|

Proprietary Data Insights Retail Top Oil & Gas Midstream Stock Searches January

|

What we’re watching

|

|

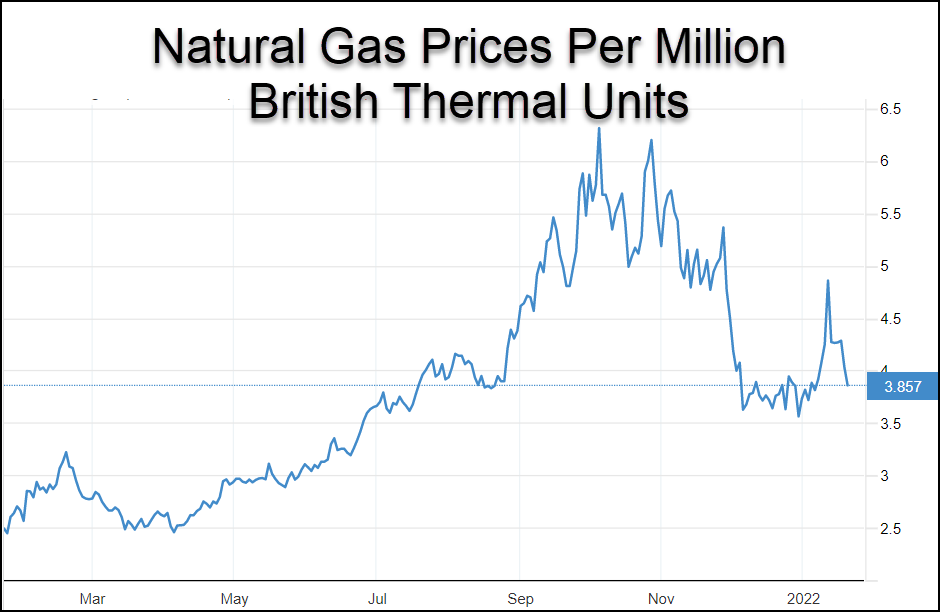

A look at Cheniere Energy who are taking advantage of the rise in natural gas prices.

|

|

Stock Analysis |

Cheniere Energy’s Export Boom |

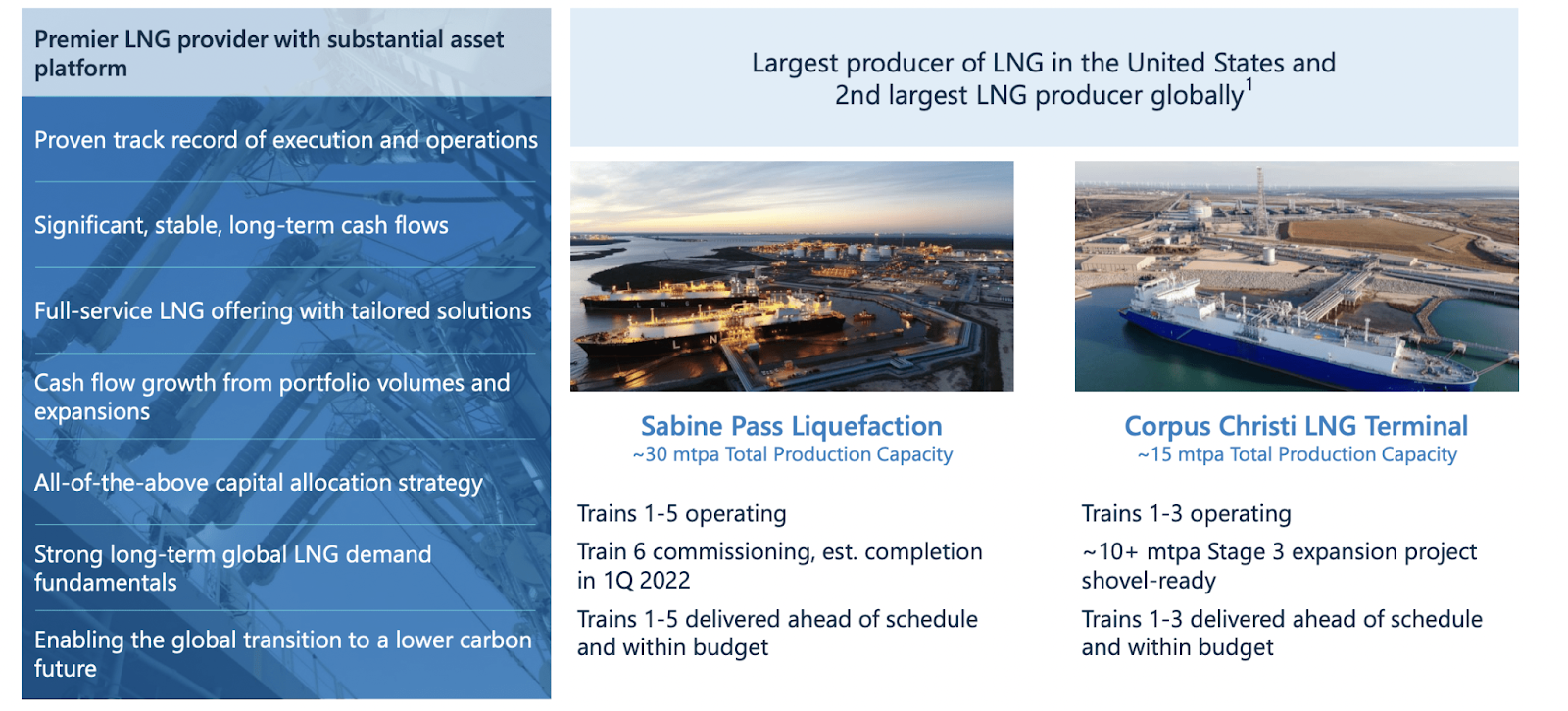

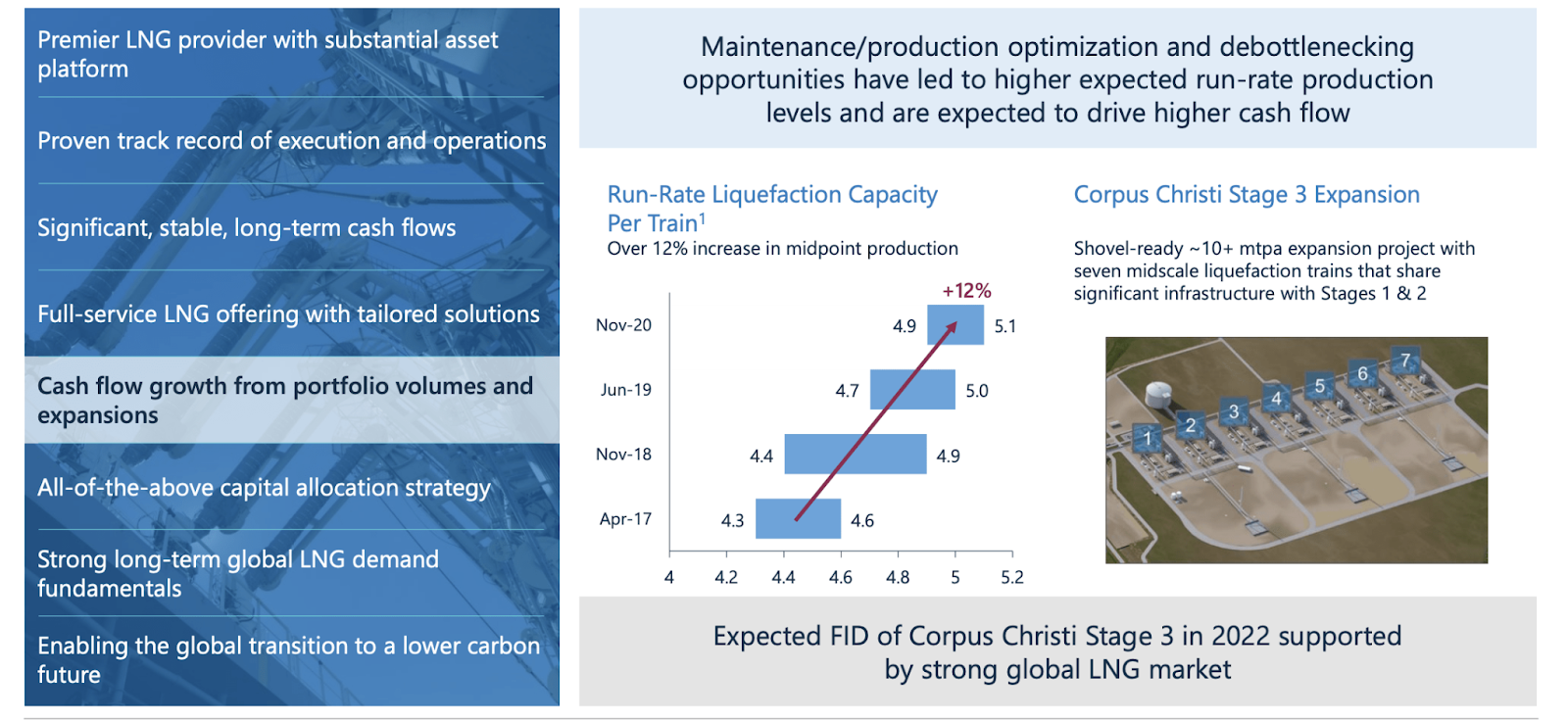

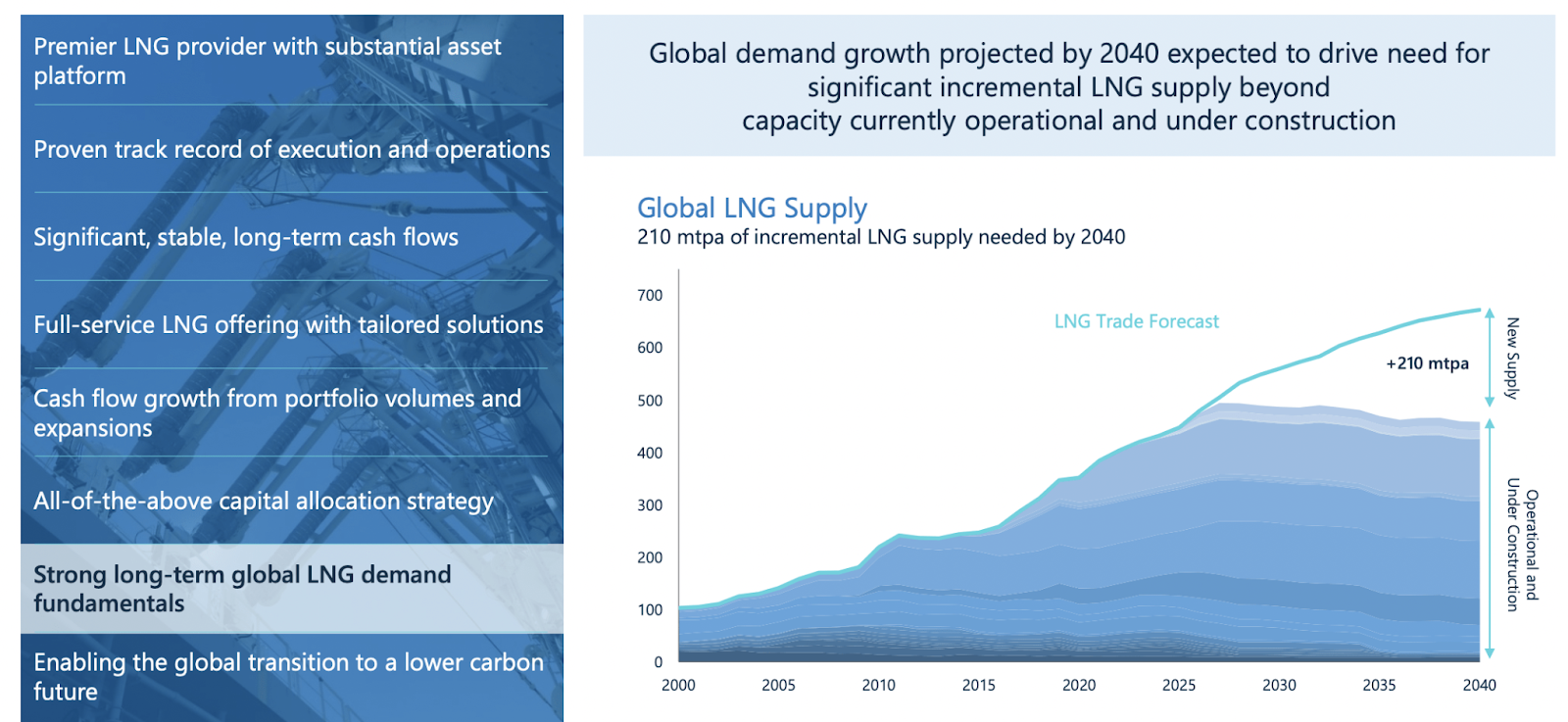

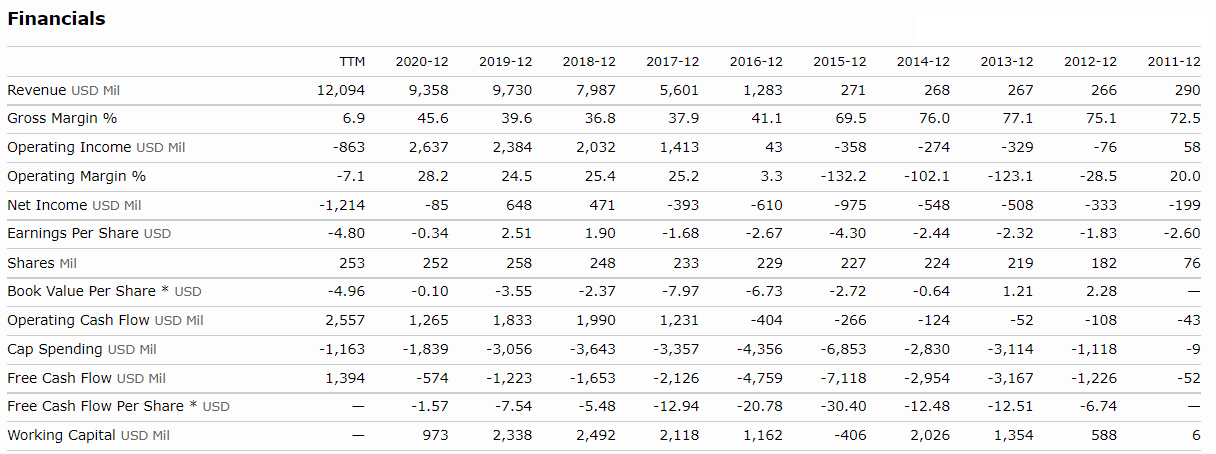

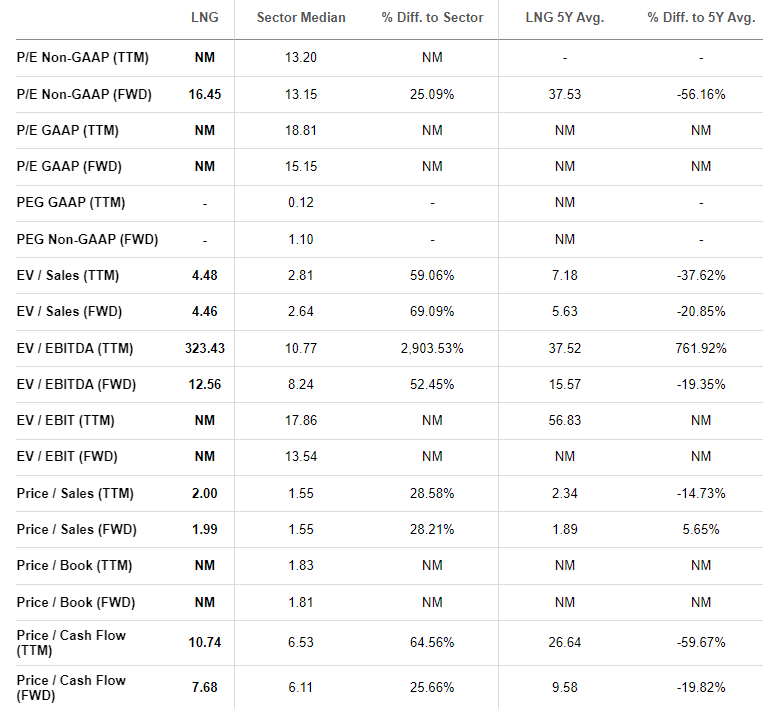

For years, natural gas prices slid lower and lower without an end in sight. Then Covid came. Today, a perfect storm of events has led to severe inventory shortages and supply disruptions, particularly in Europe, sending prices to some of the highest levels in decades. That’s where Cheniere Energy (LNG) comes in. The company is the largest producer of Liquid Natural Gas (LNG) in the U.S. and the 2nd largest in the world. Right now, U.S. natural gas companies are exporting to Europe to take advantage of higher rates, adding to the producers’ bottom lines. As one of the top five Oil & Gas Midstream stock searches by retail investors this month, we expect markets to send the stock higher in the coming months. And it all boils down to the long-term outlook for the company. Cheniere Energy’s Business Based out of Houston, Texas, Cheniere Energy acts as a midstream natural gas company operating a LNG terminal and LNG marketing company. Additionally, the company, through controlling interest in Cheniere Partners L.P., owns and operates the Sabine Pass LNG terminal in Louisiana, North America’s first large-scale LNG export facility. Also, the company owns and operates 94 miles of the Creole Trail Pipeline which connects the Sabine Pass receiving terminal and downstream markets. In the near future, Cheniere intends to construct up to six trains in the Sabine Pass with each having a capacity of 4.5 million tons per annum. Furthermore, the company is developing a liquefaction and export terminal in Corpus Christi Texas. The company prides itself on contracting out 90% of its volume with an average weighted life on remaining contracts of 17 years. LNG is the only pure natural gas export play in the U.S. The company expects demand to rise across the globe as countries push towards cleaner energy, with natural gas being an important part of that mix. Financials A high-level look at the company’s financials doesn’t paint a pretty picture. While revenues have grown substantially, net income and free cash flow have been negative most years. That’s driven by the company’s operations expansion. You can tell because the revenues jumped significantly while operating income turned positive after a few years along with operating cash flow. Additionally, capital spending grew as the company built more terminals and capacity. Now, they’ve moved into more of a money-making mode. Hence, the improvement in margins and cash flows. In the last year, gross margins and incomes dropped while cash flows increased due to a hit the Cheniere took on derivatives it used to hedge natural gas prices. Otherwise, things looked pretty decent this past year and looking forward to the next. We like the high cash flows since the company can use it to pay down its $29 billion in long-term debt and lower interest expenses. Valuation Because of the hits the company took on its derivatives, valuations don’t look amazing. None of these metrics look all that great. Even the price to cash flow ratios aren’t all that amazing. But, let’s go with the company’s adjusted EBITDA for the moment to get a sense of what its future state might look like. While they’ll always have depreciation and taxes, these should decline over time as will interest expenses. FY’22 the company expects to hit around $5.8-$6.3 billion adjusted EBITDA or $23 to $25 per share. At current prices, that equates to a multiple of 4.3x-4.8x. That’s not too shabby. But just as important, the company began to pay a quarterly dividend of $0.33 per share and expects to use cash to pay down $1 billion in debt as well as buyback $1 billion in shares for 3 years. Lastly, as the company expands its operations and achieves scale, margins will continue to improve, setting the stage for future growth. Our Opinion – 7/10 LNG stands to benefit both from higher natural gas prices and expanding operations. While the company has an amazing future ahead of it, we’d prefer to pick up shares below $100 if we can. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |