|

Proprietary Data Insights Financial Pros Top Credit Services Stock Searches This Month

|

What we’re watching

|

|

A look at diversified financial services company Ally Financial.

|

|

Stock Analysis |

Make This Name Your ALLY |

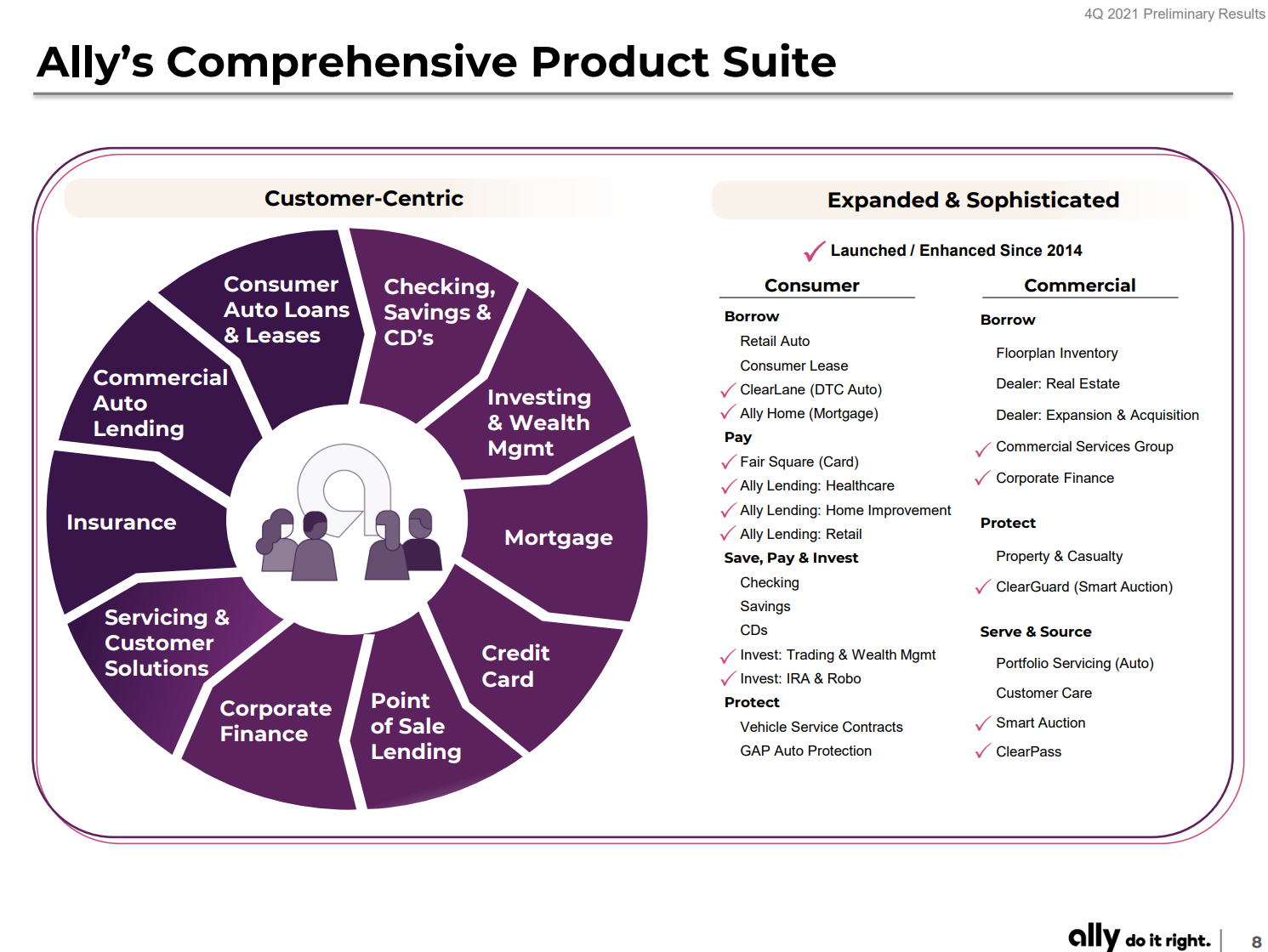

Yesterday, we introduced you to Capital One Financial (COF). That particular company gives investors exposure to the credit card and loan business more than most other stocks. At the time, we identified Ally Financial (ALLY) as another stock that peaked our interest. While a member of the credit services industry, its makeup was different enough we felt it deserved its own newsletter. And you’ll see why in short order. Ally Financial’s Business When we say Ally Financial is a ‘diversified’ financial services company, we mean it. The company offers customers a broad array of financial products, making it a one stop shop. Ally operates as both a financial and bank holding company. Ally Bank is an indirect, wholly owned subsidiary of Ally financial services. The company operates primarily through four main segments:

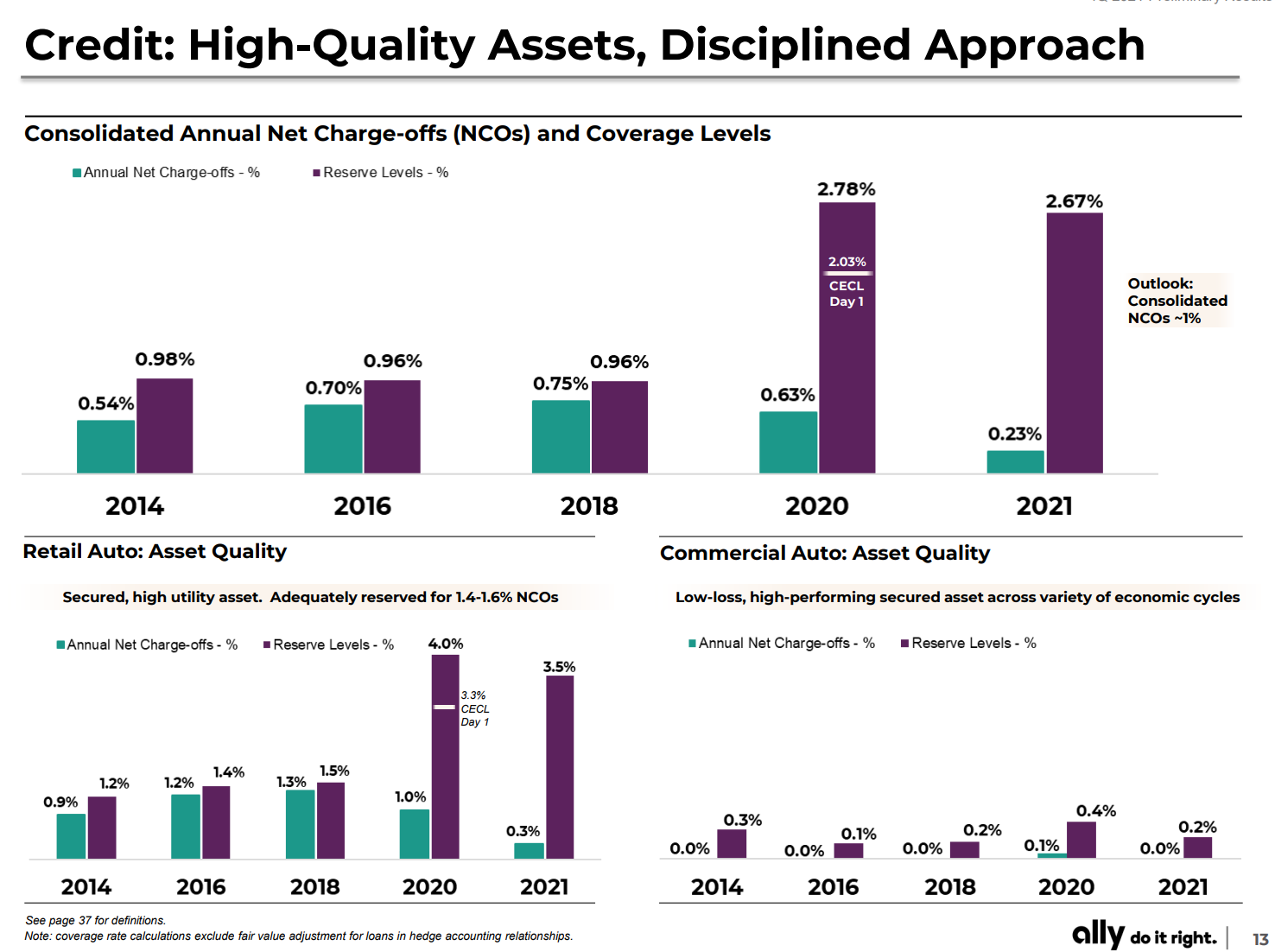

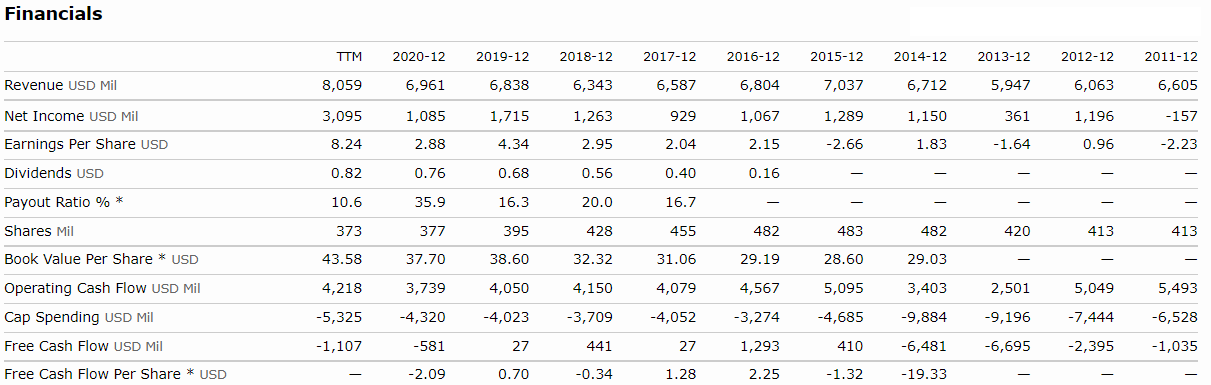

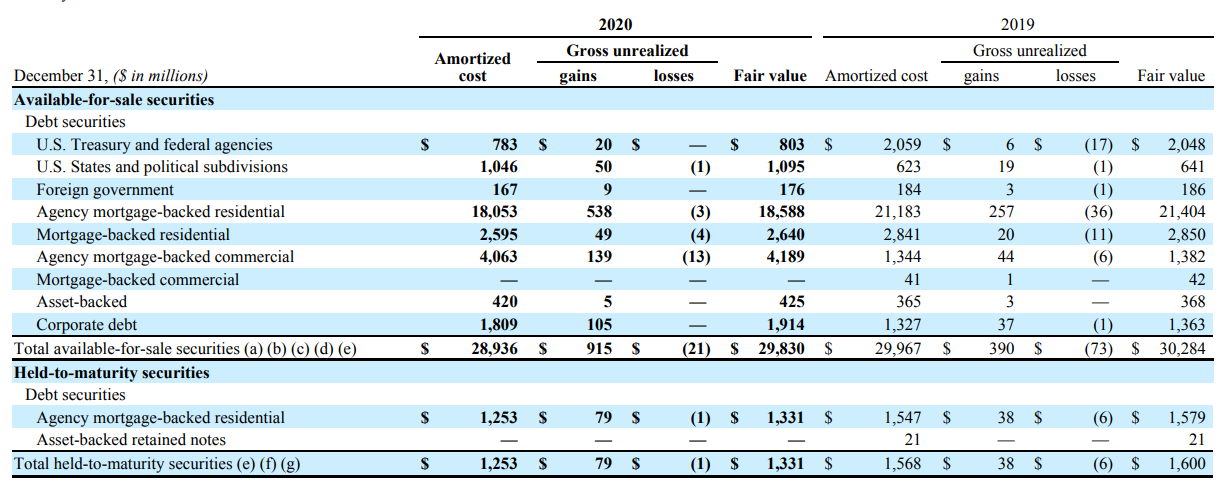

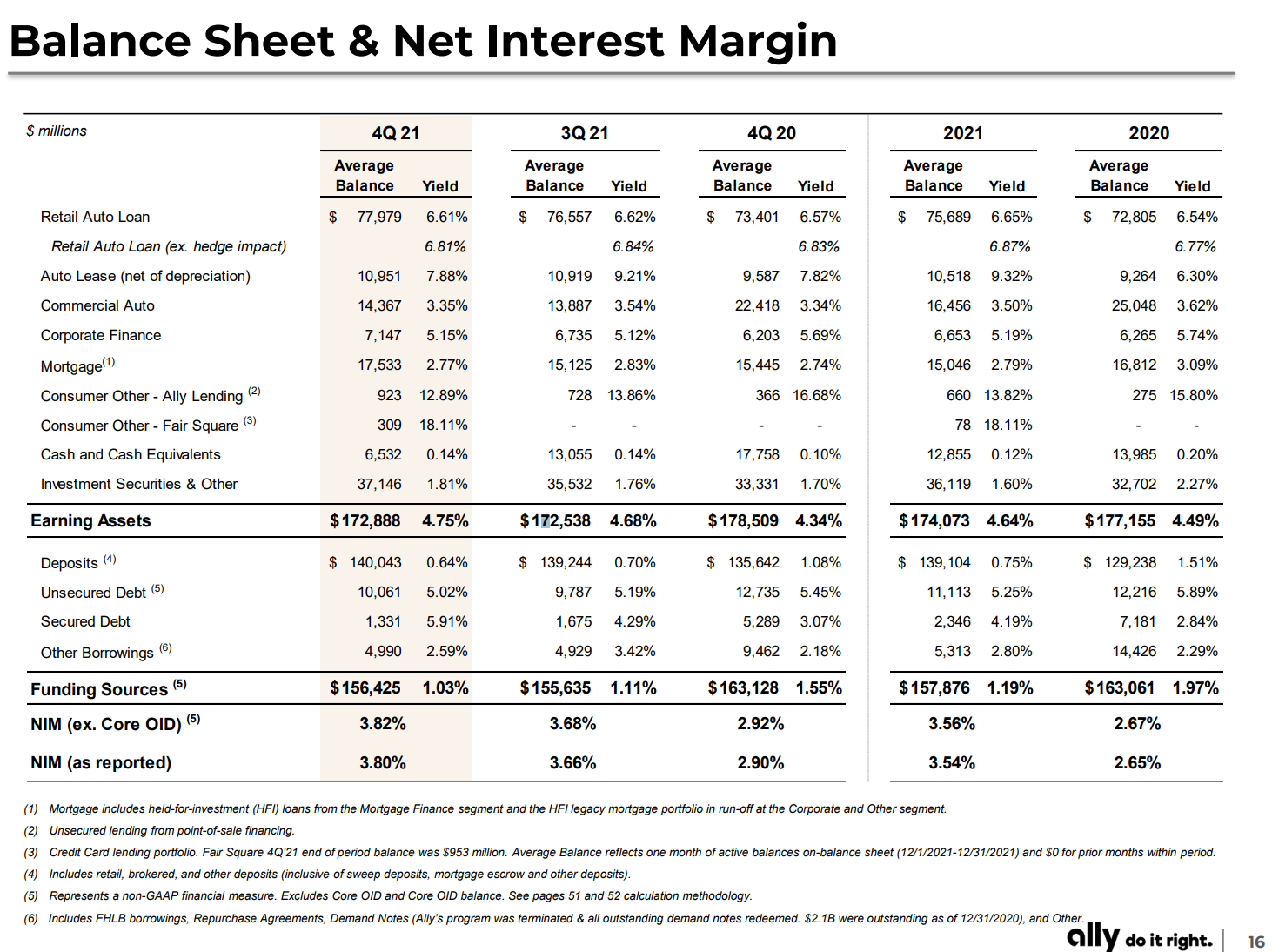

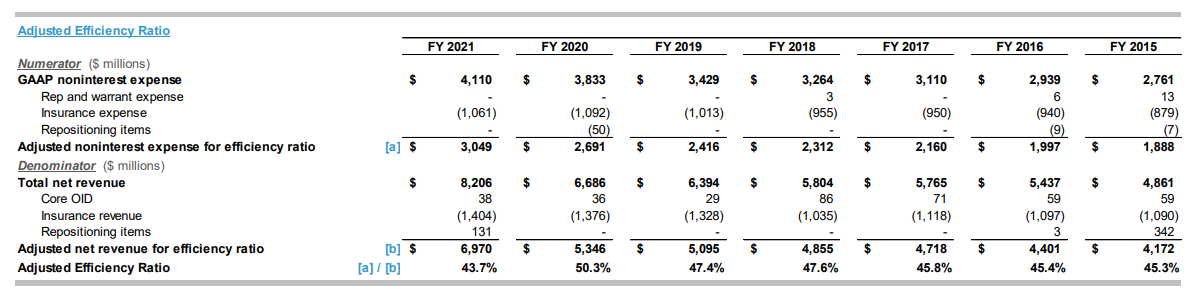

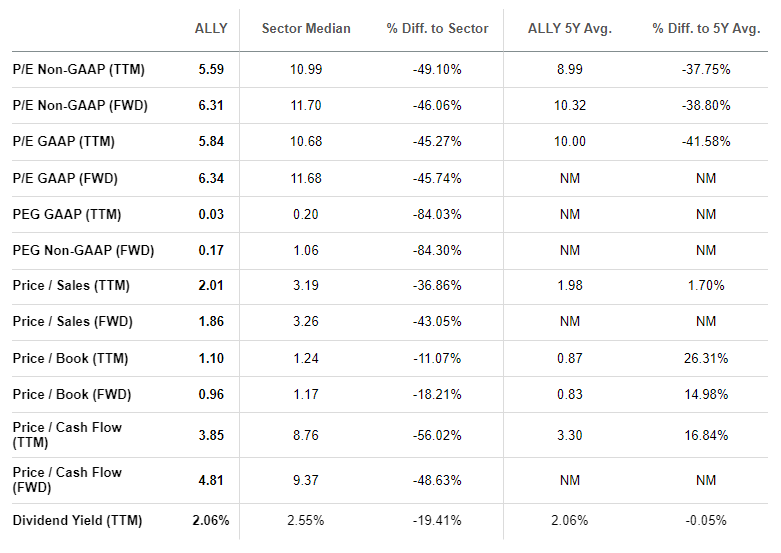

As the visual shows above, Ally has continued to expand its offerings aggressively. In 2016, they acquired TradeKing, a digital wealth management firm. Three years later, Ally scooped up Health Credit Services. Last year, they acquired digital-first credit card company Fair Square Financial. Like most banks, Ally stands to benefit from higher interest rates which drive additional profits to the bottom line through an expanded net interest margin, the difference between the rates they pay depositors vs the rates they charge borrowers. Ally has benefited from lower net charge offs (bad loans) each year than its reserve levels. The gap in 2020 and 2021 was the widest it has seen in years. Financials In the last decade, Ally’s saw revenues slip from 2015 to 2018. However, the last three years have been kind to the company, driving total revenues that exceeded any point over the 10-year period. During that same period, earnings and income followed suit, contracting before expanding. Today, EPS is nearly double what it was in 2019 and 4x greater than 2016. Capital spending here is misleading as Ally takes their cash and invests it in a wide range of financial products. You can see an example for the 2019 and 2020 calendar years below. As we noted earlier, Ally benefits from higher interest rates. The table below shows how they have been able to expand their margins by earning more from their loans while decreasing their borrowing costs. We’re also pleased to see Ally improve its efficiency ratio which measures noninterest expenses as a percentage of revenues. The current efficiency ratio is the lowest they’ve seen since 2015. Valuation We mentioned in yesterday’s newsletter that Ally and Capital One Financial stood out because of their value. Ally shows many of the same characteristics we highlighted for Capital One. The price-to-earnings ratios are spectacular as are the price-to-cash flow ratios. Like Capital One, both are expected to worsen slightly next year as many financial institutions come off a banner year. Nonetheless, shares trade at under 5x forward cash, with nearly every measure almost 50% cheaper or better than the industry average. We would like to see management push more cash back to shareholders either through an increased long-term dividend or a special one off distribution. Our Opinion – 9/10 Like Capital One, Ally Financial has a strong business that’s set to benefit in a higher rate environment. The difference here is the company creates a more diverse revenue stream. That hedges them from single product risk better than Capital One. It’s that diversification that prompted us to give Ally a slightly higher rating than Capital One. We like shares at $140. However, with such a massive run since early 2020, be aware that we could see a pullback to $100 per share if the broader market takes a tumble. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |