|

Proprietary Data Insights Financial Pros Top Small Cap Specialty Retail Stock Searches This Month

|

What we’re watching

|

|

A look at The Container Store which has had a huge fall in price since it went public in 2014.

|

|

Stock Analysis |

This Store Barely Contains its Profits |

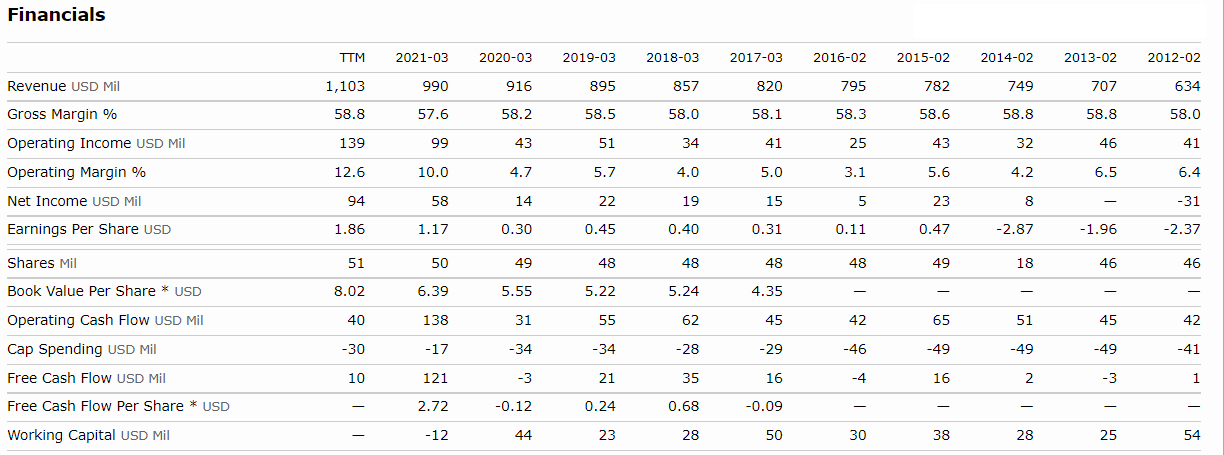

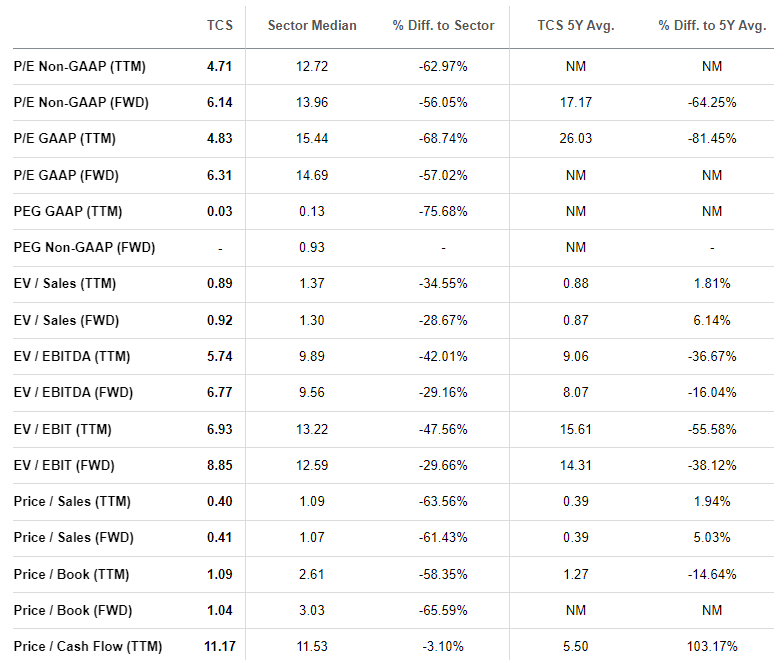

Marie Kondo is the kind of person you love to hate. You shouldn’t want to watch someone organize another person’s home… And yet you can’t look away. Now a worldwide sensation, Kondo sells an exclusive line of organizational products at The Container Store (TCS). If messes make you anxious, then be prepared to spend hundreds to thousands of dollars just ‘browsing’ through their aisles. Serving the niche market of home and office organization, The Container Store went public back in 2014. Since then, shares have tumbled from $45 to $8.65. That’s pretty absurd considering the company earned a whopping $1.86 per share in the past year. So why is it the second most searched small cap speciality retailer by financial pros is trading at historically cheap prices? Let’s find out. The Container Store’s Business Despite intense competition from larger retailers such as Target (TGT), Walmart (WMT), and other furniture retailers, The Container Store holds a special place in the hearts of organizational enthusiasts. The company focuses on providing storage and organization products and like solutions to customers in the U.S. With nearly 100 stores in operation, TCS offers brands like Elfa, Avera, and Laren. Revenue is split roughly 50/50 between general merchandise and custom closets. Recently, the company acquired Closet works for $21.5 million, which enhances TCS’ offerings for custom closets, garages, home offices, pantries, laundry rooms, and Murphy beds. This comes as part of TCS’ effort to double its sales to $2 billion. The majority of that is expected to come from opening 100 new stores in the coming years while doubling down on custom closets. Financials Historically, TCS has struggled to find revenue growth. It took the company a decade to get close to doubling its revenues. However, gross margins held steady while operating margins expanded dramatically in 2021 largely due to a drop in depreciation and SG&A expenses. Additionally, cash flow increased in 2021 before contracting in recent quarters. In the recent earnings report, management provided forward guidance of a sales decline of 6% net and 11% when you include a difference in total calendar days. And, they expect to hit EPS of $0.24 for Q4. It was quite disappointing in the most recent quarter to see negative operating cash flows of $7.0 million driven largely by an increase in SG&A costs and a decrease in gross margins. That’s not entirely surprising given the inflationary pressures. Lastly, we want to highlight the company’s total long-term liabilities of $570 million. That’s fairly high relative to the $19 million in cash. So, the company will need to focus heavily on generating cash and borrowing if it wants to open additional stores. Valuation While growth and profits have been a bit lumpy, there’s no denying the stellar valuation for the current share price. There’s no denying the cheap price-to-earnings ratios look back twelve months and forward. In fact, TCS is cheaper than the sector in every single category. The only spot it barely keeps up with is the price to cash flow. Yes, forward earnings aren’t expected to do as well. However, management hasn’t provided much on 2022, so there’s a lot of educated guessing in these numbers. And if the company is planning to strategically push more custom closets, we could see it spending heavily in the first half of the year. Our Opinion – 7/10 The Container Store is coming off a banner year. However, they face inflationary pressures and supply issues. Plus, they don’t have a lot of cash to invest. However, last quarter’s cash flow draw is likely a blip. And management seems eager to push higher margin custom closet business. With the latest acquisition closing in December, we’ll be interested to see how the results shake out in the coming quarters. But this is definitely a stock we are interested in. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |