|

Proprietary Data Insights Retail Top Luxury Goods Stock Searches This Month

|

|

Stock Analysis |

Signet Jewelers Special Sparkle |

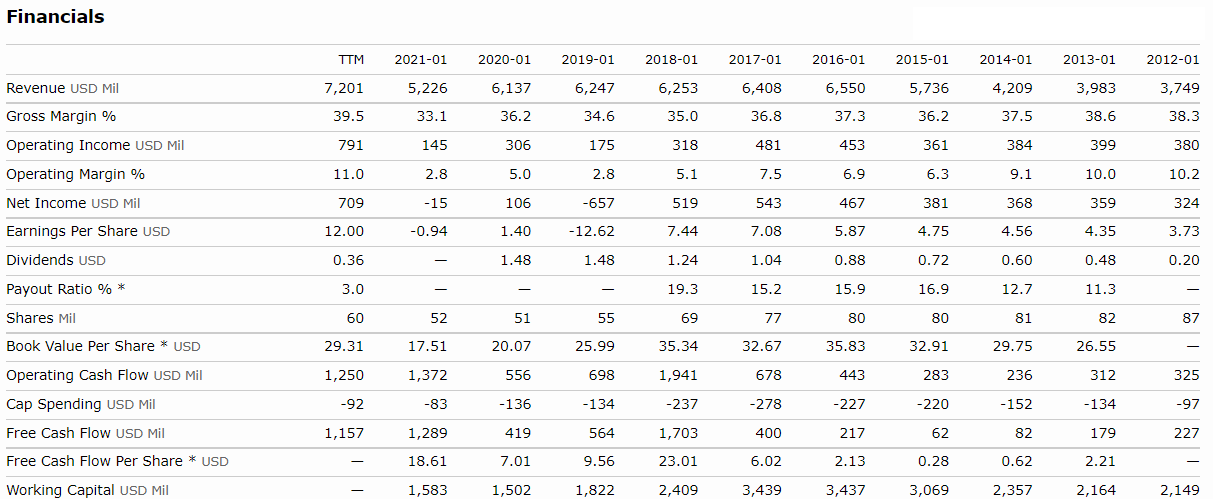

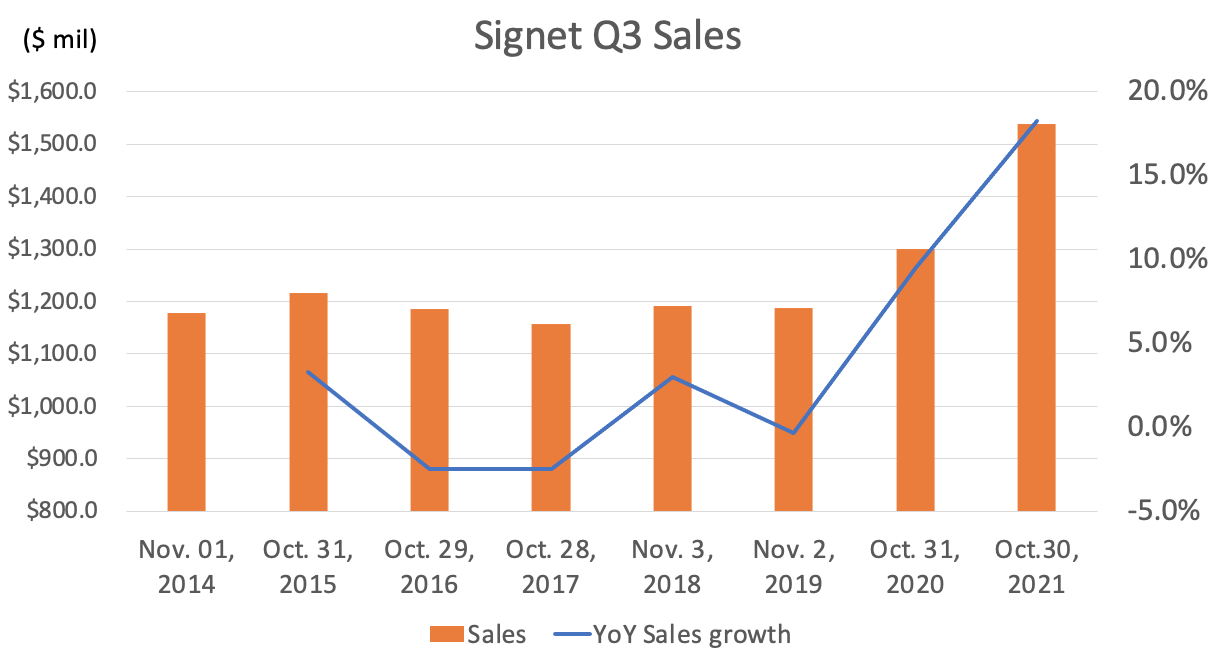

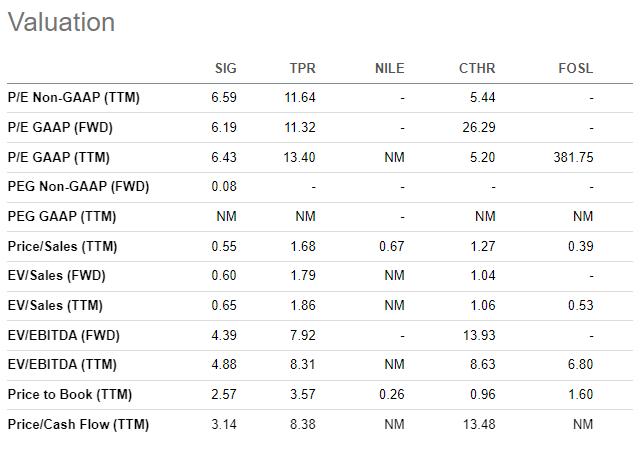

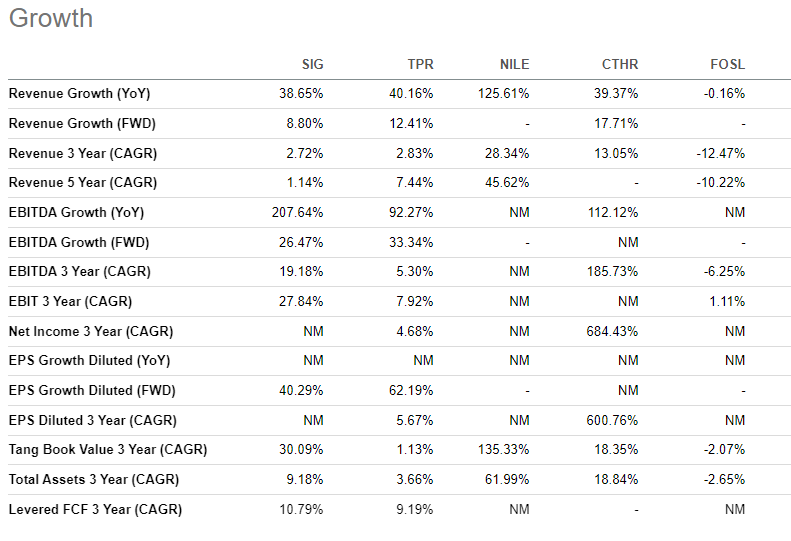

It’s pretty rare that a stock surprises us. And yet, Signet Jewelers (SIG) wasn’t one we’ve ever looked at. Frankly, we were checking out Tapestry (TPR) as the top luxury good stock search amongst the retail audience. But when we compared it to the other companies in our top searches, Signet stood out by a mile. At just a touch more than 6x forward earnings and 4x forward cash, Signet Jewelers is insanely cheap relative to its peers. And as we dug deeper into the company, we found a lot of reasons to like this stock. Signet Jewelers’ Business Founded in 1950, the Bermuda-based company operates in the U.S., Canada, The U.K, Ireland, and the Channel Islands. Within these countries, Signet is often considered the leading diamond retailer. 90% of the company’s sales occur in North America through its Sterling Jewelers and Zales units. U.S. stores operate nationally in malls and of-mall locations including Kay, Jared, Zales, and Piercing Pagoda. In Canada, the company operates under Peoples Jewelers and Mappins Jewelers. This segment also operates a variety of mall-based regional brands, including Gordon’s Jewelers in the United States and Mappins in Canada along with the JamesAllen.com website, acquired through R2Net. The international segment constitutes just under 10% which consists of the legacy UK Jewelry division thatoperates stores in the United Kingdom, Republic of Ireland and Channel Islands. These stores operate as H.Samuel and Ernest Jones banners in shopping malls and off-mall locations. The various brands break down into unique marketing segments including bridal (44% of sales), fashion (39%), watches (5%), and others (12%). Signet has done a considerable amount of acquisitions over the years, scooping up eight companies, with four in the last five years. In 2014, the company acquired Zale for $1.5B in its largest acquisition to date. Financials Signet’s revenues plateaued from 2016-2020. After a sift drop from the pandemic, they’ve quickly recovered and thensome. Outside of the pandemic, margins remained relatively steady. Earnings dropped in 2019 due to a one time charge off of goodwill for $735 million. Otherwise, they too have been fairly consistent. And in the last year, they’ve expanded quite a bit. Thankfully, management expects to continue the trend and is forecasting an adjusted EBIT margin of ~10.7% for 2022. The revenue growth has also been particularly eye-catching. Sales surged in Q3 by nearly 20%. YoY growth comes in at a staggering 38.65%. While forward growth is only expected to hit 8.8%, the company has done a remarkable job of cashing in on heavy consumer demand. Lastly, Signet’s rock solid balance sheet holds $1.5B in cash on hand compared to long-term debt of $147M and capital leases of $994M. That gives them plenty of room to expand their operations. Valuation This is where Signet really shines (pun intended) compared to its peers. Since Blue Nile (NILE) and Fossil (FOSL) aren’t profitable, we’ll set those aside for now. Tapestry is the real one we were interested in. And it’s nearly twice as expensive as Signet in nearly every category. Even Charles & Colvard’s (CTHR) trailing P/E ratios fall apart when we look out to the following year. Plus Signet’s price to cash flow is outstanding with prices trading 3x trailing and a bit more than 4x forward cash. Even when we look at growth, Signet delivers more consistent results across multiple categories. True, companies like Blue Nile are seeing huge sales growth as they expand. But when it comes to actual earnings and cash growth, Signet takes the cake. Our Opinion – 9/10 Signet is by far and away the best jewelry stock amongst its peers. And in a broader sense, it’s quite cheap both in terms of earnings and cash. We could see shares dropping down towards $60, which would be a fantastic spot to start a position. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |