|

Proprietary Data Insights Financial Pros Surging Stock Searches This Week

|

||||||||||||||||||

|

Earnings Season is Here! And we’re on top of the latest stocks…starting with Netflix (NFLX). To keep you apprised of the happenings, we’ll be including surging stocks in our proprietary data above. Many of these names key in on stocks based on earnings, providing unique insights. So keep an eye out as things are heating up. |

What we’re watching

|

|

Netflix’s subscriber growth is stalling and that has caused a fall in the share price.

|

|

Stock Analysis |

Netflix Hits a Brick Wall |

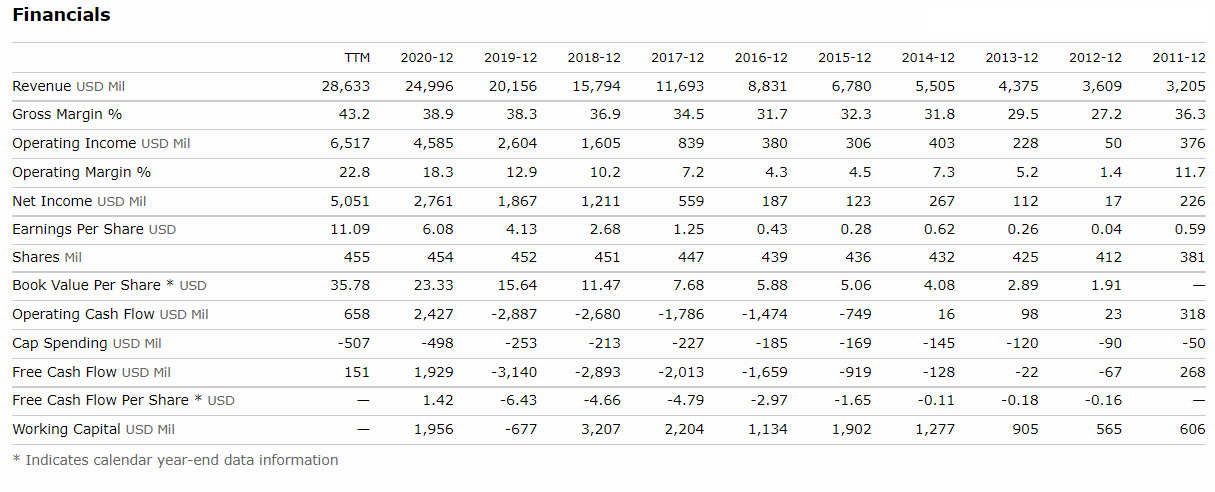

Shares of Netflix (NFLX) fell hard off the company’s latest earnings announcement. Earnings beat estimates by $0.50 at $1.33 while revenue was in line with expectations. But management couldn’t hide the slower user growth and putrid cash flows. Without growth, Netflix is dead in the water. We haven’t taken an opinion one way or another on the company as it’s managed to keep adding subscribers. However, this latest quarter could be the warning shot that could send shares plummeting much further. Netflix’s Business Chances are you have a Netflix subscription or know someone who does. With 221.84 million global paid memberships, Netflix is the largest streaming service in the world. Once a DVD mail service, the company invested heavily in streaming and creating its own content. Its first hits including House of Cards and Orange is the New Black paved the way for a global takeover. Today, the company creates shows in dozens of languages to meet specific niche markets. By geography, the company earns the following in revenues:

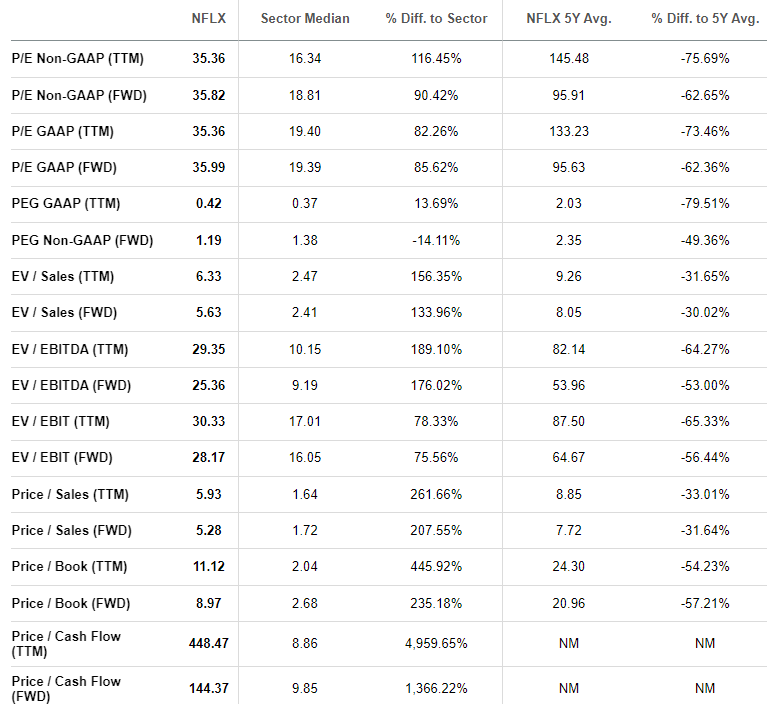

In 2021, Asia-Pacific revenues grew the most at 38% with EMEA up 25%, and the U.S. & Canada as well as Latin America up 13% each. The biggest challenge for the company has been slowing user additions. In 2021, Netflix saw +50% fewer paid member additions than it did in 2020. True, 2020 was an outlier year due to Covid. Yet the additions are nearly 35% lower than 2019’s numbers. For Q1, management guided 2.5 million net additional subscribers vs the 6 million expected by the street. It’s worth understanding the sheer size of Netflix relative to its competitors. At some point, the company will saturate the market. Currently, HBO Max has 73 million subscribers, Disney+ boasts 118 million subscribers (179 million across Disney+, ESPN+, and Hulu), and Paramount+ has 47 million subscribers. Financials In the financials, we want to highlight three key points. First, we want to note the improving gross margins. As they grew, management achieved economies of scale, helping deliver gross margins above 40%. Along those same lines, operating margins improved over time as well. Second, revenues grew at a 10-year average of 27.73%. The latest quarterly report shows YoY quarterly growth of just 16.28%, which has analysts worried. The last point, which we alluded to earlier, was the high cash burn. It’s unusual for a company to turn an EPS profit with negative operating cash flow. That means the company is amortizing assets which will drive up costs for the company in the future. The majority of that spend goes to content development. Lastly, we want to point out Netflix has $14.7b in long-term debt. That’s not a lot given the revenues. But it’s a problem when you have negative operating cash flows. Luckily, the company hasn’t had to issue much debt since 2019. Valuation It shouldn’t come as a surprise that Netflix has some pretty crappy valuations. Yet, given the cash flow issues, we’d expect the P/E ratios to be worse. At ~36x earnings TTM and FWD, they’re expensive but not horrible. However, the company is more expensive than the reset of the sector in nearly every category save one. Although, shares do trade at a discount relative to the 5-year average. That’s not surprising given the growth concerns. Our Opinion – 5/10 If you read analyst downgrades, you’d think Netflix would go belly up tomorrow. Far from it. This company dominates the streaming universe. Recent price increases will help them add to the bottom line. We feel that with prudent management, the company can bring down its debt levels, which currently cost them almost $6b a year. Where do shares get interesting? Below $300. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |