|

Proprietary Data Insights Retail Surging Stocks Last Week

|

What we’re watching

|

|

A look at software manufacturer Unity Software.

|

|

Stock Analysis |

Unity Software 3D Software Sells |

If you were ever inspired by the Star Trek Holodeck, listen up. Software is at a historic inflection point. We’re moving from dynamic algorithms to interfaces we can actually interact with from virtual to augmented reality. It won’t be something that slams into us overnight. But neither did the internet. Software companies that provided SaaS and compatible services won market share over the last decade. It’s why Unity Software (U) stands out in our opinion. The maker of 3D software modeling and development is the purest play on the niche category at the moment. So if you believe in the growth of the new ‘reality’ then this is your ticket. We’ll explain how the company is on the pathway to profitability in a few short years. Unity Software’s Business Unity’s software allows users to create, run, and monetize their content across any device in 2D or 3D. The company’s platform is used for creating and operating interactive, real-time 3d content. Right now, the majority of Unity’s revenue comes from the gaming industry. But that won’t always be the case. The company is working with industrial clients, incorporating CAD and BIM modeling for architects as well as design software for automakers. Recently, Unity paid $1.6 billion for Weta Digital, a visual effects company. The deal brings in 275 technicians, is immediately accretive to earnings in 2022, and expands the company’s addressable markets by $10 billion. Unity offers customers two distinct products:

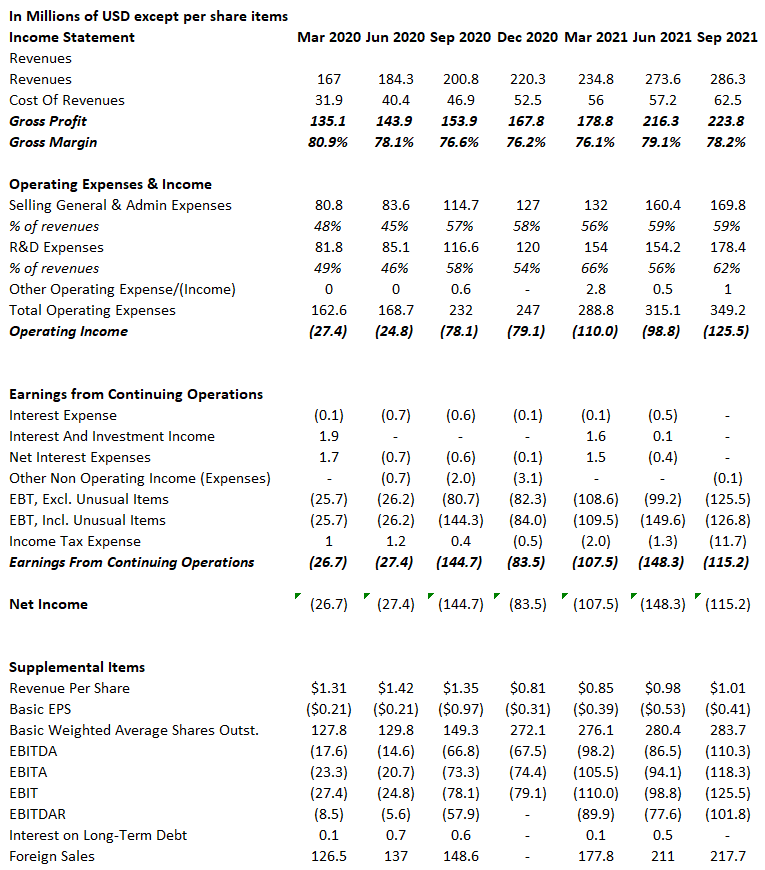

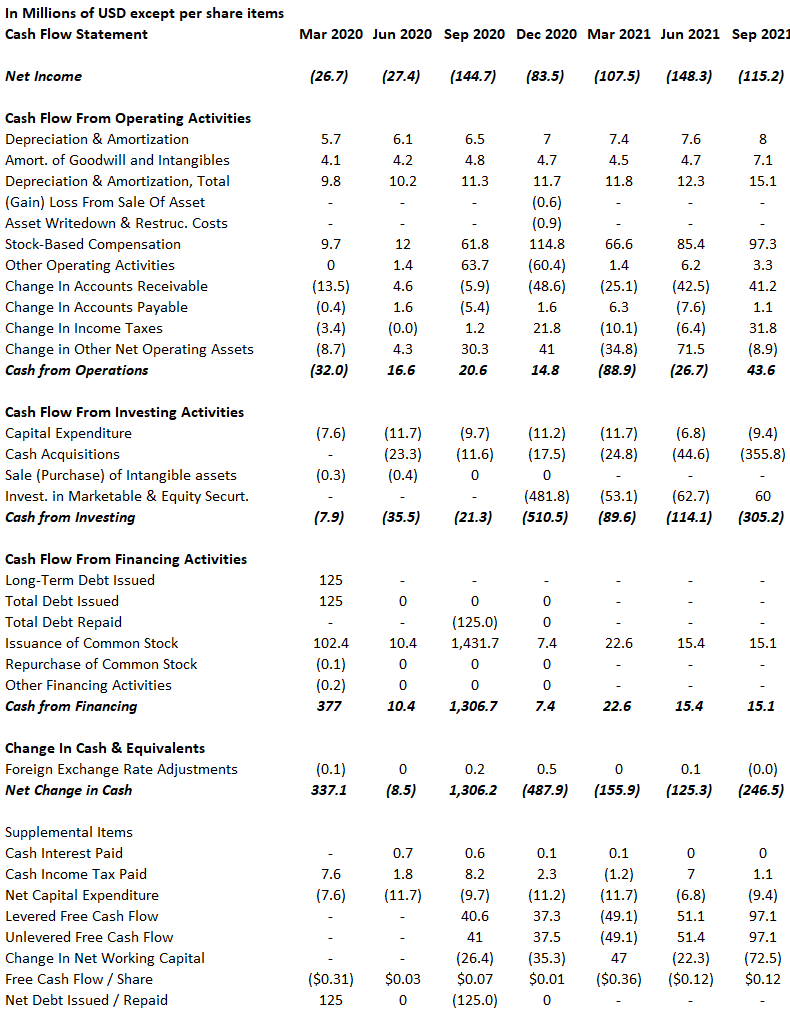

Financials Since Unity only went public in 2020, it’s best to use that as our starting point for the financials other than to note revenues in 2018 and 2019 were $381 and $542 million respectively. Sales continue to grow at a rapid pace, jumping +40% YOY. At the same time, gross margins remained fairly consistent. On the cost side, we see each expense line taking up a larger percentage of revenue each quarter. This is the largest issue facing the company and an uphill battle. However, we want to highlight Unity’s cash flows. Most quarters, the company is able to generate positive cash flow from operations and has little in the way of capital expenditures. As they hit growth in the coming years, we expect expenses as a percentage of revenue to drop and cash flows to improve markedly. Valuation Since Unity doesn’t turn a profit, most valuation metrics don’t work here. However, we want to point out the company trades at ~25x this year’s sales. That is expensive. However, this stock was trading at 40x those same sales just a few months ago with little that changed fundamentally for the company. Our Opinion – 8/10 Unity is an interesting speculative investment. We can see them hitting positive cash flow regularly by 2023. We expect a lot of volatility in share price and could easily see this trading down as low as $60. So, if this is a stock you’re interested in, take that into account. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |