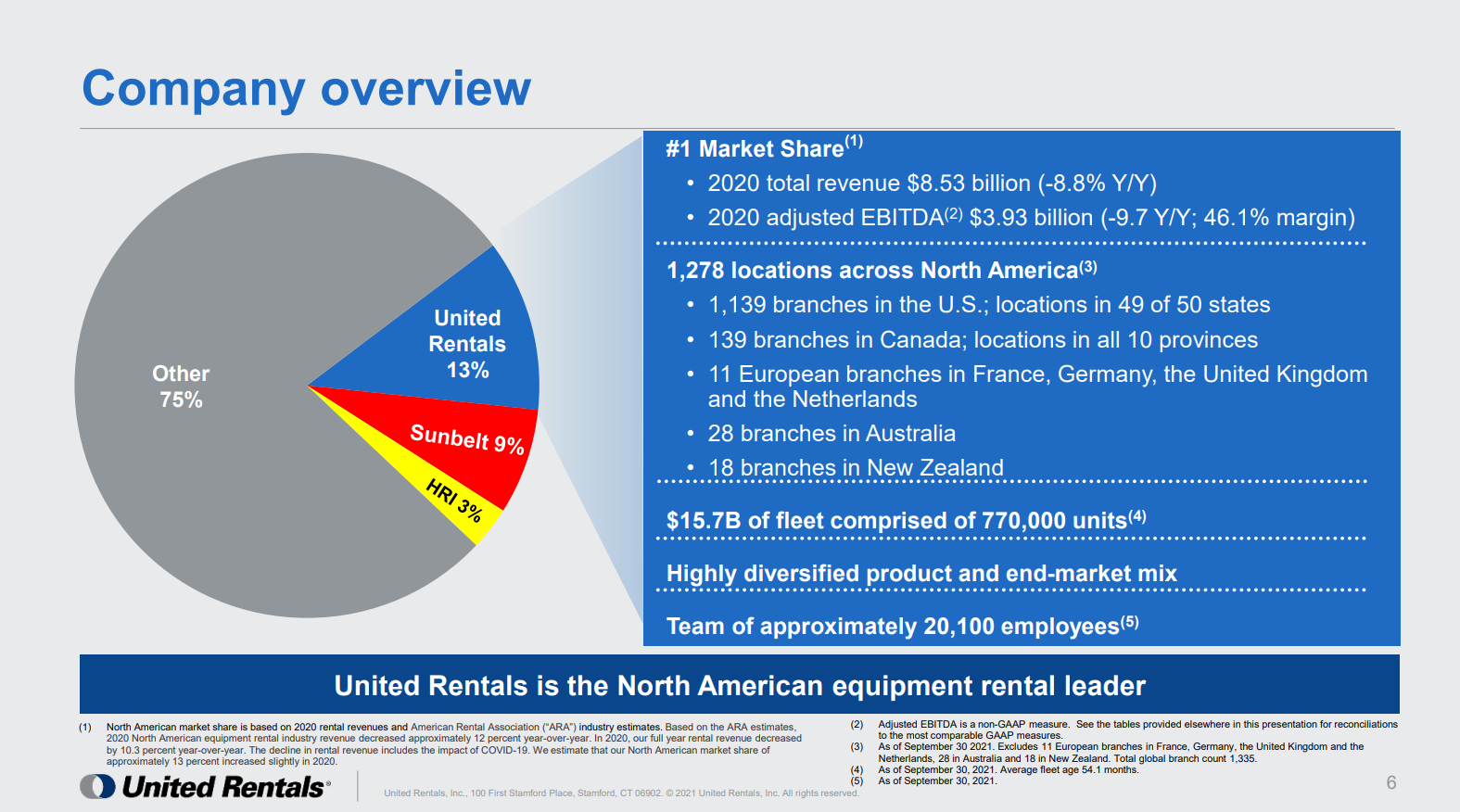

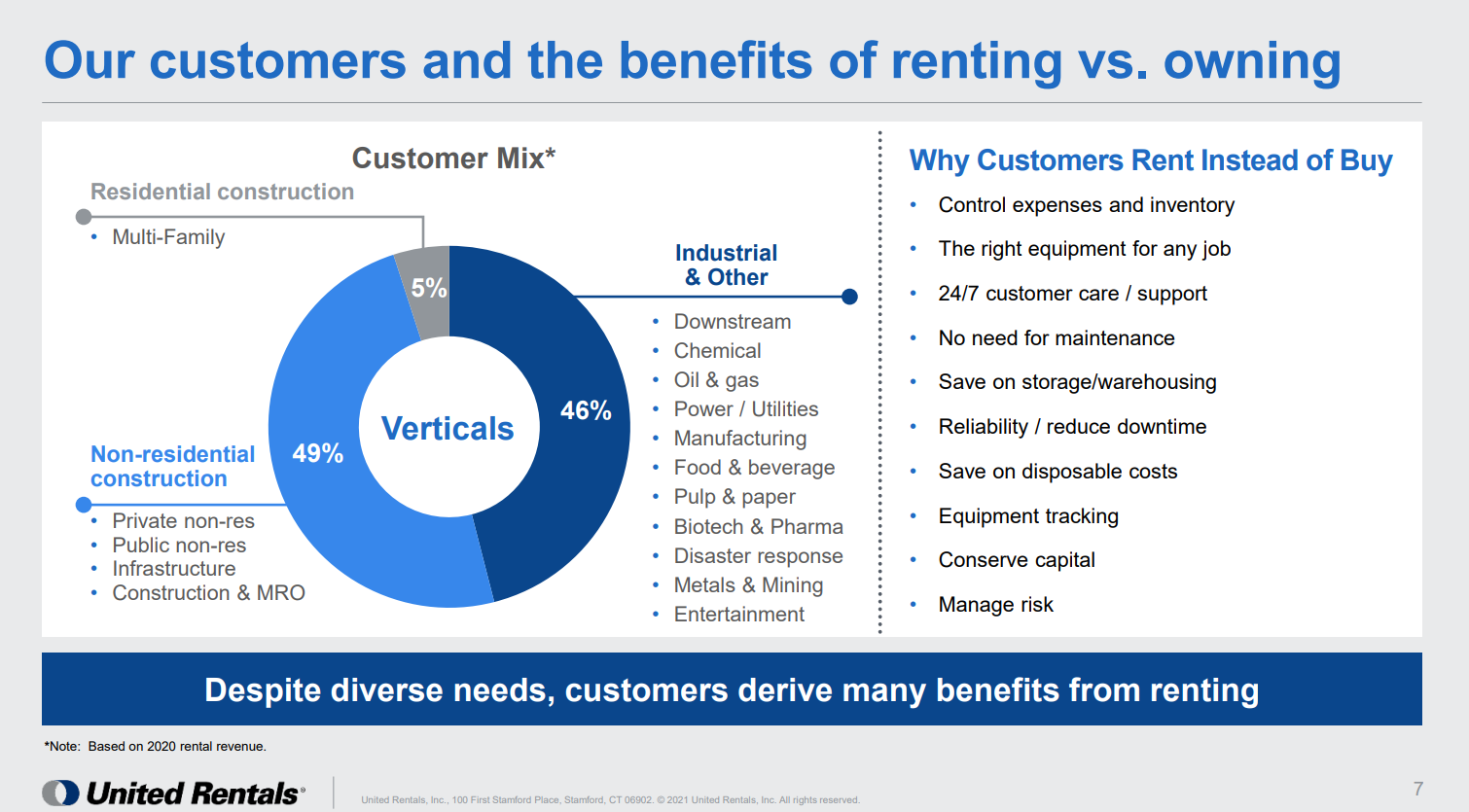

We all know about the coming construction boom in the U.S. Burned by clogged supply chains, manufacturers plan to build more domestic capacity to accommodate high demand. On the retail front, consumers continue to fight over the few houses available on the market. If you take this to its logical conclusion, it makes sense that United Rentals (URI) stands to do well in this environment. The heavy machinery provider lives and dies by demand for its equipment. And while sports and entertainment items may not be as popular, the company can’t get construction equipment out fast enough. Although it was the 8th most searched rental & leasing stock search amongst financial pros in December, the stock looks like a great value. But we’ll explain why that might not be true. United Rental’s Business Headquartered in Stamford, Connecticut, United Rentals is the world’s largest equipment rental company. URI runs a network of 1,278 locations across the U.S., Canada, and Europe with operations in 49 states and every Canadian province. The company carries 4,300 classes of equipment with a total original equipment cost of $15.72 billion. Despite its #1 status, URI only owns a fraction of the total rental market. Customers include construction and industrial companies, utilities, government agencies and municipalities, independent contractors, homeowners, and other independent renovation project personnel. URI runs two distinct segments:

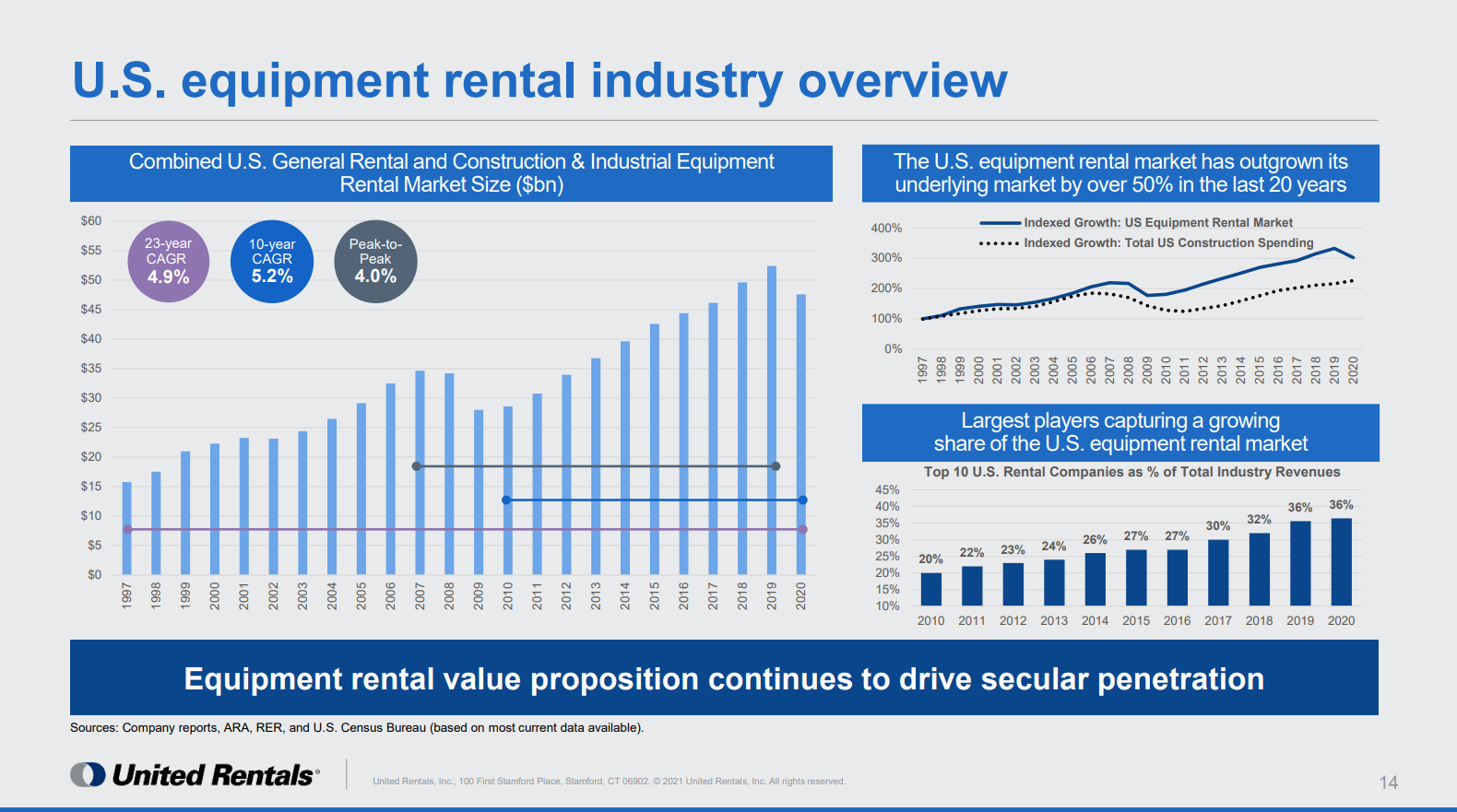

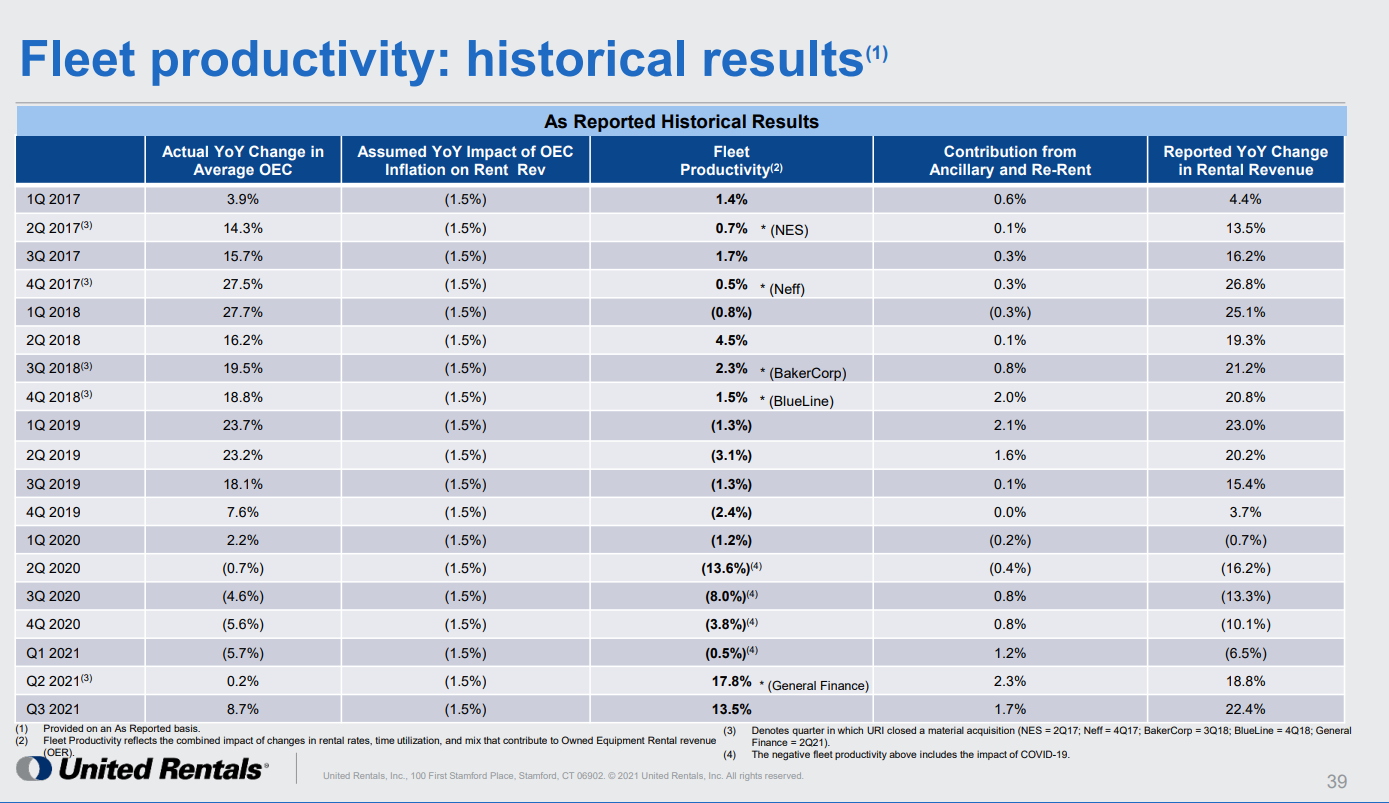

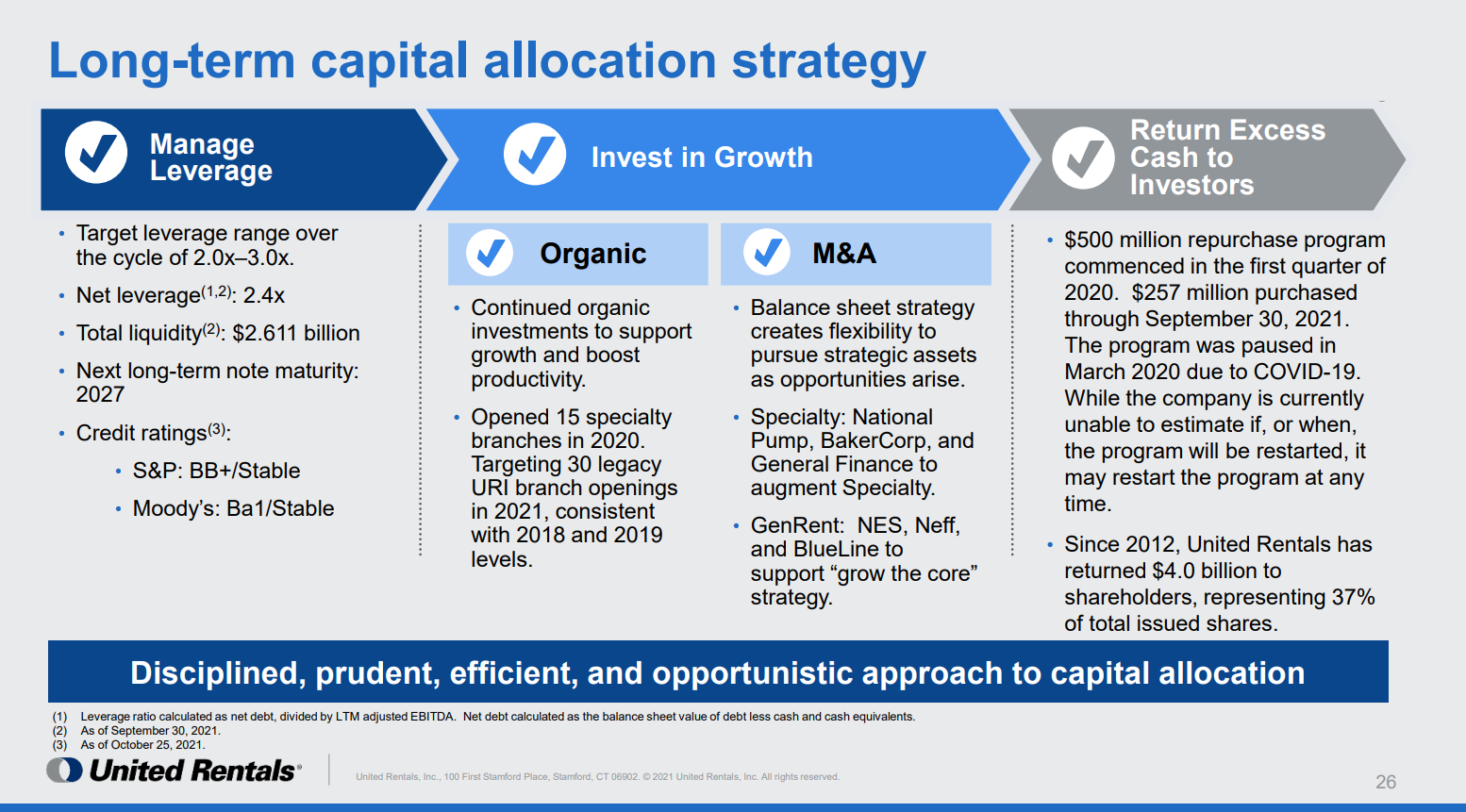

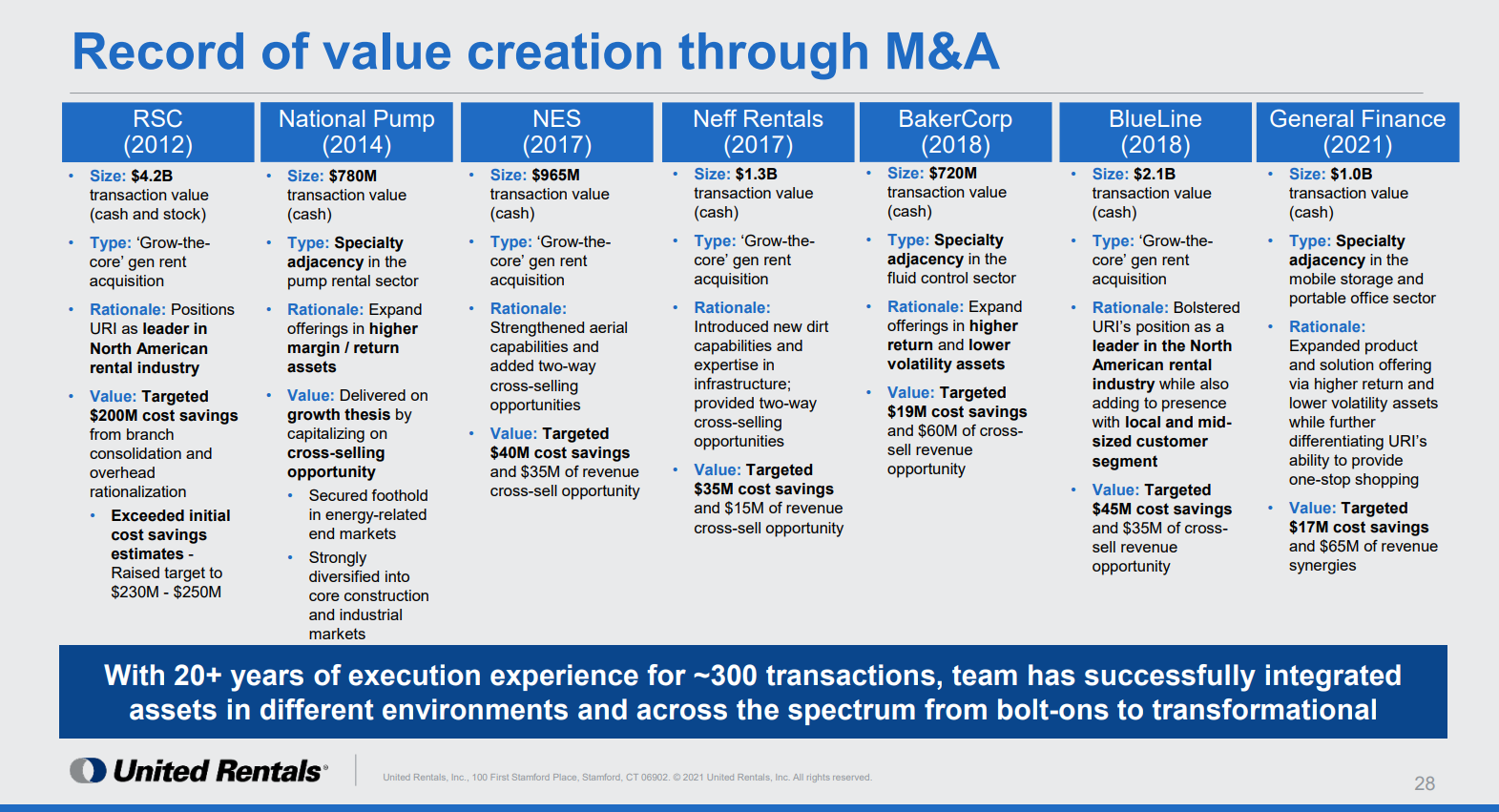

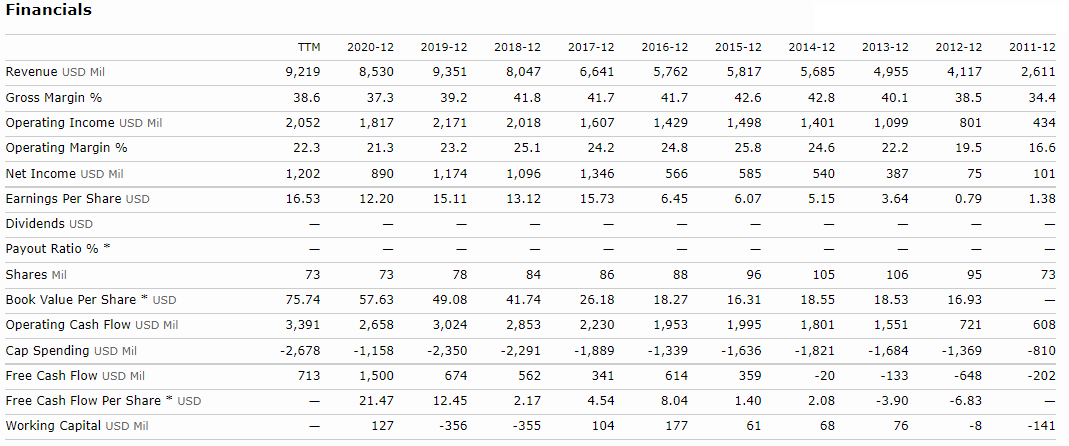

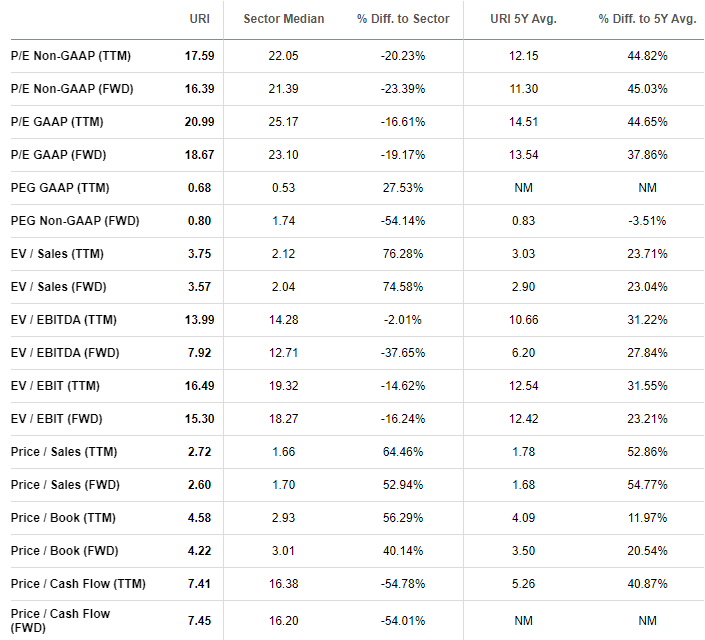

As the company notes in their presentation, the equipment rental market is quite consistent and robust with few exceptions. We believe that secular construction trends driven by the recent infrastructure bill in the U.S., pent-up demand for construction, as well as venue entertainment, bode well for the company over the next several years. This has already shown up in the company’s “Fleet Productivity” measure which combines the impact of rental rate changes and time utilization. Additionally, URI fits nicely into the business shift to capital-light models, opting to rent instead of own equipment. We like management’s long-term capital allocation strategy which balances leverage, investments in growth, and shareholder returns. With rates going up, it’s imperative United Rentals, as well as other companies, become choosier in their investments and acquisitions. And as you can see, the company hasn’t been shy about buying up competitors. Financials URI’s financials point to some interesting trends over the last decade. Revenue growth has been outstanding, with current sales more than triple where they were in 2011. The company’s 10-year average revenue growth rate sits at 14.32%. At the same time, gross margins expanded from 34.4% to 38.6%, though they are down from their highs around 42%. URI doesn’t issue a dividend, instead opting for share buyback programs. You can see that since 2013, total shares have decreased 31.1%. As a capital equipment provider, operating cash flow always looks healthy. However, free cash flow (which includes CAPEX) used to be negative. Now, they consistently put up more than $500 million in FCF every year. Lastly, we want to note that URI has very little cash on-hand with long-term debts of $9.2 billion. However, this is offset by equipment and property value of ~$11.9 billion. Valuation Turning to valuation, we get a bit of a mixed bag. For starters, all URI’s valuation metrics are higher than its own 5-year average. Given the consistent growth for the company, that is a bit troubling. However, compared to the industrial sector, URI is cheaper in many cases. While the P/E ratios are a bit high the price to cash ratios are phenomenal, especially considering the amount of money they invest in capital equipment. Our Opinion 6/10 We like everything about the company except the current stock price. Shares already fell back below $350 after breaking through $400. There is an easy case to be made that a market correction could take that price down to $200. However, that would be the spot we’d step in with both feet. But without a dividend that we could reinvest to lower our average share price, we aren’t as interested in such lofty valuations, even if they’re lower than the overall sector. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |