|

Proprietary Data Insights Retail Surging Large Cap Stocks Last Week

|

What we’re watching

|

|

A look at Encore Wire, which is delivering record profits.

|

|

Stock Analysis |

WIRE your portfolio |

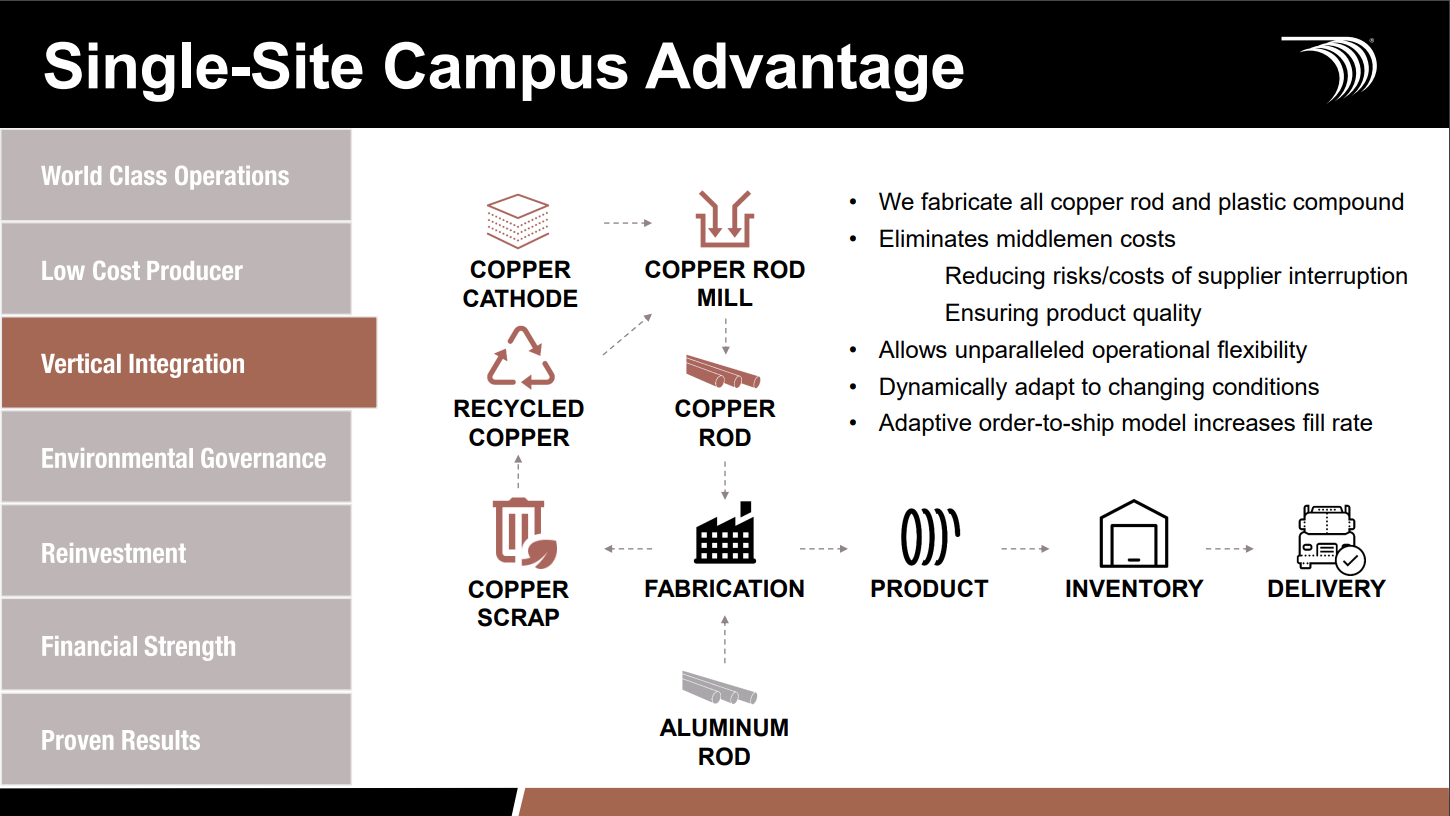

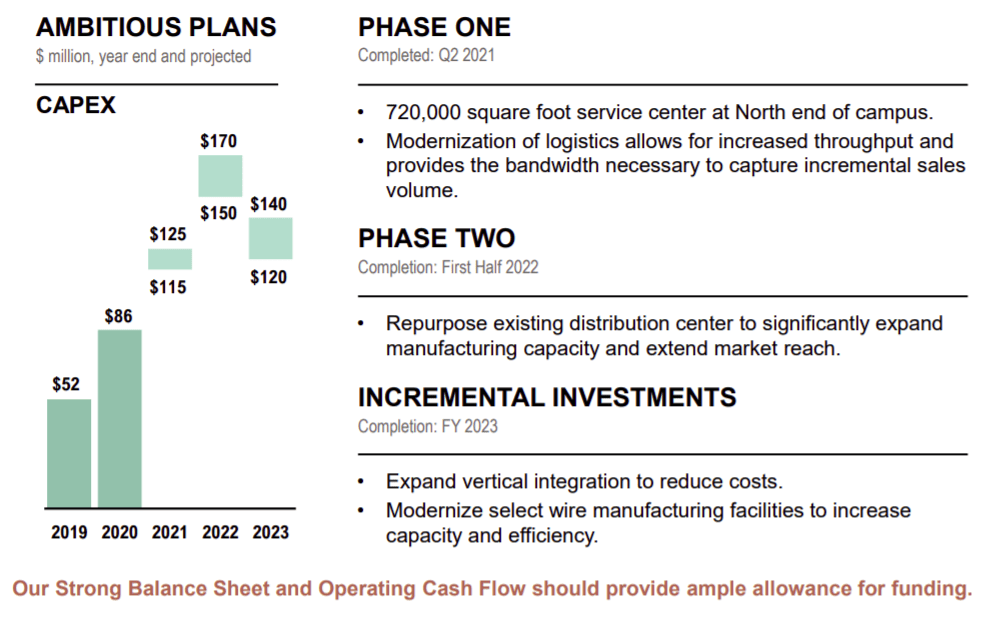

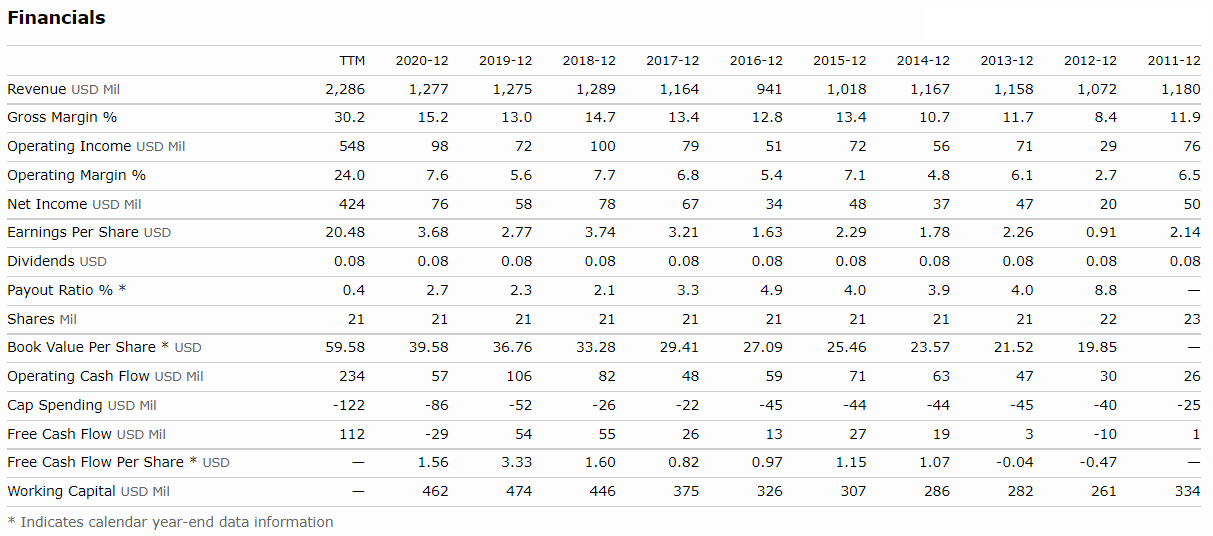

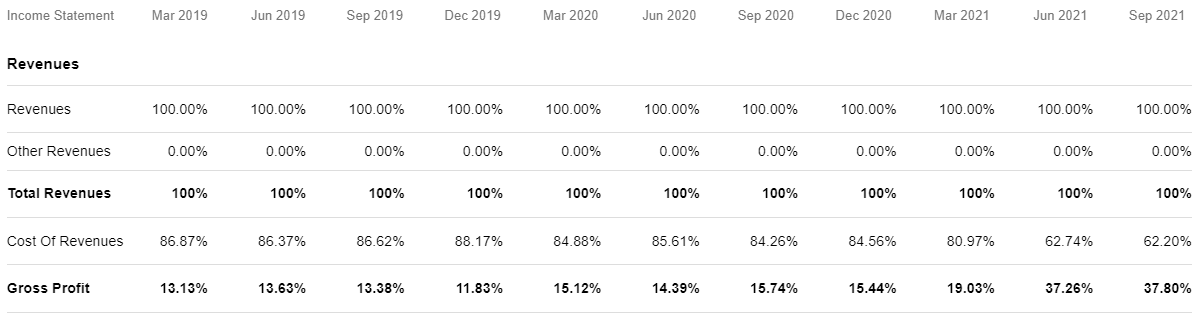

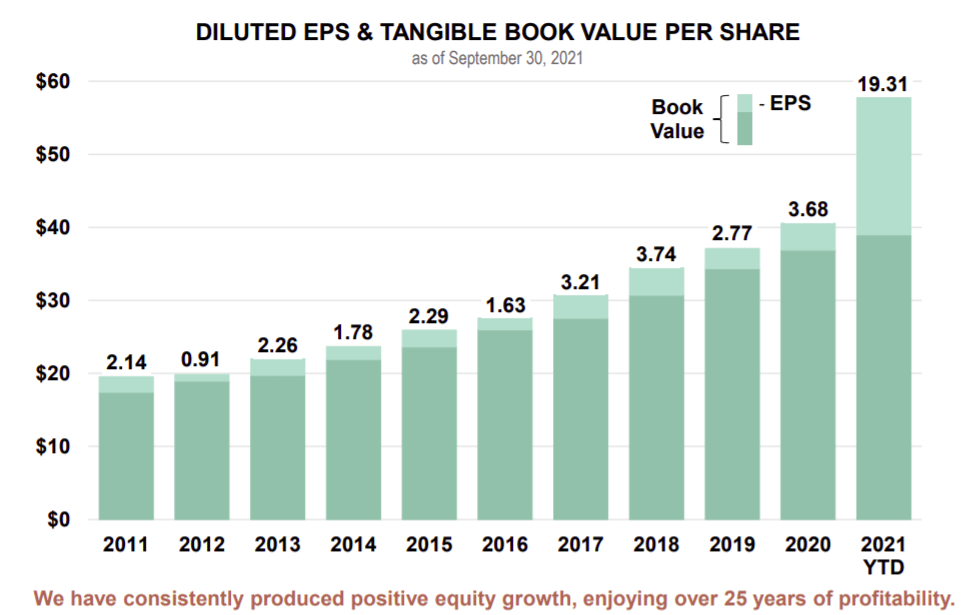

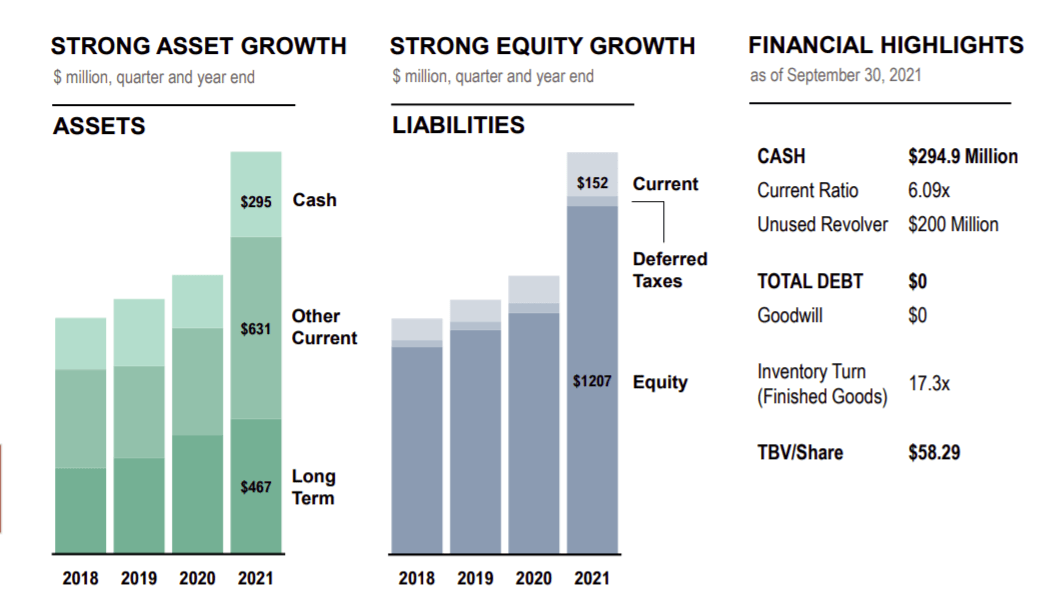

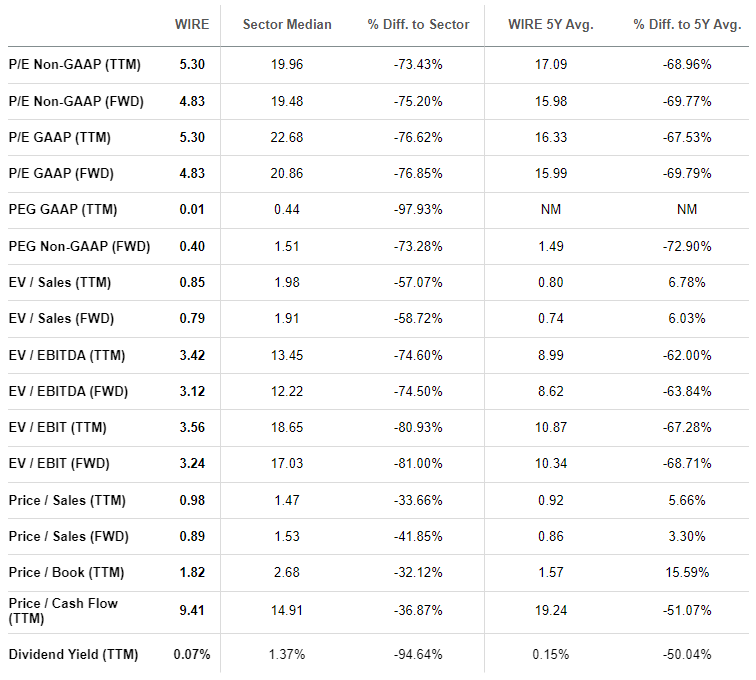

Construction spending is set to surge in 2022. A massive infrastructure spending bill begins to dole out money on top of demand for everything from housing to manufacturing capacity at record levels. Suppliers who feed this industry stand to make a bundle, assuming they can control their input costs. Encore Wire (WIRE) makes electrical wire and cable for everything from commercial to residential buildings. And you would think that copper costs would hurt Encore, driving up input costs. Yet, the company is managing to deliver record profits. And that is set to continue for one specific reason: Encore Wire’s Business Encore bills itself as a low-cost manufacturer of electrical building wire and cable. The Company is a significant supplier of building wire for interior electrical wiring in commercial and industrial buildings, homes, apartments, and manufactured housing. Pretty simple business right? We noted that copper prices were a huge input cost for Encore. What we left out was that copper wire itself, the sales price, is a commodity in and of itself. The spread between raw copper input costs and the sales price of copper wire has increased by 181.1% since last year. Wire prices increased by 91% while copper prices increased by 55%. With construction demand through the roof and unlikely to subside, we expect wire prices to continue its upward trajectory. Encore works to keep its costs low through a vertically integrated operation. Along those lines, the company has a two-phase expansion plan they laid out in the last earnings call. In mid-May, the company opened a new service center. Additionally, Encore is repurposing a disruption center to expand its manufacturing capacity, which is scheduled to open in 2022. The company plans to continue spending Capex, to take its business beyond basic organic growth. Financials As we noted earlier, the spread between input and sales price led to some of the best margins in the last decade. On a quarterly basis, you can see how gross margins exploded in the back half of 2021. But, what’s also critical to understand is how WIRE consistently grew earnings year after year Along with the better earnings, Encore created a fortress balance sheet with little debt and an excellent cash position. Valuation With record margins, Encore’s valuation metrics look fantastic relative to the rest of the sector and many of its 5-year averages. The price-to-earnings ratios (P/E) are ridiculously cheap at 5.3x TTM and 4.83 forward earnings. Even the price to sales is less than 1x which is cheap for any industry. Probably the least appealing metric is the price to cash flow of 9.41x, which is still pretty darn good. Our Opinion – 7/10 While we think WIRE is a fantastic company with a great outlook, its technical picture looks a bit precarious. That’s why we’d be more interested in shares down near $80. Otherwise, we’d be at 10/10. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |