|

Proprietary Data Insights Financial Pros Top Auto Supplier Stock Searches Last 30 Days

|

What we’re watching

|

|

Goodyear’s results beat expectations, yet the stock still cratered 27%.

|

|

Stock Analysis |

Goodyear’s Selloff Creates Opportunity |

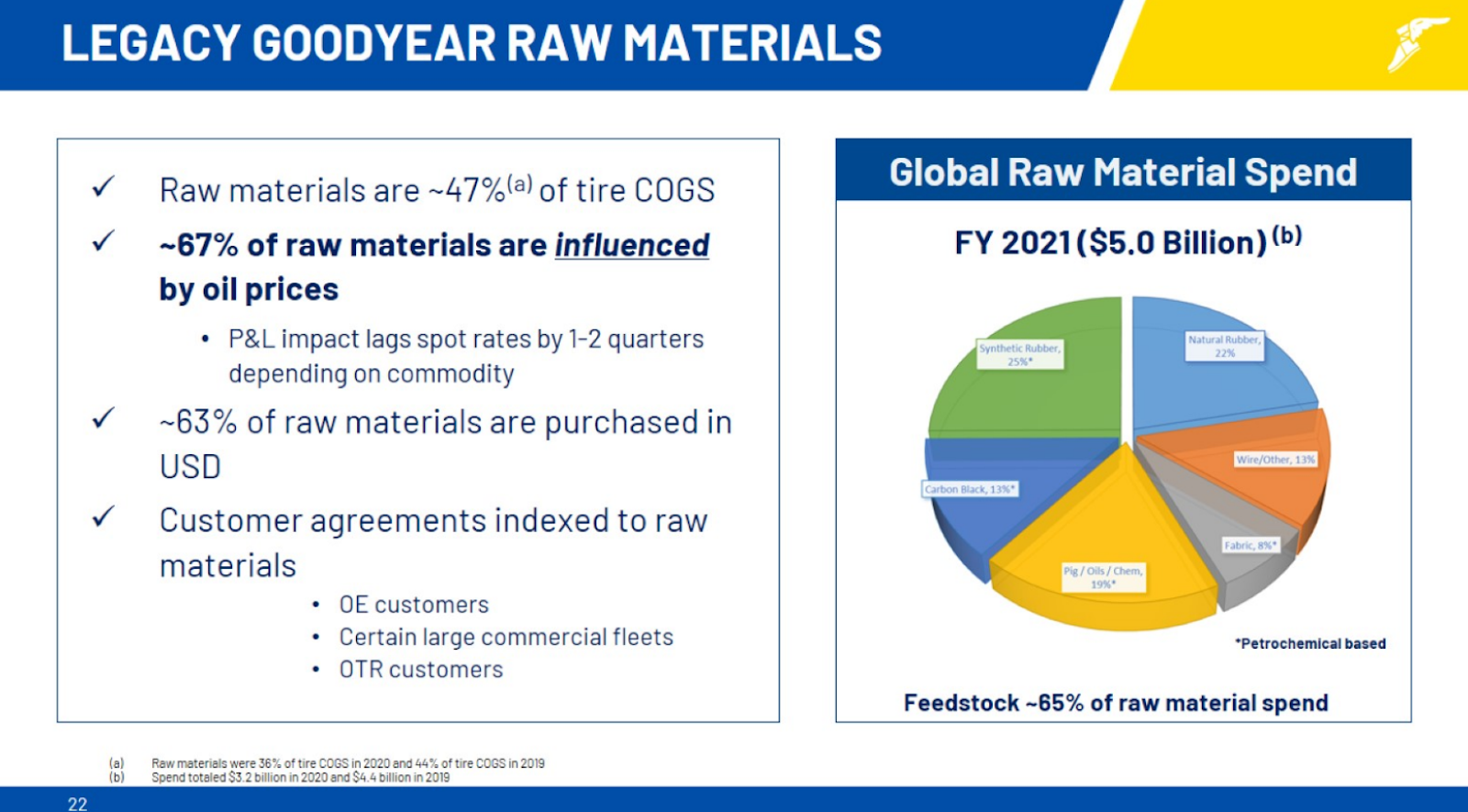

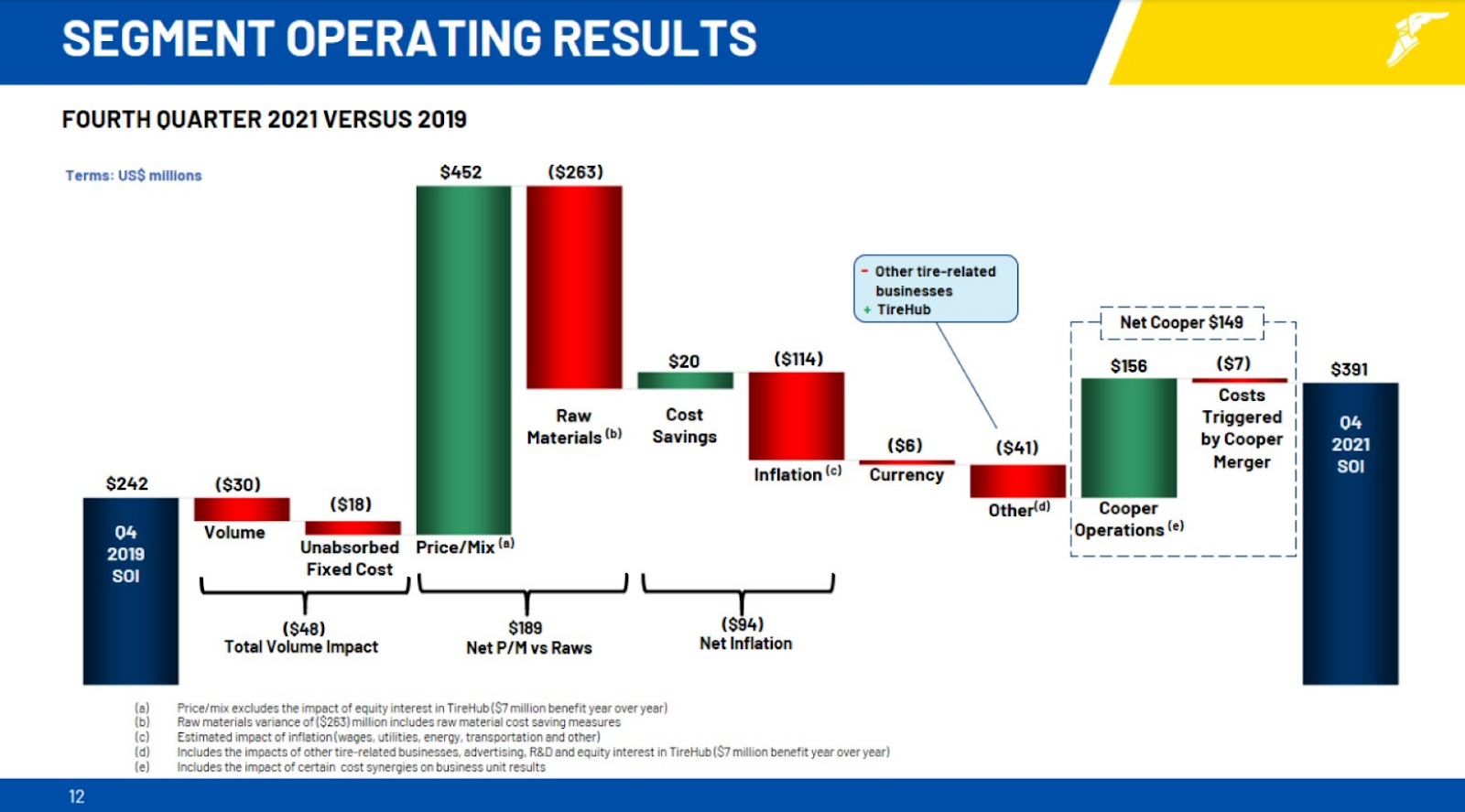

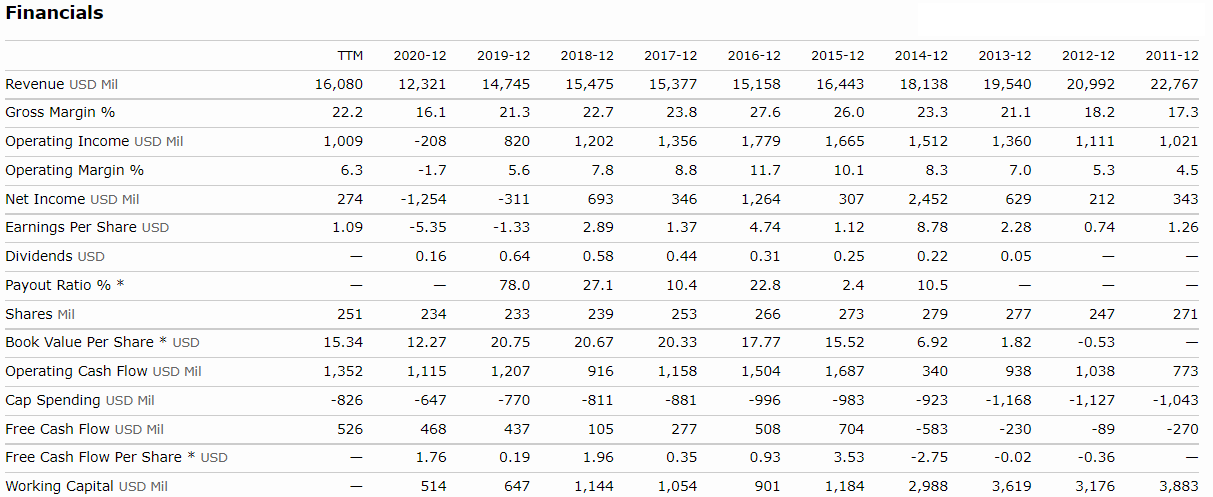

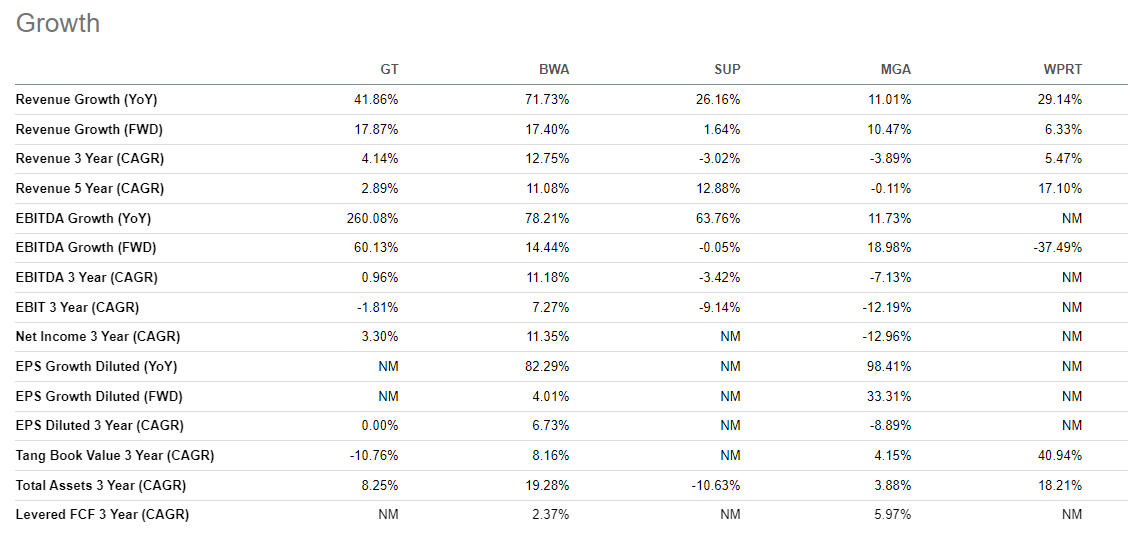

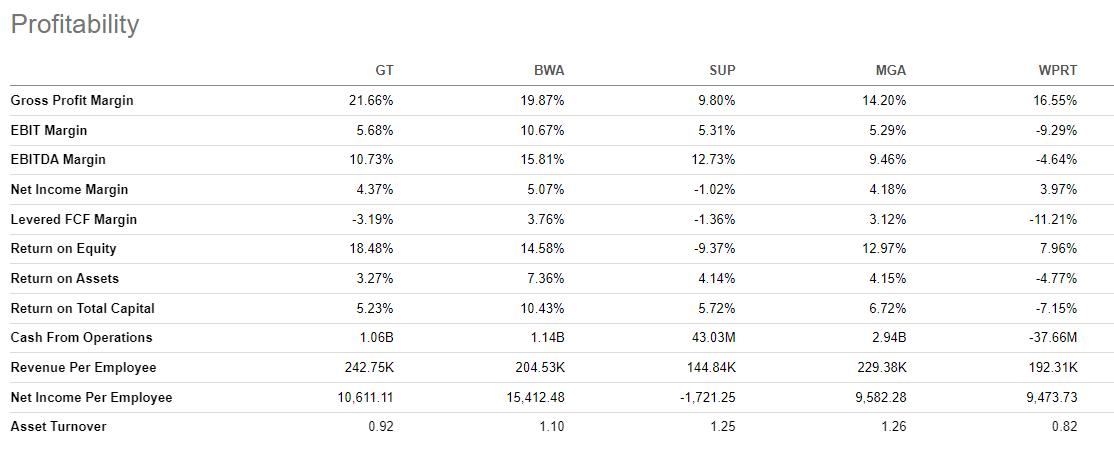

Markets can be unforgiving. Goodyear Tire & Rubber (GT) reported earnings and revenues that beat expectations. Yet, the stock cratered 27%. JP Morgan analysts just came out stating the selloff was overdone. We agree. Goodyear Tire doesn’t see price movement like this often if ever. We also see further evidence of interest by the surge in searches by financial pros for the company of 30x the typical volume! Our analysis below digs into what the company does along with its financials, what ‘caused’ the selloff, and why we see a ton of potential here. Goodyear Tire’s Business Following the company’s acquisition of Cooper Tire, Goodyear became one of the largest tire manufacturing companies in the world. You’ve probably heard of some of the company’s brands including GoodYear and Dunlop Tires. Besides consumer tires, Goodyear manufactures and sells tires and related products to a host of industries from aircraft to farming equipment. In 2019, Goodyear entered into a joint venture with Bridgestone to form the largest tire distribution network in the U.S. Back in June of 2021, Goodyear finalized its merger with Cooper Tire, strengthening its leadership in the industry. Goodyear’s business is broken down by geography with the Americas accounting for 53% of revenues, EMEA 32.2%, and Asia Pacific 14.6%. Now, if you weren’t aware, the raw materials that go into are heavily influenced by the price of oil. Financials That’s why the company expects raw material costs to increase $700-$800 million in the first half of 2022, net of savings. You can see the impact in the Q4 results. The good news is that pricing will continue to help keep margins from collapsing through 2022. However, management forecasts breakeven free cash flow in 2022. You can actually see how margins improved in 2014 as the price of crude oil dropped when global supply increased. General revenues dropped off during that same period before bottoming out in 2020. However, the company continued to deliver solid operating and free cash flow. So while it is disappointing the company won’t deliver positive free cash flow next year, it’s not the end of the world. Lastly, we want to highlight the long-term debt and liabilities which come in around $10.4 billion. That’s a bit heavy considering they only carry $1.2 billion in cash. However, that’s jumped in part due to the recent acquisition of Cooper Tire. Valuation There aren’t too many tire manufacturer stocks out there. So instead, we’ve created a comparison between Goodyear and several other car part suppliers. Though not an exact comparison, they all tend to live and die by the cyclical nature of car and truck buyuing. Across nearly every measure, Goodyear Tire comes out as the cheapest. Given the higher raw material costs for 2022, it’s not surprising to see a higher price to earnings ratio forecasted. One interesting point not included here is GT’s forward price to cash flow ratio of 2.61x. While that’s extremely attractive, keep in mind the company plans for breakeven free cash flow in 2022. Turning to growth measures, we wanted to focus more on the forward looking metrics. Specifically, the forward EBITDA growth for GT tops all its competitors by a mile as does it’s YoY EBITDA growth. But what we found most striking was the profitability measures. You see, most of these suppliers operate in very different areas. Some make parts for the car’s mechanics while others create fuel systems. And Goodyear makes tires. Yet, Goodyear had the best gross profit margin despite a run up in raw material prices. Now, we aren’t as impressed with its EBIT and EBITDA margins. However, Goodyear’s net income margin came in second place, which is a positive sign for shareholders. Our Opinion – 7/10 We expect markets to fully price in the raw material costs for Goodyear in the coming months. However, auto demand remains strong and oil prices will eventually fall. We expect 2022 to be a tough year for the company, while 2023 onward should see benefits from the merger with Cooper Tire as well as pricing improvements. Ideally, we like shares around $14.50. This may not be a stock you jump into at this exact moment. But as we approach the second half of the year, this is one to keep on your watchlist. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |