|

Proprietary Data Insights Financial Pros Surging Midcap Stock Searches Last Week

|

What we’re watching

|

|

Freelance work platform Upwork has a great opportunity to soon turn an earnings profit.

|

|

Stock Analysis |

Upwork down >60% – Is it a Buy? |

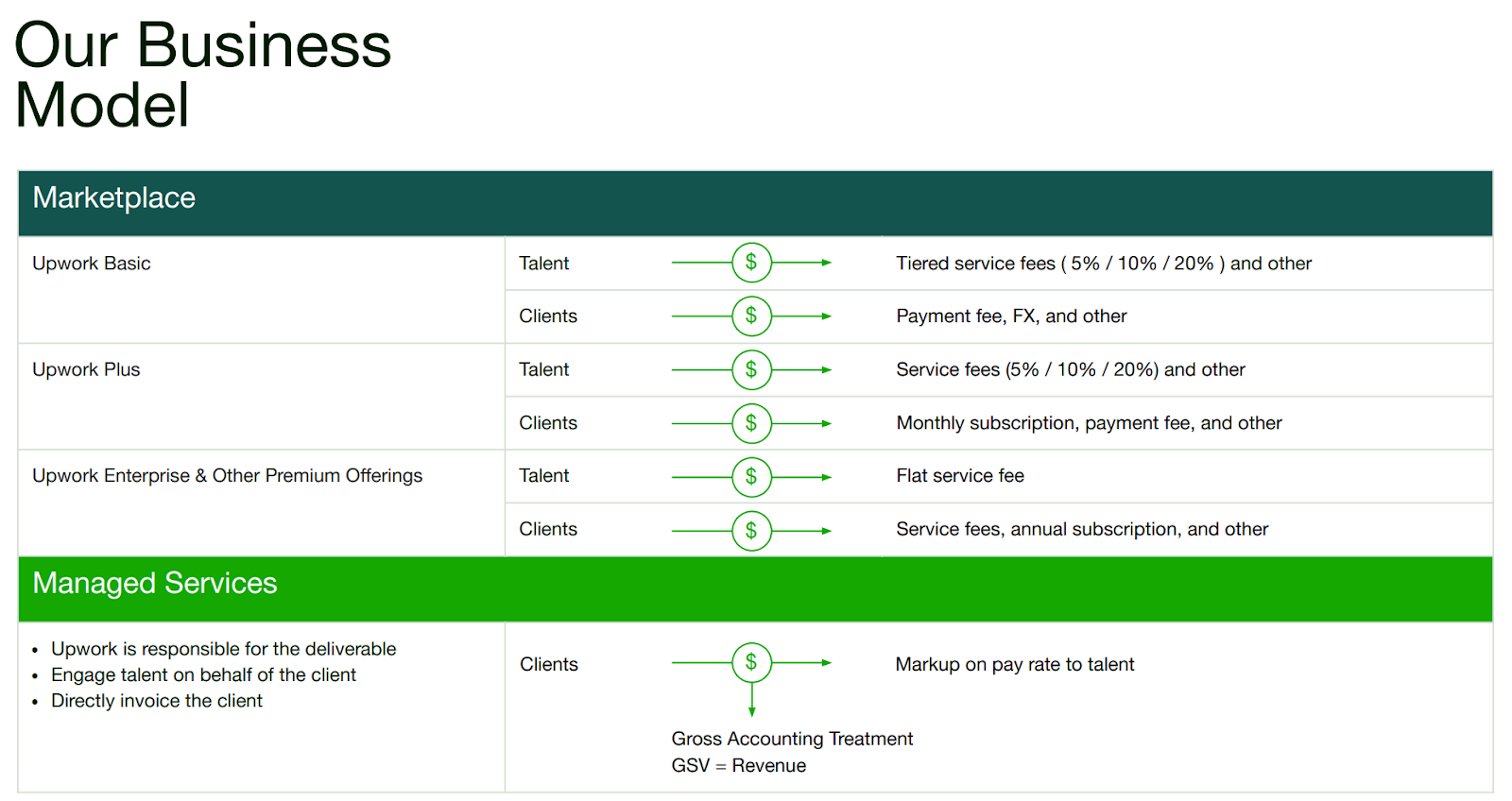

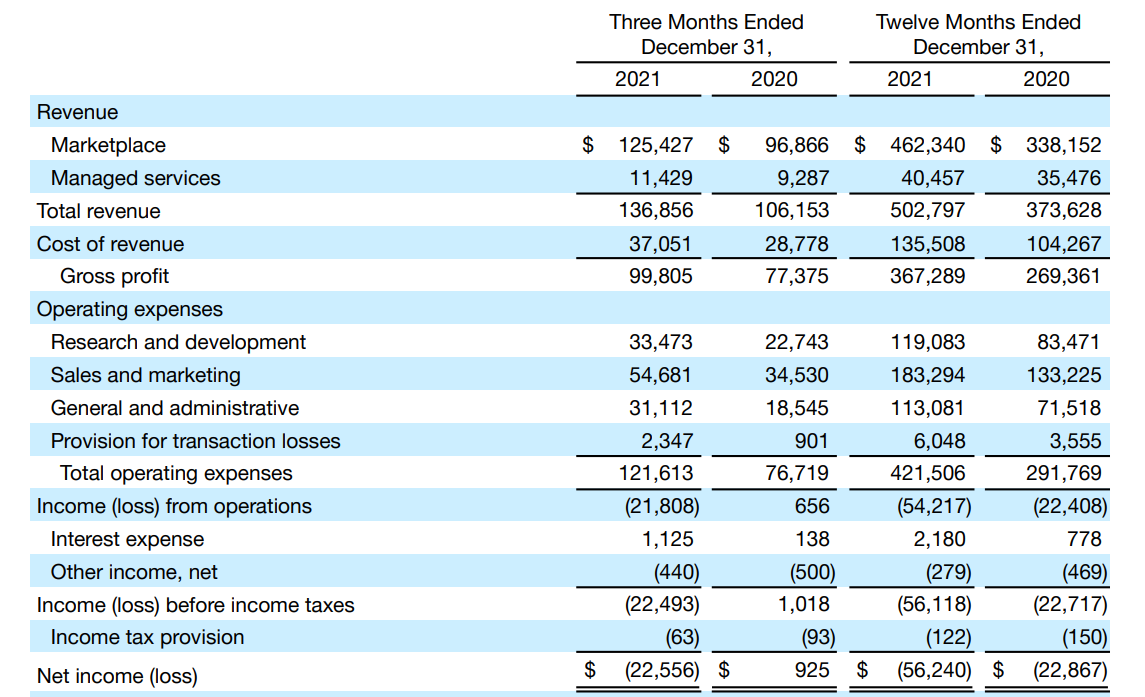

Upwork (UPWK) is sooo close. With workers flipping jobs like pancakes and many choosing to go solo, this freelance platform sits at the precipice of something huge. You see, freelancers are great for businesses with small projects. Rather than hire a large firm, one or more freelancers can provide the same services with personal attention. While the company hasn’t turned an earnings profit yet, it’s managed to grow operating and free cash flow at a rapid rate. This implies overall profitability is just a matter of time. But that’s not why we caught up with this stock. After reporting earnings, search volume for the ticker amongst financial pros surged 700% in a week. That might not seem like a lot. But for a midcap stock, that was enough to put it in 3rd place amongst surges by financial pros. It stood out specifically because of the surge on a stock with negative EPS. And that got us curious as to why. Upwork’s Business With its subsidiaries, Upwork operates an online freelance marketplace where people looking for work and those looking for workers connect. The platform allows freelancers to post their portfolios, resumes, as well as bid on various projects and jobs. Job posters can view different bids from freelancers, communicate with them, and select amongst candidates. Upwork provides tracking and billing services as well as communication, allowing freelancers and clients to set up a one-stop-shop on their platform. The company’s closest competition, Fiverr (FVRR), takes a slightly different approach. Where Upwork allows for more of an auction style connection between job seekers and clients, Fiverr lets freelancers post their work, prices, and resumes for clients to find. Upwork’s freelancers and clients span the globe, reaching from the U.S. to India and everywhere in between. The company earns money in a few different ways.

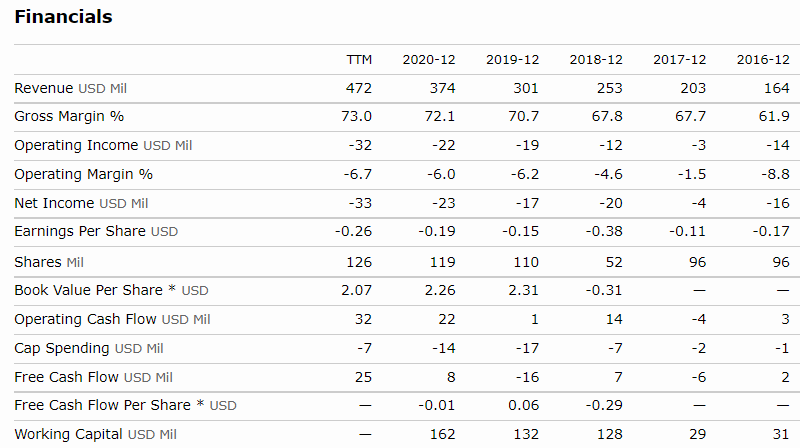

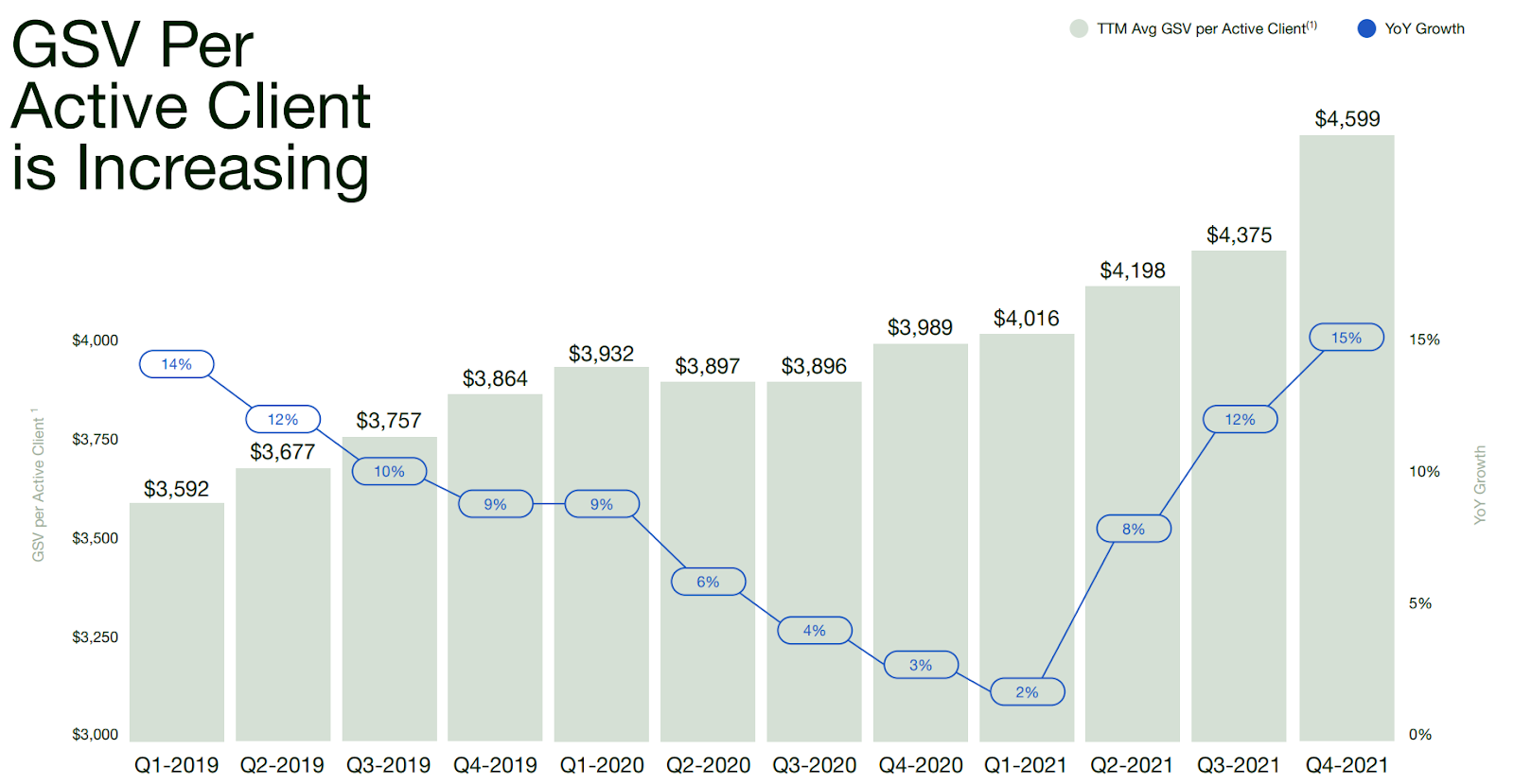

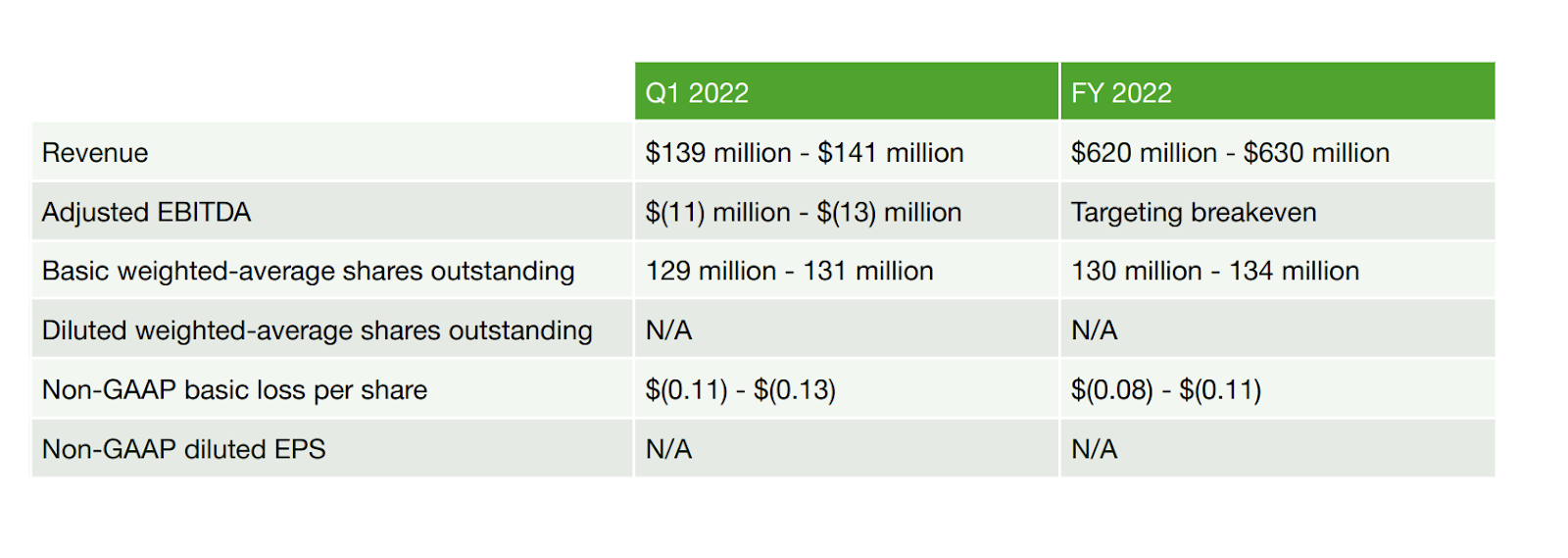

This is all part of the Upwork Marketplace. Managed services allows clients to hire Upwork to find the talent and directly invoice the client. Currently, marketplace revenue accounts for nearly 92% of the revenues. Financials In the latest 2021 results, total revenue jumped 35% with marketplace revenue up 37% and managed revenue up 14%. That’s a solid get considering the 5-year average revenue growth is only 22.64%. Turning to the financials, it’s apparent Upwork hasn’t turned an operating profit yet. Why is that? The biggest expense hurdles the company faces are the sales and marketing costs. Right now, those account for ~36% of revenues. And from 2020 to 2021, G&A expenses increased from 21% to 24.5% of revenues. And based on the latest earnings results, it doesn’t appear that will change anytime soon. The company is expected to increase marketing spending from $47 million to $80 million in order to increase brand awareness. That’s why Gross Sales Volume (GSV) per active client and customer retention are so crucial. Upwork needs to keep pushing this up to generate more revenue from existing clients which require little to no additional marketing. Additionally, Upwork provided guidance that the company expected breakeven EBITDA and total revenues roughly 31.3% higher than 2021.

Lastly, we want to highlight the balance sheet. The company has $588 million in long-term liabilities compared to $697 million in cash. That gives them plenty of flexibility to spend where they need.

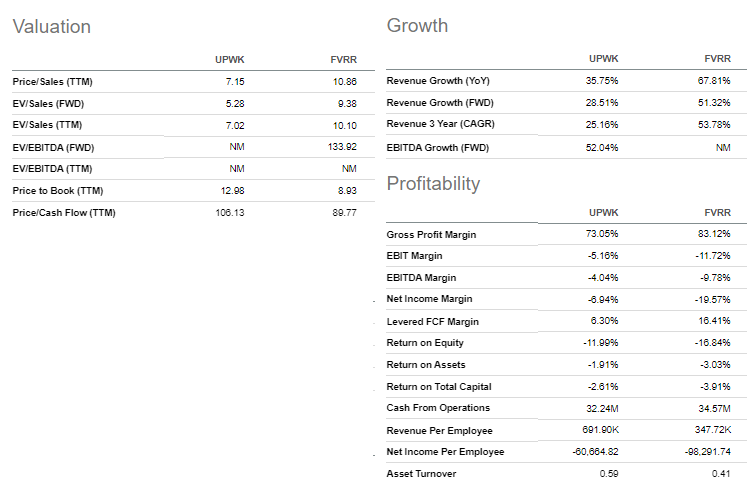

Valuation For our valuation section, we wanted to compare Upwork to its closest competitor Fiverr. Now, since neither turns a profit, we’ve cut the metrics down to the most relevant ones.

Revenue growth for Upwork isn’t nearly as robust as Fiverr. However, Upwork does twice the total sales. That explains part of why Upwork has a better price to sales ratio and forward looking enterprise value to sales ratio. Fiverr also has a notably higher gross profit margin that has risen over the past 5 years. While neither company has a particularly great price to cash flow ratio, Fiverr’s is a bit better. Our Opinion – 5/10 It’s tough to get behind a company that doesn’t have an obvious pathway to profitability. Many high growth companies don’t turn a profit for years as they build out their business. However, we tend to see growth rates of +50% on that kind of business. And the current price to cash flow ratio is just too poor to ignore. Upwork makes a good speculative play. But we would want it at sub $10 before considering it. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |