|

Proprietary Data Insights Financial Pros Top Oil & Gas Integrated Stock Searches December

|

What we’re watching

|

|

Even though ExxonMobil will find itself in trouble like many other companies, there are still opportunities for value with the move to renewable energy not happening overnight.

|

|

Stock Analysis |

Exxon Mobil Has More Value Than You Realize |

Exxon Mobil (XOM) used to be the largest company in the world by market capitalization. Then fracking became a thing. And then renewable energy became a thing. Pretty soon, Exxon, like many other oil companies, found itself with lower margins and a murky outlook. Yet, the transition to clean energy isn’t happening overnight. And the pandemic created a mismatch in supply and demand that took oil prices to their highest levels in over a decade. Believe it or not, we expect them to remain elevated for the foreseeable future. As the top integrated oil and gas integrated stock search amongst financial pros last month, we know many big money managers wondered the same thing. Let us walk you through our thoughts on the company’s future and you can decide for yourself. Exxon Mobil’s Business As an integrated oil and gas company, Exxon Mobil touches two of the three areas of the oil industry:

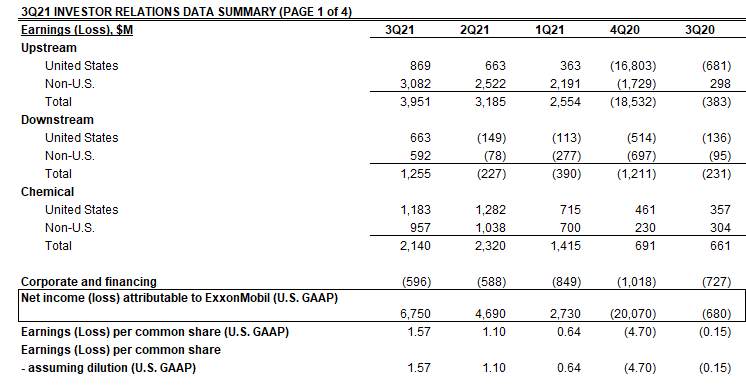

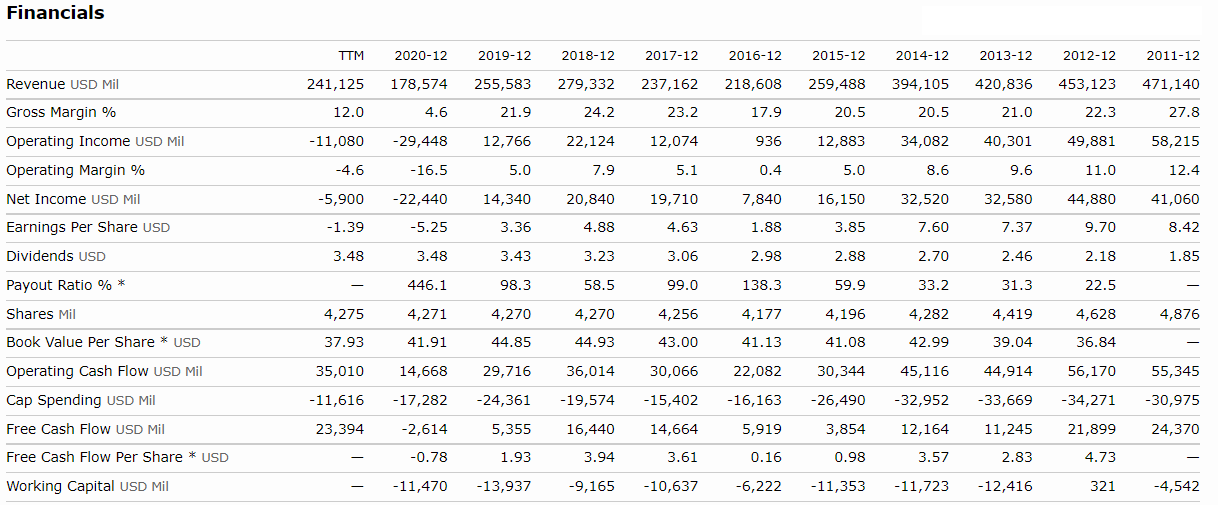

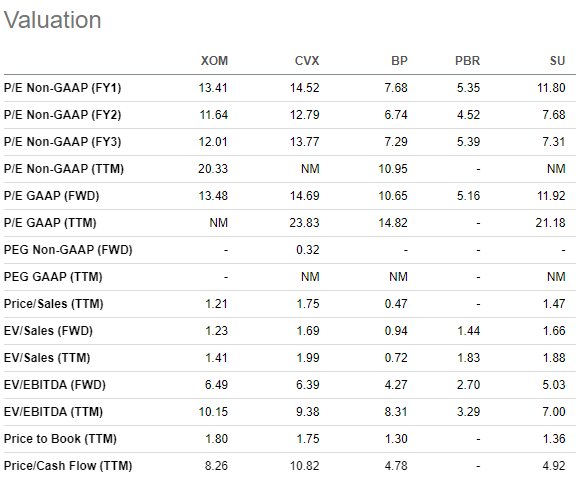

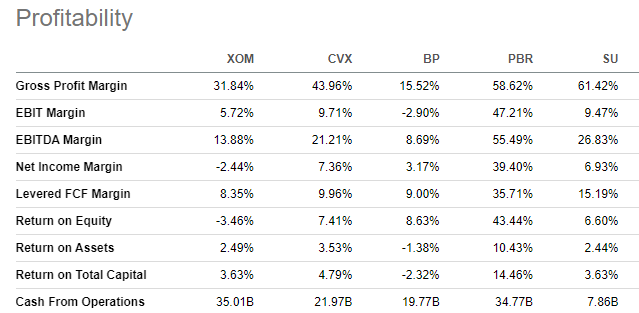

Since 2019, the company’s upstream portfolio hasn’t generated much production growth and that isn’t expected to change. However, they boast some of the most prolific assets which gives them a leg up for when they plan to use them. Compared to other energy companies, Exxon is extremely disciplined in its capital spending. Unlike many of its peers, Exxon believes renewables alone won’t be enough to meet energy demand in the coming decades. In fact, they’re betting people will need more oil in the coming years as standards of living improve. Financials It’s hard to discuss Exxon without immediately diving into its financials. While 2020 was a difficult year for the company, things have begun to look up in 2021. Specifically, all operations now operate at a profit. If we extended their current operations out into the future, the company would generate profits that match some of its best years in the last decade. It’s important to note that although revenues aren’t what they once were, operating and free cash flow are still doing extremely well. We also want to point out the consistency and level of the company’s dividend which pays a stunning 5.11%. Lastly, we’d like to note that although the company carries +$43 billion in long-term debt, that could be paid off in two years if they do what they did in the last 12 months. Valuation We felt the best way to look at Exxon’s valuation was to compare it to the top searches from our data. We should start with the obvious – not all companies have turned a profit yet. That’s fair, which is why it’s probably best to look at the forward P/E. In that regard, British Petroleum (BP) and Petrobras (PBR) come in cheaper than Exxon, Chevron (CVX), and Suncor (SU). However, Exxon boasts a better price to sales with the exception of BP and the same with Enterprise Value (EV) to sales. While the price to cash flow isn’t as cheap as BP Suncor’s, at 8.26x it isn’t too shabby. It’s worth noting that Petrobras’ stock price is depressed due to political uncertainty. And as we show below, BP isn’t exactly profitable yet. While Petrobras takes the top spot for margins, Suncor comes in a close second followed by Chevron. Exxon’s margins aren’t too bad, but still not as good as its peers. Our Opinion – 6/10 While we like the stability and discipline of Exxon, shares simply trade at too high a multiple. And stacked up against its peers, we prefer Chevron or Petrobras (as a riskier play). It might sound like a big ask, but we’d prefer Exxon closer to $50 per share. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |