|

Proprietary Data Insights Retail Surging Apparel Stocks Last Week

|

What we’re watching

|

|

A look at Levi Strauss who have posted only one loss in the last 8 years.

|

|

Stock Analysis |

Delightful Denim |

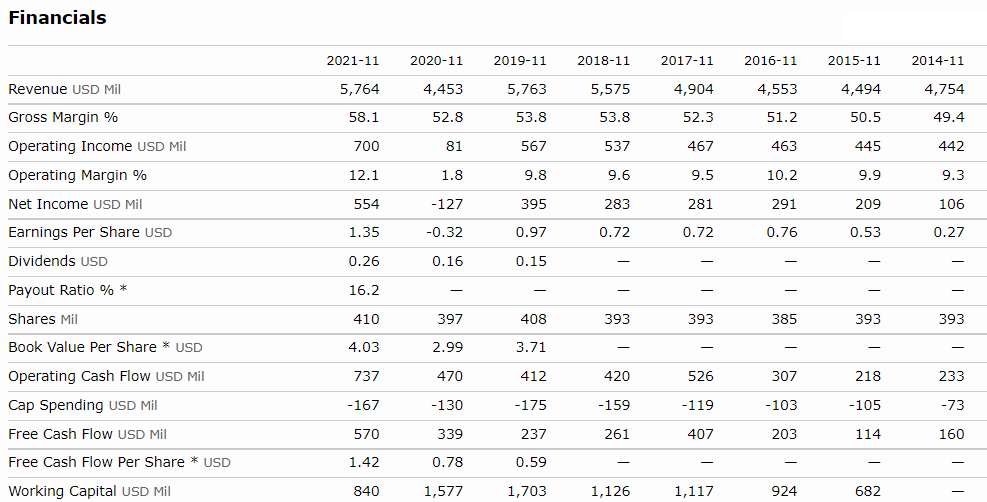

Few brands hold the history of Levi Strass (LEVI) jeans. Notably, the company posted only one loss in the last 8 years (2020). After the company released earnings last week, the stock’s searches amongst retail investors for apparel companies surged 239%, marking one of the most dramatic increases in search volume in the last several months. This is particularly interesting given Levi’s stock isn’t a momentum name nor actively traded. In fact, it’s most well-known amongst value investors. Given the intrigue, we dug into the company’s financials and trading history to see what we could find. Levi Strauss & Co.’s Business Most of us know Levi Strauss for the Levi’s brand denim jeans. What you may not know is that the company also owns Dockers and Denizen. That said, jeans are the company’s main revenue generator. Geographically, the company is well-diversified with 55% of its sales coming from the Americas, 29% from Europe, and 16% from Asia, the Middle East, and Africa. Note: The last presentation available is from 2019. However, the general category performance is roughly the same with the exception of e-commerce accounting for nearly 8% of total sales now. Recently, the company has shifted its focus to three core ideas.

In the most recent quarterly earnings call, management noted that demand for products outstripped supply by $50 million or 3% of revenue due to supply chain constraints. They also noted that the company locked in 2nd half cost of goods sold slightly higher than 5%. However, the company continues to raise prices to handle this, guiding for gross margins in 2022 of 0.15%-0.30% higher than 2021. Financials We want to start by noting that the company issued guidance for 2022 of net revenue growth of 11%-13% or $6.4-$6.5 billion and adjusted diluted EPS of $1.50-$1.56 compared to $1.47 for 2021, which we’ll discuss more in the valuation section. Turning to the broader financial performance, we want to go back to the consistency of the company’s revenue and earnings growth over the last 8 years. While not massive, the company’s 3 year growth rate prior to 2020 was around 8%. YOY revenue growth in 2021 came in just shy of 30%. What’s also notable is the EPS 5-year average in 2019 was 29.17%. Today, the company boasts gross margins close to 60% with cash flows more than 50% higher than its best years. Lastly, we want to point out the company carries about $1 billion in long-term debt and another $969 million in capital leases compared to $902 million in cash and about $898 million in inventory. This tells us management has ample room to invest in digitization and omnichannel growth. Valuation Compared to the rest of the consumer discretionary sector, Levi’s stock isn’t all that cheap, nor is it ridiculously expensive. While forward estimates for non-GAAP P/E are a bit higher than the sector average, the price to forward cash flow is much better. Taken as a whole, cash flows are the best asset for the company while earnings are a bit of a drag. However, that’s largely due to the higher growth rates for Levi’s compared to the sector. Both trailing and forward-looking revenue growth rates exceed the sector and blow away the company’s 5-year average. The forward-looking earnings growth rates overstate things a bit as the adjusted EPS growth is only supposed to hit 6% at the top end. Technical Picture Taking a look at the weekly chart, we find a stock that’s in a clear downtrend coming off the highs it put in last spring. The two support levels that caught our eye come in at $20 and $16.50, the latter being an ideal location to build a position. Our Opinion – 7/10 We like this stock and want to keep it on our watchlist. It’s just a bit overpriced at the moment. That’s why the $16.50 support area makes a lot of sense from a technical and fundamental point of view. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |