|

Proprietary Data Insights Financial Pros Top Rental & Leasing Stock Searches December

|

What we’re watching

|

|

A look at why Manchester United is an interesting stock.

|

|

Stock Analysis |

Want to Own a Soccer Team? |

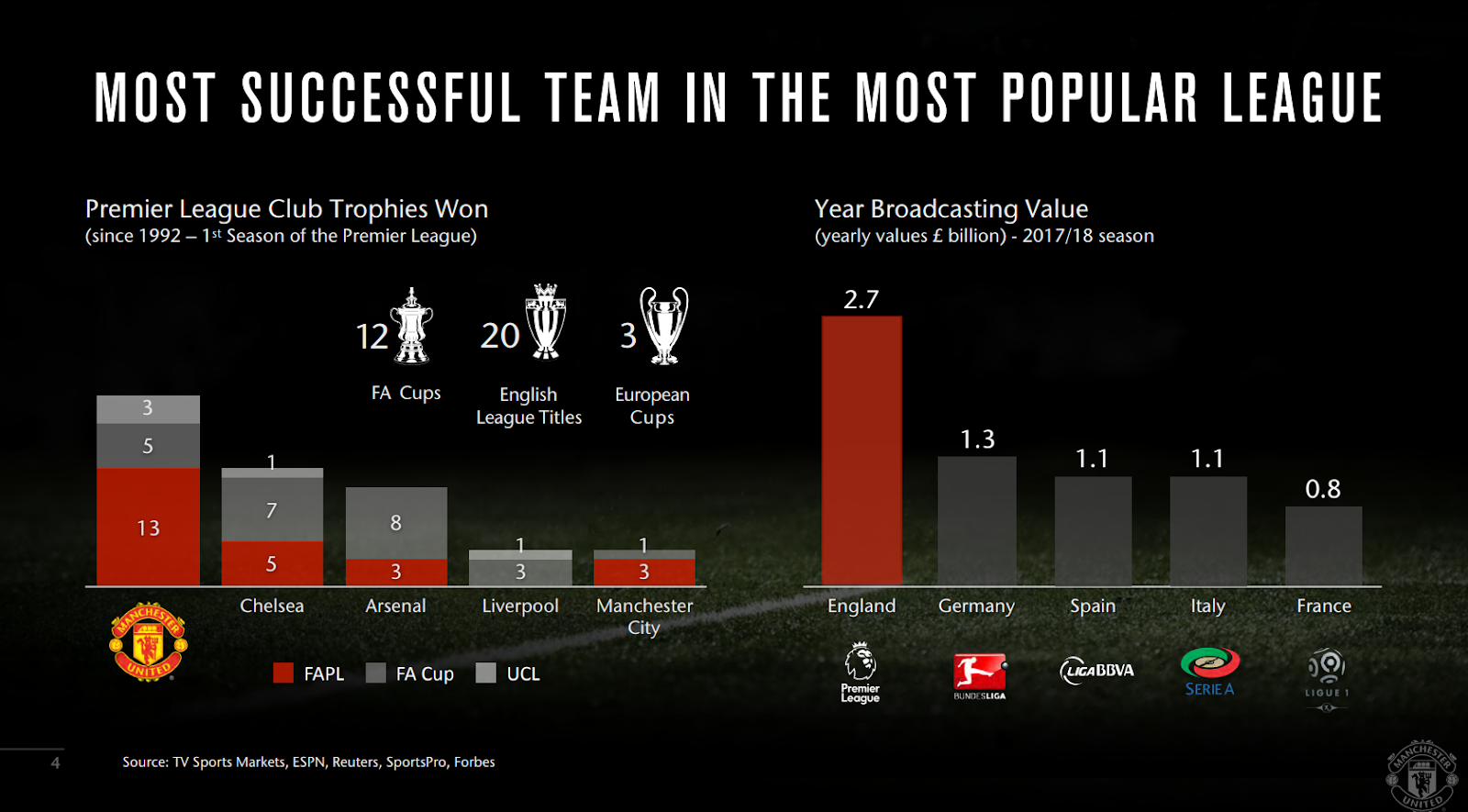

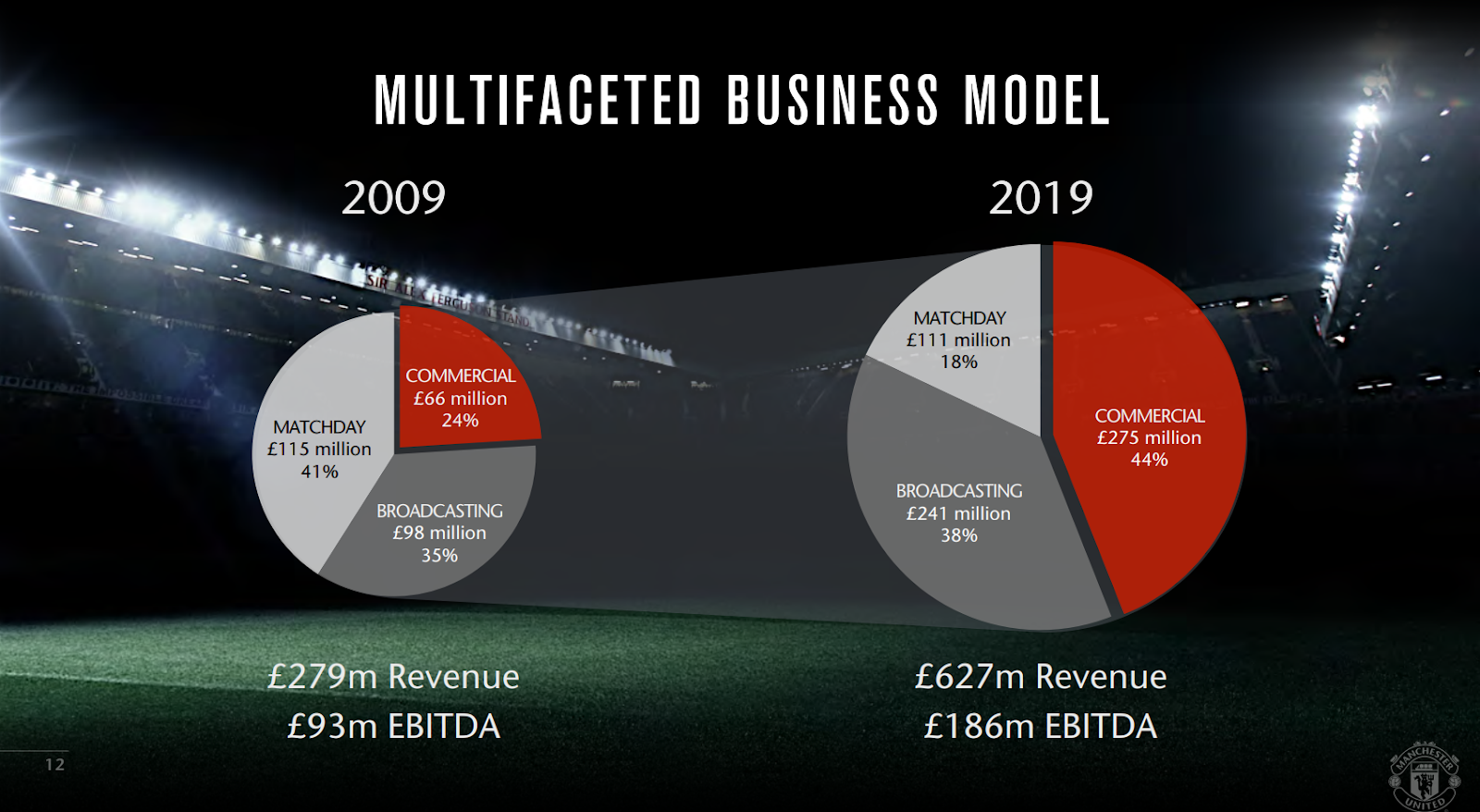

Covid made things difficult for the sporting world. Although many venues remained closed, sports continue on. At some point soon, life will return to normal. Which is why Manchester United (MANU) is an interesting stock. The fabled soccer/football team from England boasts an active global fanbase. Currently, shares trade just above $14, some of the lowest levels in the last decade. However, the financials don’t look that great at first glance. And as far as interest goes, it ranks 24th out of the 35 leisure ticker searches by retail investors last month. But could Manchester United be staged for a turnaround as fans clamor back into the stands? Manchester United’s Business Manchester United runs mens and womens soccer teams under its brand names, participating in the Premier League. Known as the ‘Red Devils’ Manchester boasts more trophies and wins of note than any other team. As one of the best in the top league, the team’s built a global fan base that extends to millions of social media followers worldwide. Unlike most U.S. sports, most of Manchester’s fanbase resides outside the U.K. Manchester United divides its revenues into three segments:

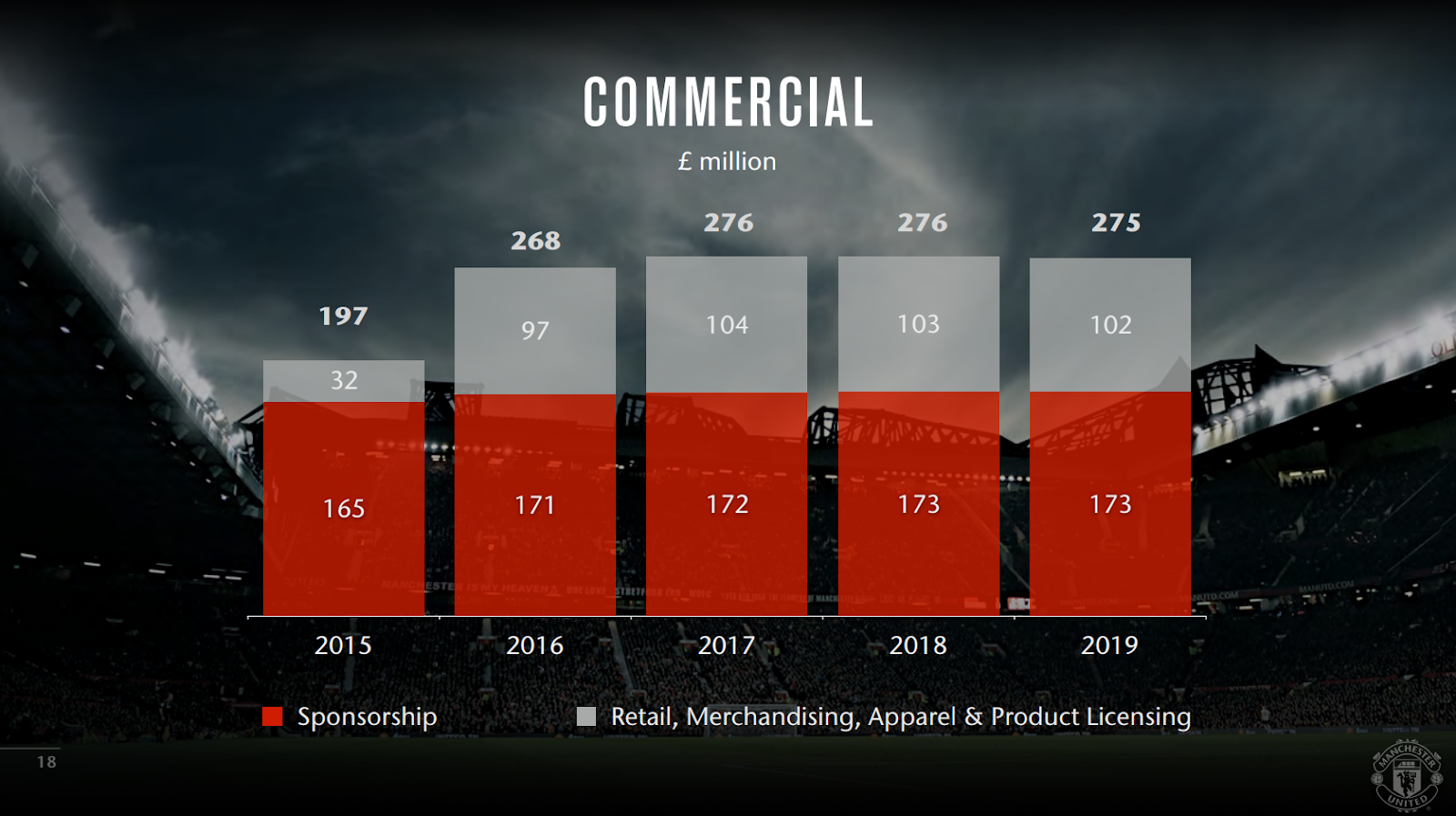

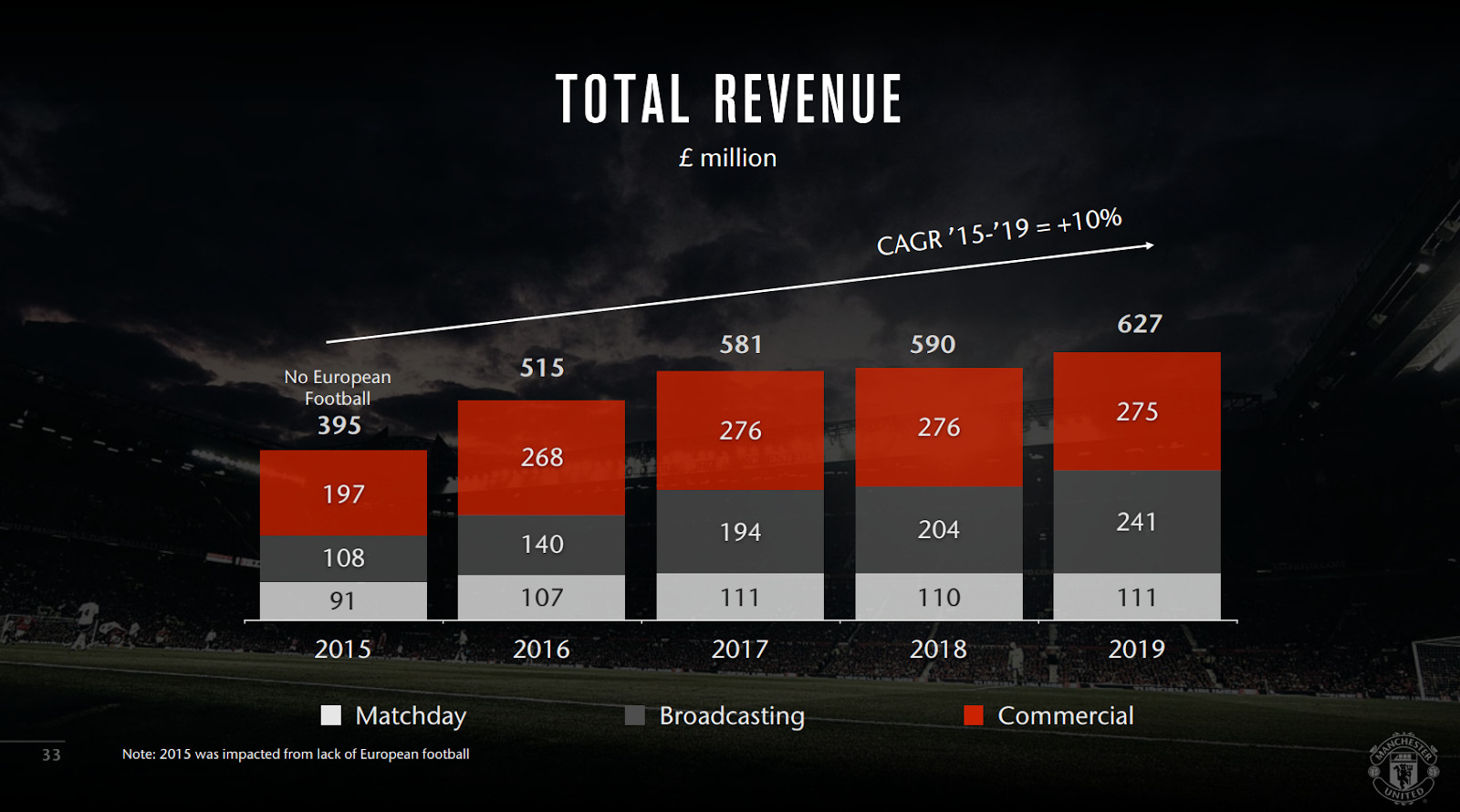

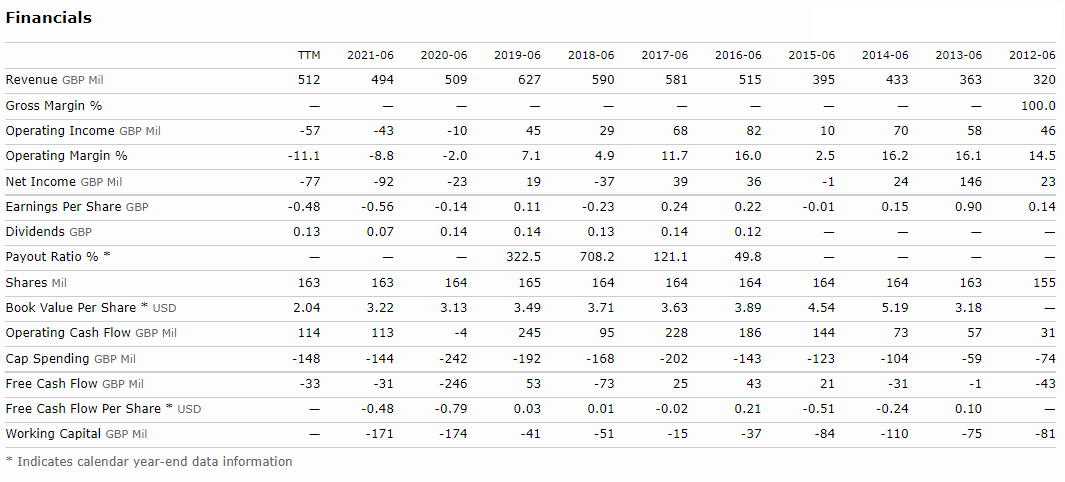

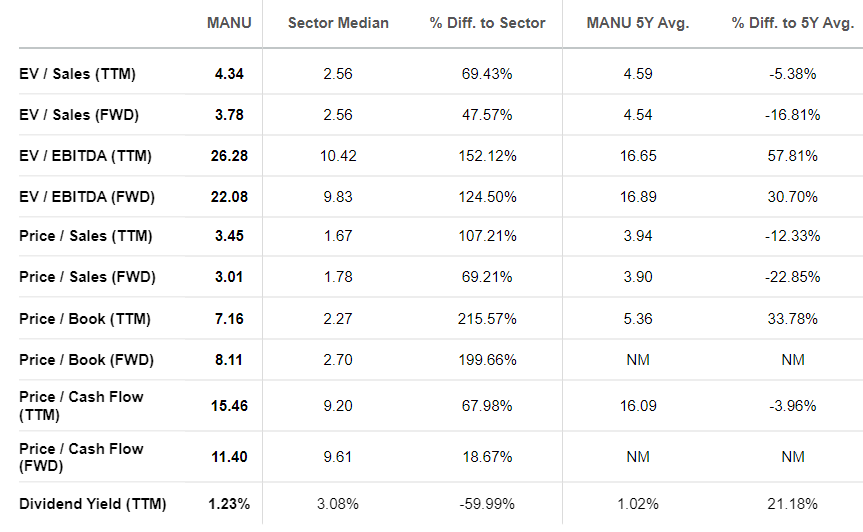

Financials The majority of Manchester’s revenue growth, in fact their only real source of revenue growth, comes from broadcasting. You can see below that commercial sponsorship and retail has been flat for years. Matchday sales have increased, but not by much. That’s led to a flat adjusted EBITDA for the last several years (excluding Covid). Note that there was no European football in 2015. So saying they had a CAGR of +10% is a bit disingenuous. Adjusted EBITDA excludes one of their largest costs – amortization. Manchester amortizes player and personnel salaries over the life of the contract. This regular expenditure is necessary but isn’t offset by any noticeable growth. All of this has led to a somewhat lackluster performance over the last decade. However, we want to point out that on an operating basis, the company generates cash rather consistently. When you take players into account, free cash flow doesn’t look as hot, but it is still positive most years. Additionally, the company pays a 1.23% dividend yield, which is descent. Valuation Since Manchester hasn’t turned a profit lately, we need to look to alternative valuation methods. There is one metric here that catches our eye – price-to-sales. While it’s higher than the sector median, it’s much lower than the 5-year average on both a trailing and forward basis. That’s important because the trailing doesn’t capture the company returning to full revenues quite yet, while the forward measure does. This says investors still value the company below its historical performance even when sales return to normal. Our Opinion – 9/10 You might be surprised we ranked this as high as we did. But when we consider the current share price in historical context and outlook, we see a lot of upside. No, we don’t necessarily believe the company will start hitting amazing earnings anytime soon to give it a nice P/E. However, the company isn’t going anywhere. And lockdowns will end. So, considering the stock has traded as low as $12 back in 2013 and as high as $27.70 in 2018, $14-$15 a share has a nice risk/reward profile. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |