|

Proprietary Data Insights Financial Pros Top App Co. Stock Searches This Month

|

|

Stock Analysis |

Could UBER Be At The Cusp of Greatness? |

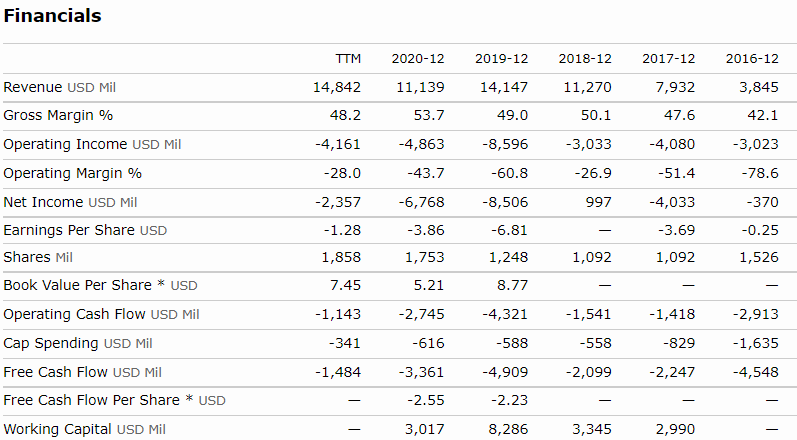

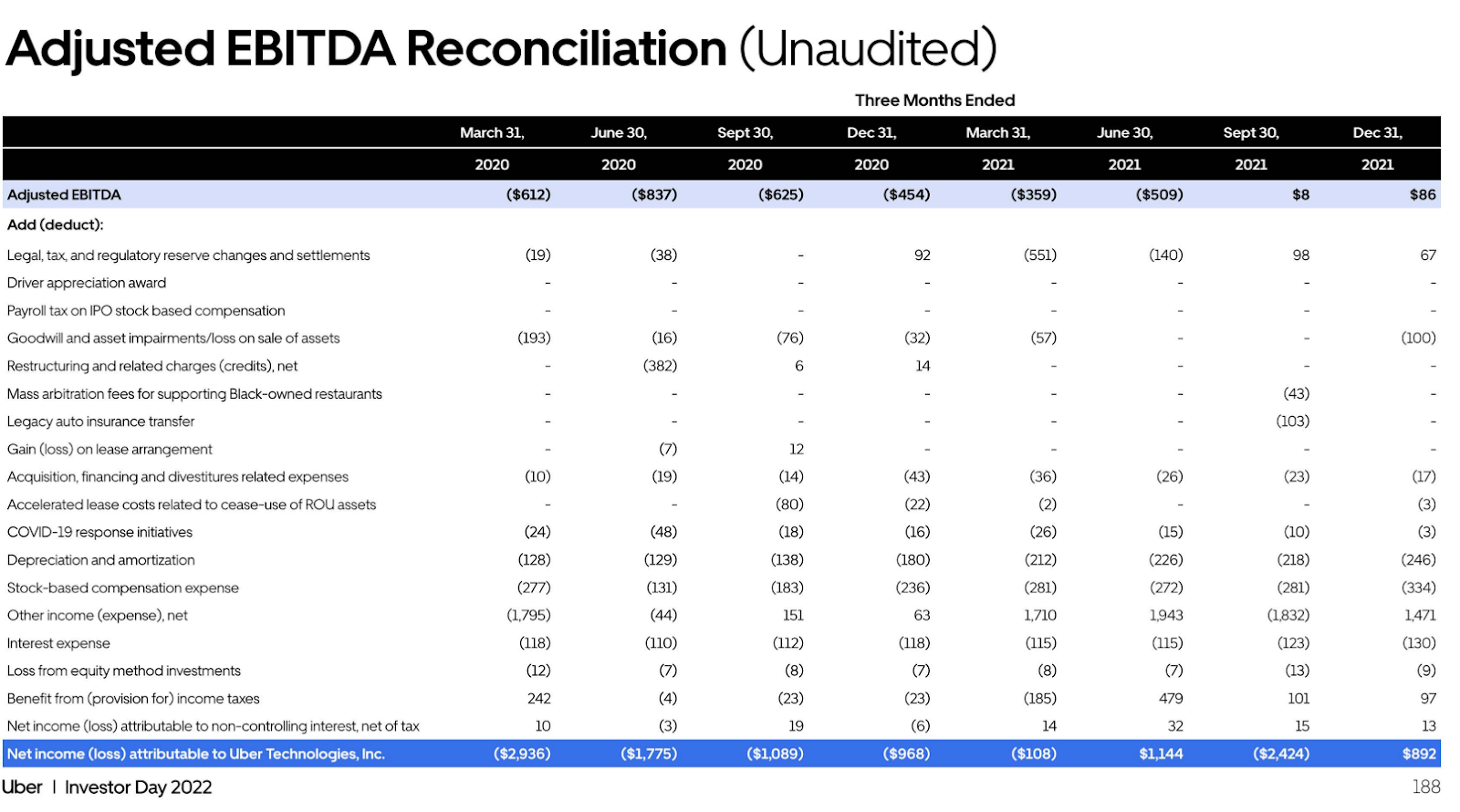

Look up ‘disappointing investment’ in the dictionary and Uber (UBER) is sure to be on the list. For all the hype and growth, the company never turned a profit…until recently. While it wasn’t huge, Uber hit two major milestones in the past year. First, it achieved positive net income in June of 2021. Second, it generated $614 million in cash from operations in September. To be fair, June’s number was buoyed by a gain of $1.912 billion on the sale of an investment. Still, it marked a significant shift in investor sentiment. With 719 pageviews from financial pros over the last month, Uber Technologies became the second most searched software application stock behind Exela Technologies (XELA), beating out hot stocks like Shopify (SHOP) and Digital Turbine (APPS). We dug into the most recent earnings call and took a broader look at Uber’s performance over the past few years. And we uncovered something rather interesting. Uber’s Business When you step back and think about it, Uber is just a glorified taxi service. And yet, what it created was so much bigger. It wasn’t until 2019 the company went public. And after years of hype the actual performance was a bit of a letdown. In a nutshell, Uber uses a proprietary app to bring together drivers and riders for ridesharing (AKA taxis). Initially, the company met resistance from local and state governments. However, they worked through those issues in most places. Today, the company provides ridesharing, meal preparation and delivery, as well as some limited freight transportation services. THe company breaks its bookings down into three major categories: mobility (46.5% of revenues), delivery (43% of revenues), freight (10% of revenues), and other. You can see below the constant churn of acquisitions and divestitures as the company discovers its niche. Uber has its hands in a lot of pies trying everything from autonomous driving to advertising on its drivers’ vehicles. Financials Although hampered by the pandemic, Uber’s growth has been nothing short of phenomenal. The company managed to nearly quadruple its revenue in less than a decade. However, it wasn’t until recently that the company managed to eke out a profit on an adjusted EBITA basis. The good news is that management expects the company to deliver 7% margins as a percentage of gross bookings (25% of revenue) by 2024 while becoming free cash flow positive by the end of 2022. Currently, the company forecasts adjusted EBITDA of $5 billion by 2024 or around $2.69 per share. That’s a significant shift for the company who’s operated at a loss since its inception. Valuation Uber doesn’t have positive earnings, so we only have a few relevant measures. First, we have the price-to-sales ratio of 3.76x TTM and 2.46x FWD compared to the industrial sector of 1.43x and 2.61x. While it’s rich, that’s not terrible considering the significant growth Uber hits each year. Outside of 2020 which saw negative growth and 2019 which only grew at 25%, Uber drove revenues higher by more than 40%. More importantly, if we take the company’s adjusted EBITDA of 25% of revenue, we’d get $3.711 billion or around $2 per share. With the stock trading at ~$33.50, that’s an adjusted EBITDA multiple of 16.75x. How close would that be to actual income and cash? Let’s take a look at the reconciliation. The big ticket items for the company are the other income and expenses associated with investments and divestments, depreciation and amortization, as well as interest expenses. Investments and divestments will wax and wane, but should ultimately slow and even out over time. Depreciation and amortization will remain as would interest expenses. Yet, it’s fair to say that the adjusted EBITDA is a reasonable approximation for future steady state earnings. Our Opinion – 7/10 We can see a clear path for the company to become profitable in a big way. However, it could take years to realize the dream. At the moment, it’s more a question of opportunity cost than anything else. Uber can and should achieve superb results in a matter of years including profitability and cash flow. But like we said, it is still several years away. That said, it’s tough to ignore shares priced below the IPO when the company is tantalizing close to an inflection point in its history. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |