|

Proprietary Data Insights Financial Pros Restaurant Stock Searches January

|

What we’re watching

|

|

Whilst most restaurants have suffered during Covid, BBQ Holdings has thrived.

|

|

Stock Analysis |

BBQ Looks Delicious |

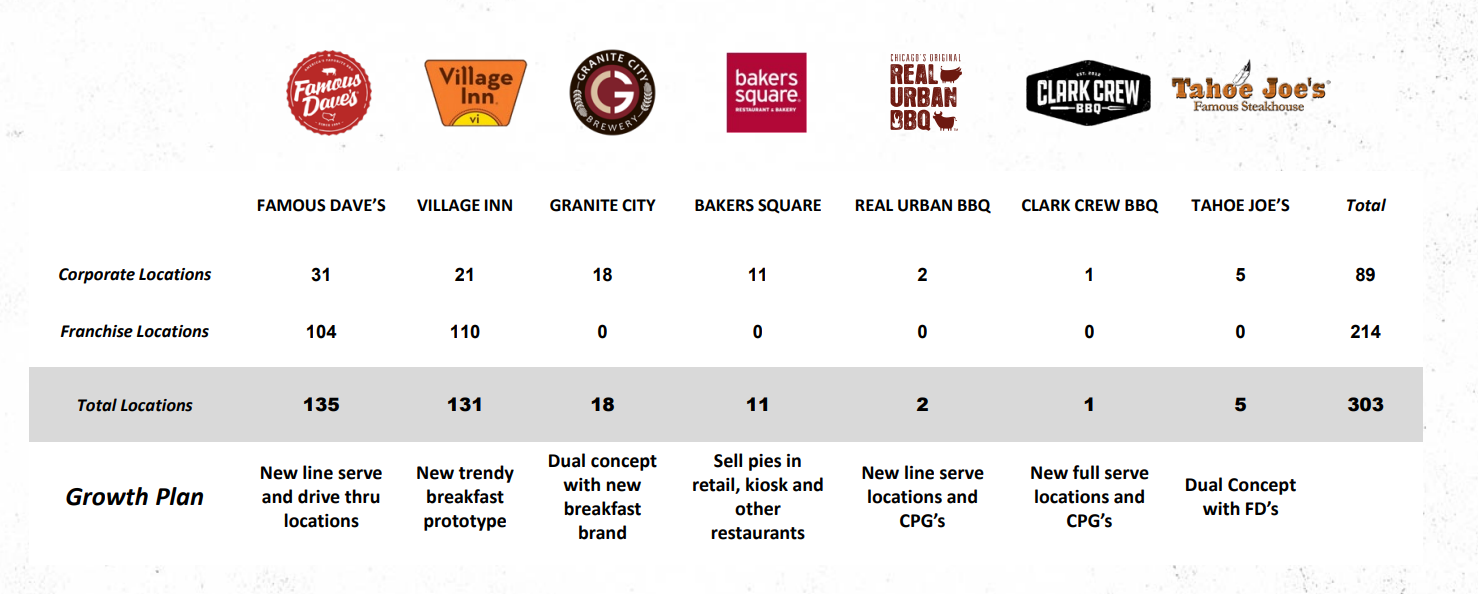

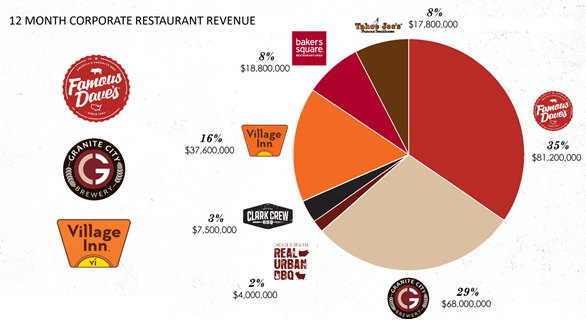

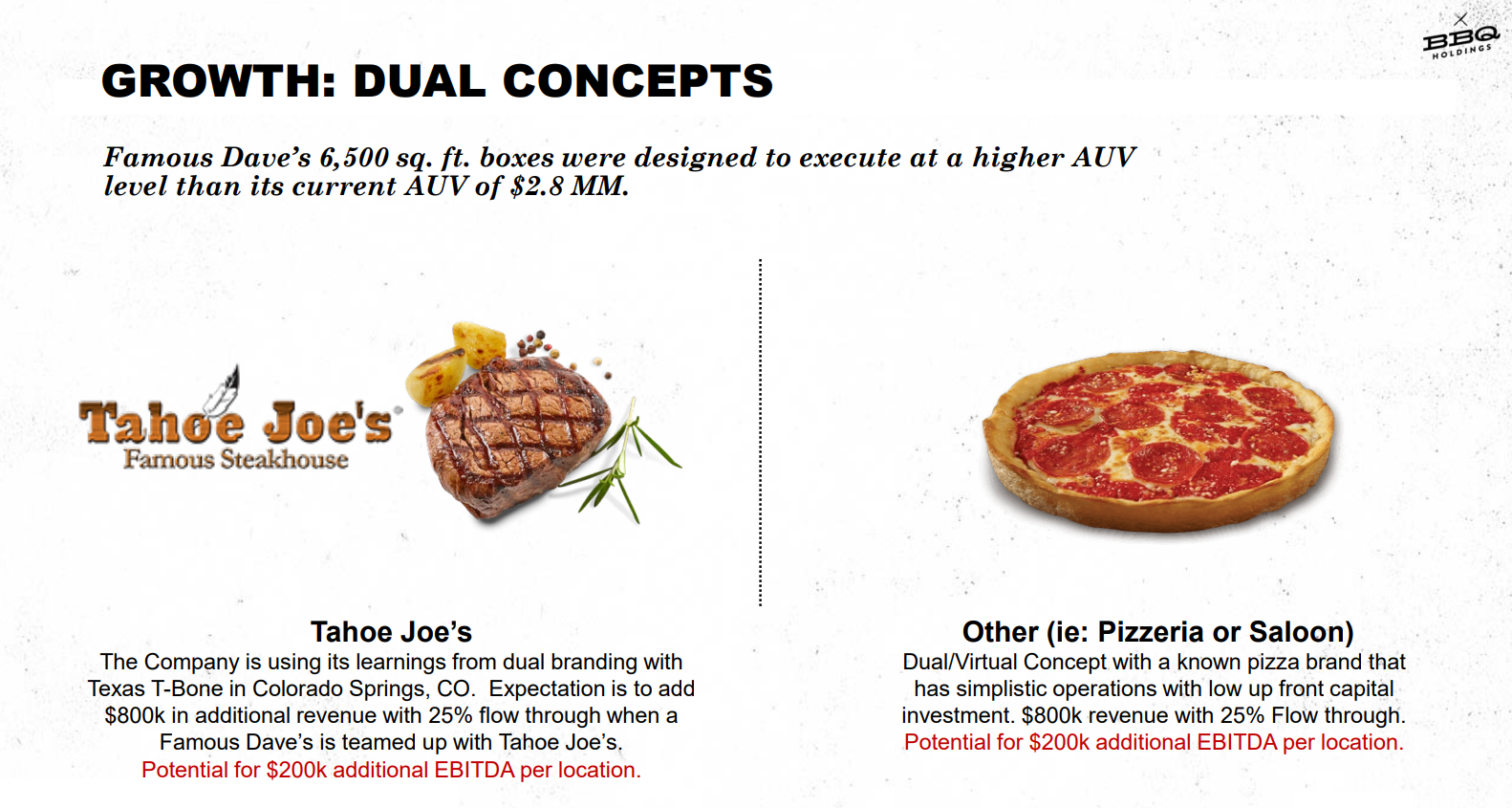

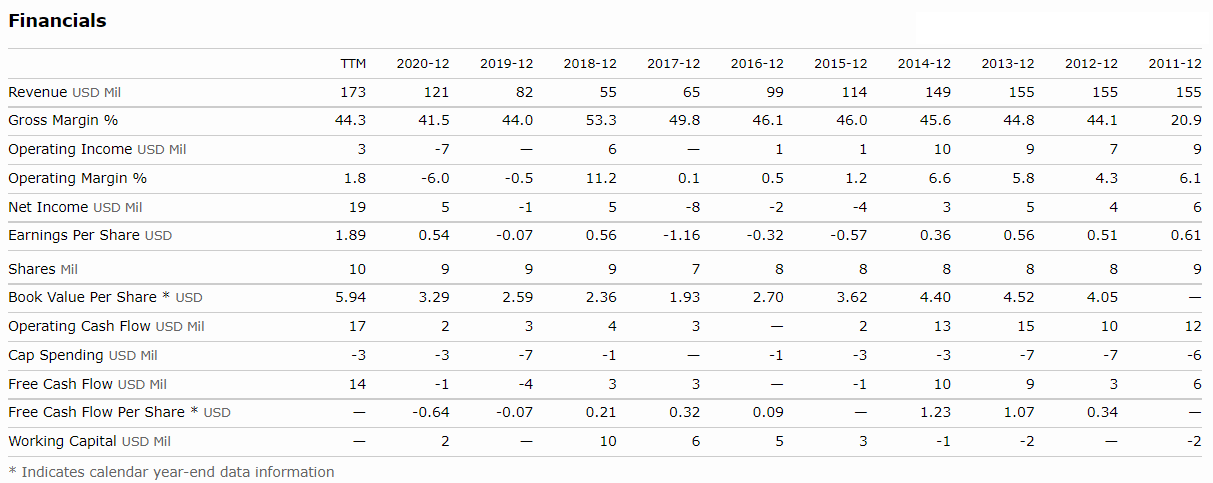

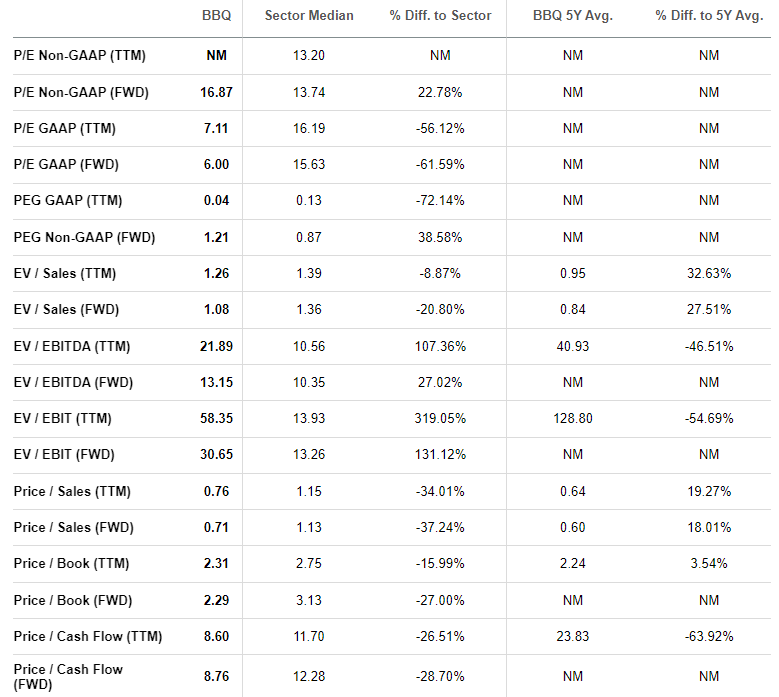

Try going out to dinner Friday or Saturday night and you’re likely to hit a wait. Restaurants face exorbitant demand both in-house and through delivery. And there are a lot fewer of them than a couple of years ago. Roughly 14% of US restaurants, or around 90,000 eateries, closed due to Covid. The ones left open struggle to staff up. So it hasn’t been going well for many. That is except for BBQ Holdings (BBQ). While BBQ Holdings faces similar labor issues, management has created an incredible turnaround, nearly quadrupling operating cash flow over the last 3 years. According to our proprietary search data, no financial pros searched out BBQ this month. And we think that makes this stock an undiscovered gem. Here’s why. BBQ’s Business Known for the Famous Dave’s restaurants, BBQ Holdings runs seven brands with 303 locations in three countries. Most locations are in 31 U.S. states with the remainder in Canada and the United Arab Emirates. Of the 303 locations, the company owns 89 with 214 run as franchises. The company also operates 28 ghost kitchens. While BBQ remains the company’s main focus, it’s expanded into other categories with the Village Inn as well as bakery. Currently, the company is refocusing on franchising and away from direct ownership. Over the last few years, the company changed the way it ran its business. The company acquired several other brands as well as changed the way they do business including the addition of pick-up and drive-through windows. Ghost kitchens are a new concept the company hopes to leverage to add service in areas that may not have been viable for a full restaurant. Additionally, the company has implemented dual kitchens where the same kitchen services two restaurants using the same equipment and staff. BBQ Holdings also licenses its products to consumer packaged goods companies for sale at local grocers. Lastly, we want to note the company’s strategy to continue M&A. Management wants to add brands that not only add to earnings but fold into its current infrastructure and have a potential for CPG sales. Financials BBQ Holdings saw revenues slide dramatically in the early part of the decade, only recovering in the last few years. However, management’s work has helped lift the company’s sales, which have more than tripled in the last 3 years, and profits. In fact, in the last 12 months, the company has seen its highest operating and free cash flows as well as earnings in the last decade. While the company has whittled down long-term debt to just $7 million, its capital leases have grown to $78 million. However, that’s offset by the $29 million cash on hand. One key item to note. In the last 9 months, the company added $14 million to its bottom line through PPP loan forgiveness. It also received $3.2 million in gains from an acquisition of a Village Inn location. If we strip these numbers out, net income lands at $4.1 million for the 9 months compared to a loss of $5.9 million the prior year. That brings our assumed 12-month net income to $5.47 million or $0.52 per share. Valuation The stunning turnaround has made shares incredibly cheap in valuation terms. At 6x forward GAAP earnings, shares are some of the cheapest in the sector. However, as we noted earlier, the adjusted EPS should be something like $0.52 per share TTM. That would give us a TTM P/E ratio closer to 26x. And it explains the difference between the forward GAAP and non-GAAP estimates. Those non-recurring items are why the EV/EBITDA measures look high relative to the sector. Yet, the price to cash flow ratios looking backward and forward as well as the price to sales ratio appear incredibly cheap. Our Opinion 10/10 This micro-cap has enormous potential. And as a speculative play, we could see the stock doubling over the next couple of years. Now, it’s certainly possible the operational efficiencies and profits the company is currently generating don’t hold. But as long as the company continues its expansion efforts, we believe they’re doing all the right things to become a better company. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |