|

Proprietary Data Insights Retail Top Bank Stock Searches January

|

What we’re watching

|

|

A look at the temporary setback for JP Morgan with its latest earnings report.

|

|

Stock Anlaysis |

The Case for JP Morgan Chase |

Investors weren’t particularly thrilled with JP Morgan Chase’s (JPM) latest earnings report. While the company beat revenue and earnings expectations, the CFO lowered guidance on ‘headwinds’ such as wage inflation and moderating Wall Street revenue. We see this as a temporary setback for a company that’s poised to deliver serious returns to shareholders. It’s not entirely surprising to see the stock top our list of bank stock searches by retail investors. Because when JP Morgan’s stock drops +6% in a day, you turn your head. When it drops more than 10% in two days, you sit up and pay attention. Despite the negative momentum, JP Morgan is an incredible value. And with interest rates set to rise, bearish sentiment seems overdone. JP Morgan’s Business JP Morgan needs little introduction. The mammoth bank, led by CEO Jamie Dimon, manages $3.74 trillion in assets with stockholders’ equity worth $294.1 billion and operations in more than 60 countries. The company’s business splits into five categories:

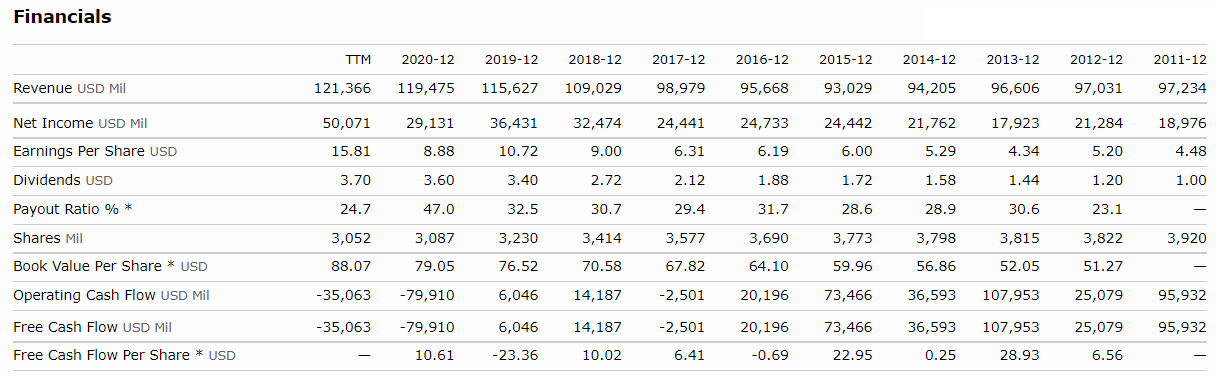

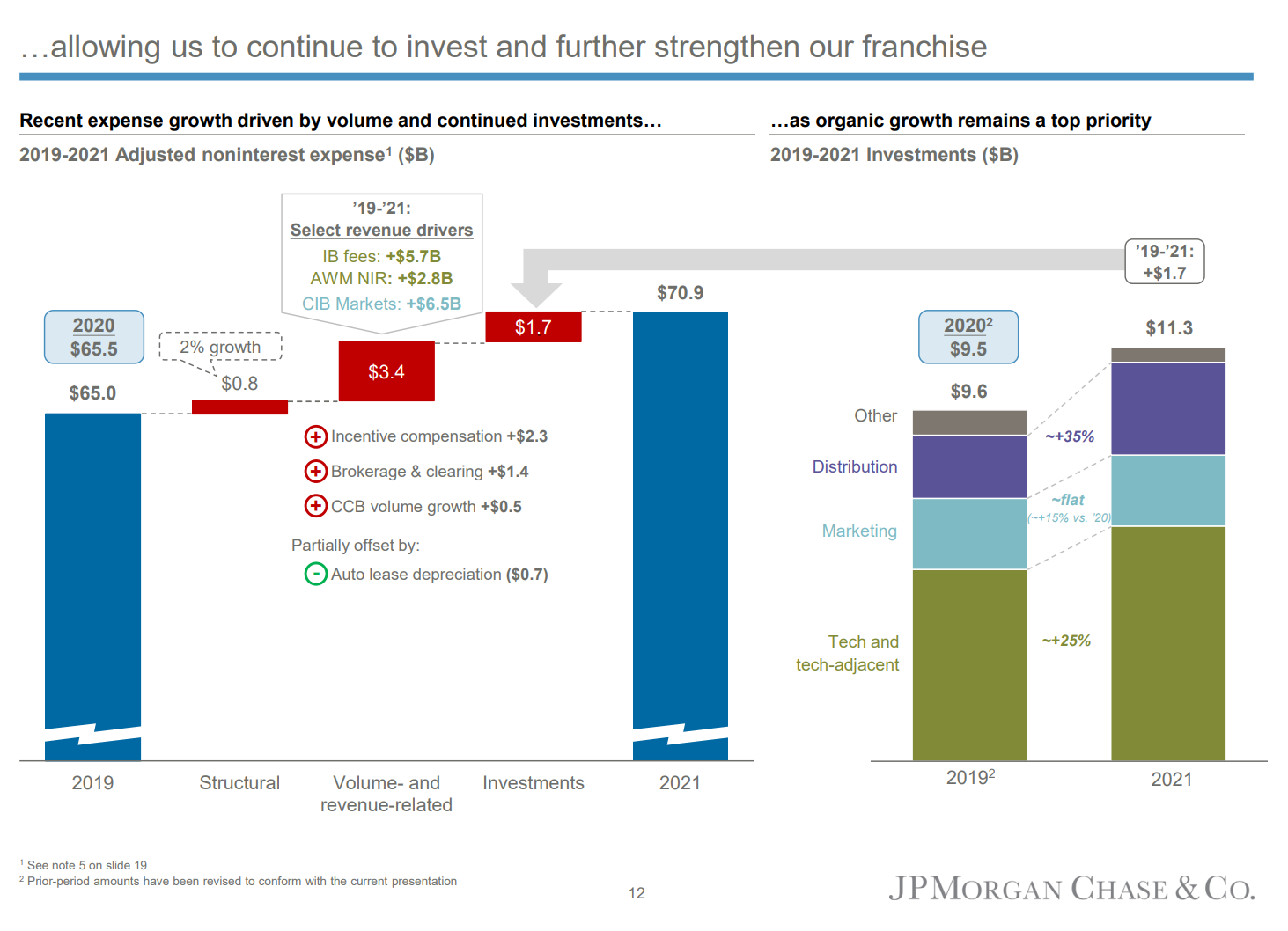

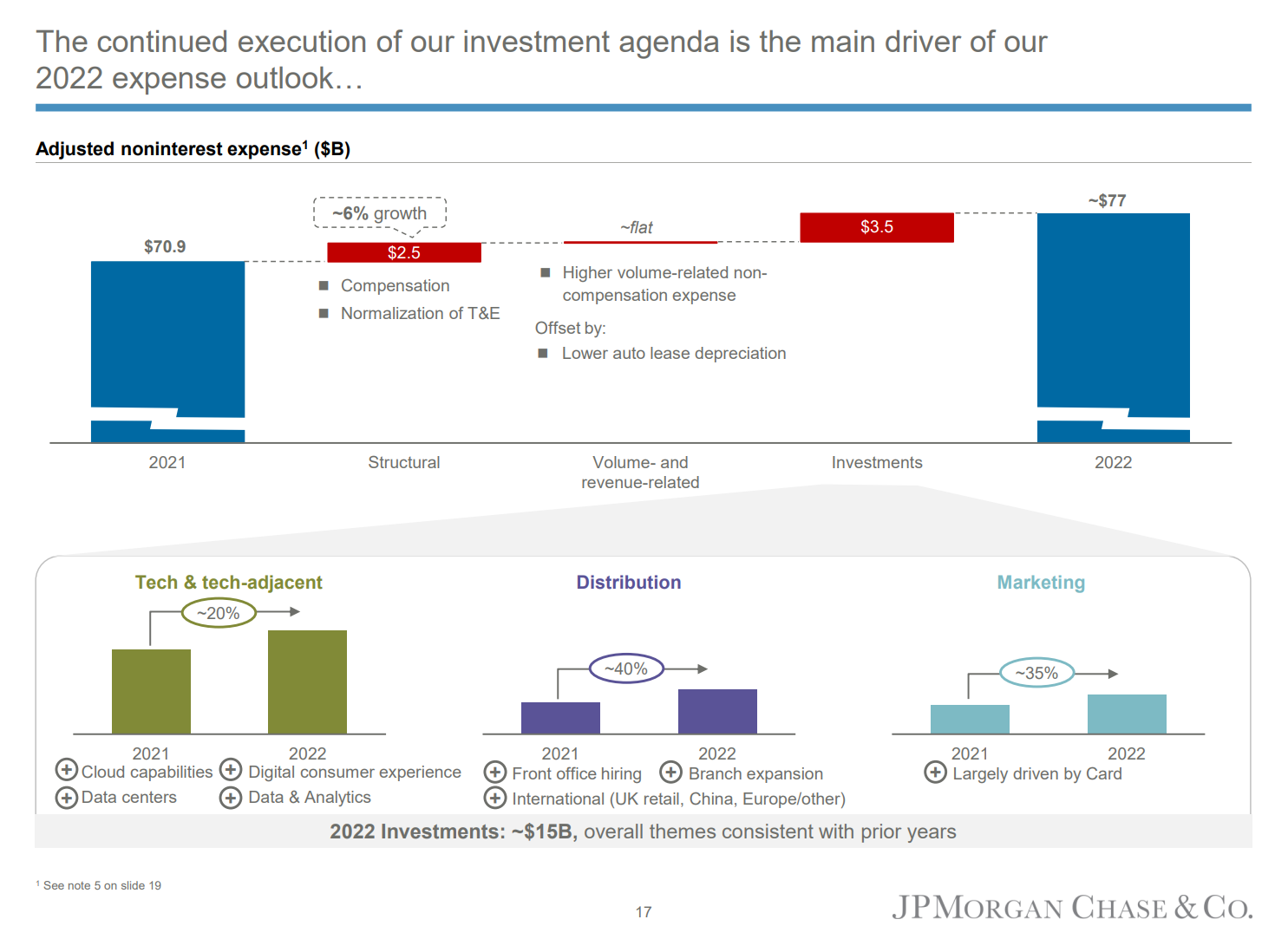

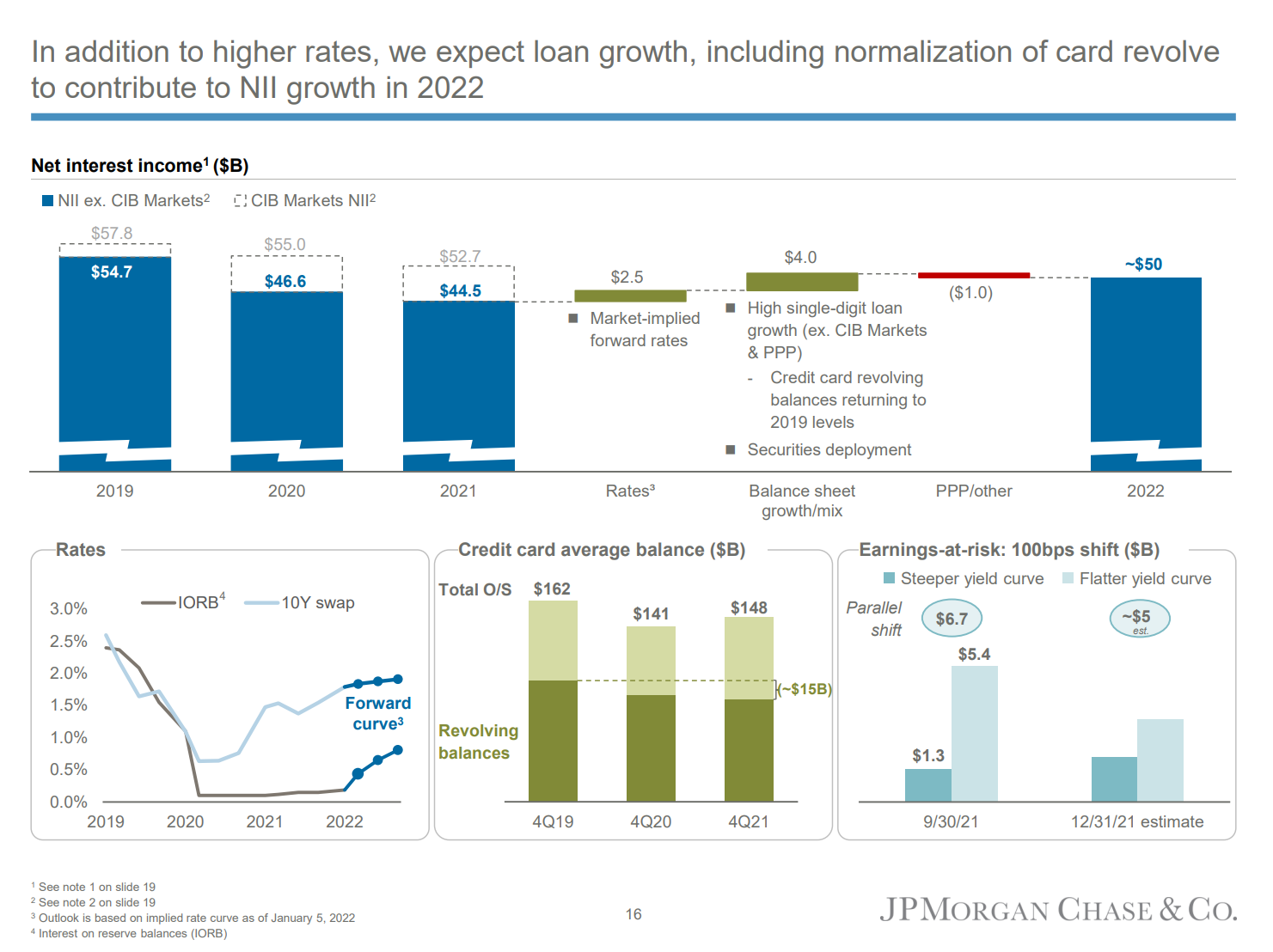

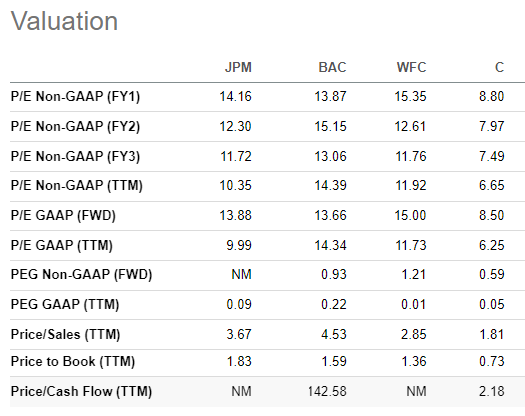

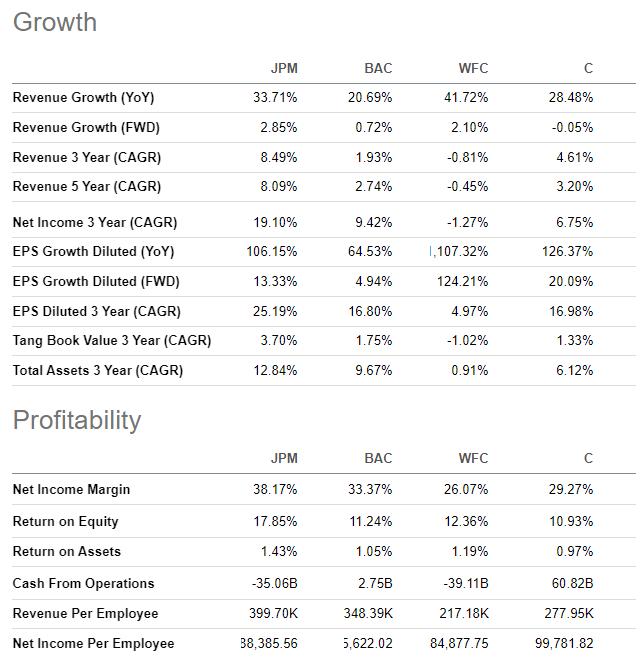

Financials It’s pretty tough to analyze JP Morgan and not start immediately talking about the financials. Because we analyze banks differently than other businesses, we wanted to use the 10-year history to highlight the sizable revenue and dividend growth as well as the book value per share. Now, we judge most banks by their non-interest expenses as to whether they manage themselves well operationally. To that end, we use the following slide from the company’s recent presentation. Management highlighted higher expenses with a large chunk driven by incentive compensation. This has been a key theme across multiple banks. Consequently, JPM expects non-interest expenses to increase by 8% in the coming year. However, part of that comes from investments in technology. The good news is that they also see growth in net interest income, driven by higher rates of $2.5 billion in 202 with an additional $4.0 billion from loan growth. This helps offset the costs and a drop in investment banking revenues which have begun to wane as the Fed pulls back on stimulus and general trading declines. Valuation To get a sense of JP Morgan’s value, we’re going to stack it up against other banks that reported during the same period. Looking at the price-to-earnings (P/E ratio, Citigroup (C) is the cheapest bank looking backwards and forwards. We’re quite bullish on Citigroup. However, JP Morgan doesn’t look too bad and holds its own relative to its peers. Price to book (P/B) is the only relevant metric where it comes out more expensive than its peers. P/B is an important metric because it tells you the price of the stock relative to the book value of its assets (loans) minus its liabilities (deposits). Next, we want to compare each company’s growth and profitability. Wells Fargo (WFC) had the best YOY revenue growth. But looking forward, JP Morgan is set to outperform its peers. Additionally, JP Morgan smokes them all when it comes to consistent revenue, income, and earnings growth over a multi-year period. Lastly, we want to note that JP Morgan has the best net income margin, return on equity, and return on assets. This is important because it says they’re handling their business better and returning more than their peers. Our Opinion – 8/10 We love JP Morgan and wouldn’t be ashamed if we owned it here at $150. However, we expect earnings to continue to weigh on stocks for a few more weeks, hopefully giving us a chance at $140 per share. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |