|

Proprietary Data Insights Financial Pros Top Semiconductor Stock Searches Last Month

|

|

Stock Analysis |

Qualcomm Destroys Most Other Semiconductors |

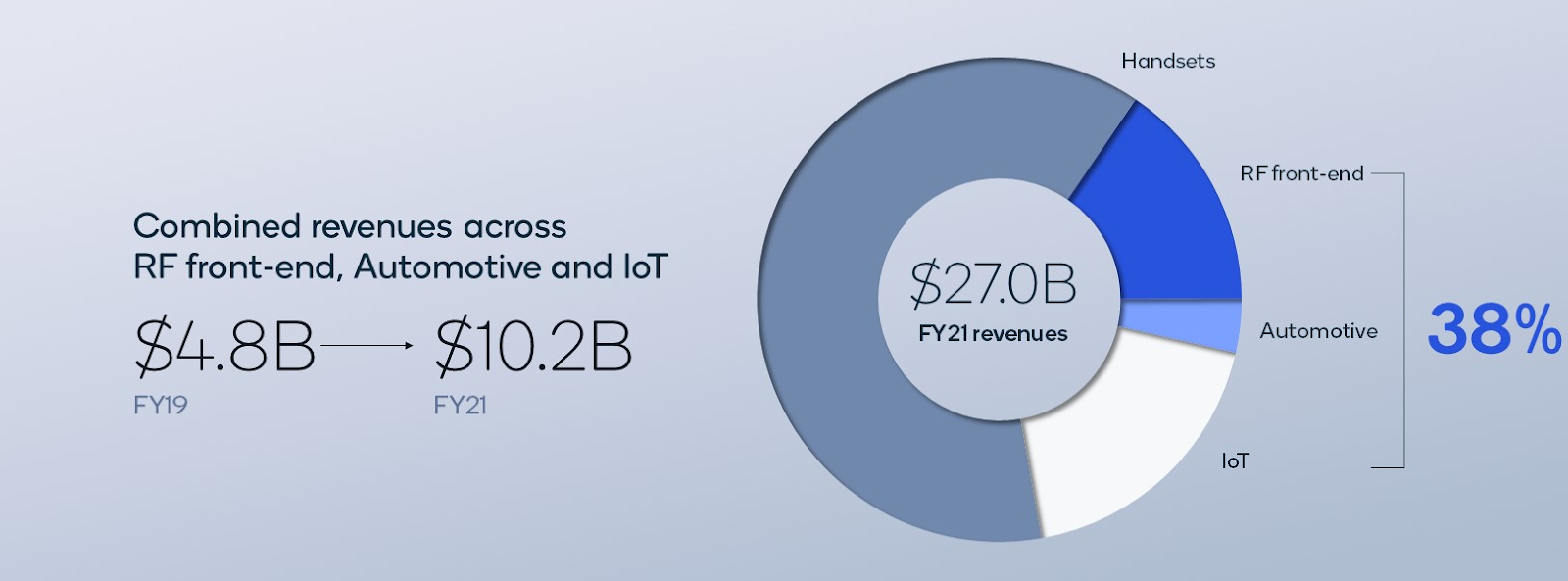

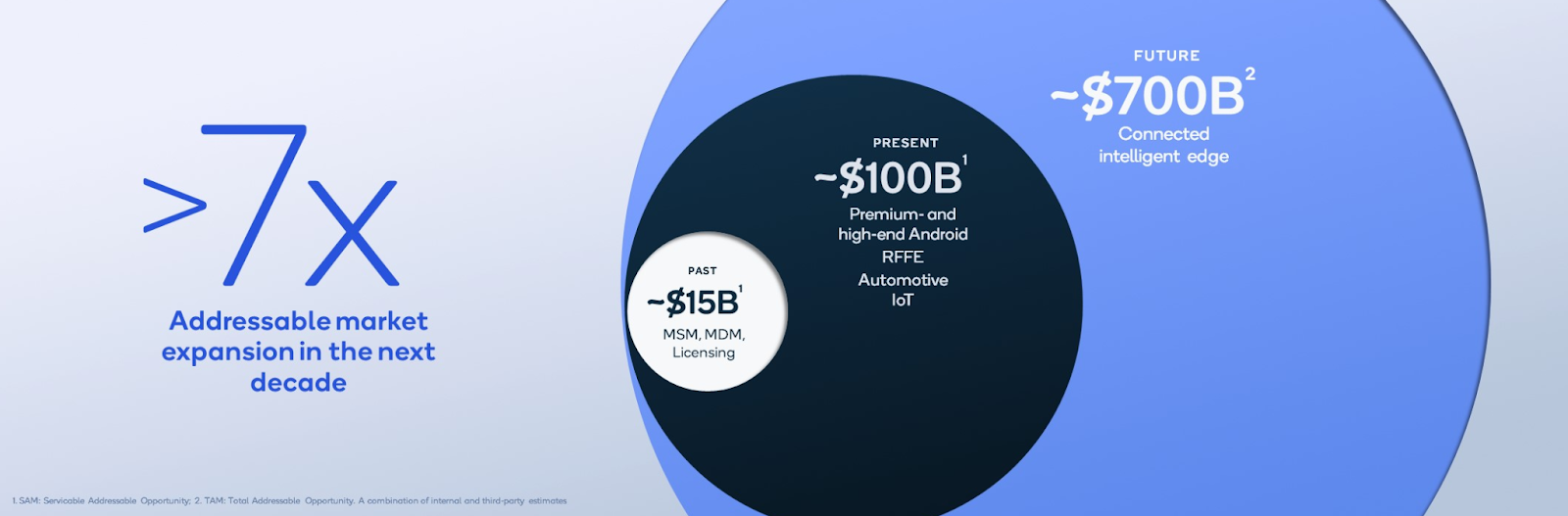

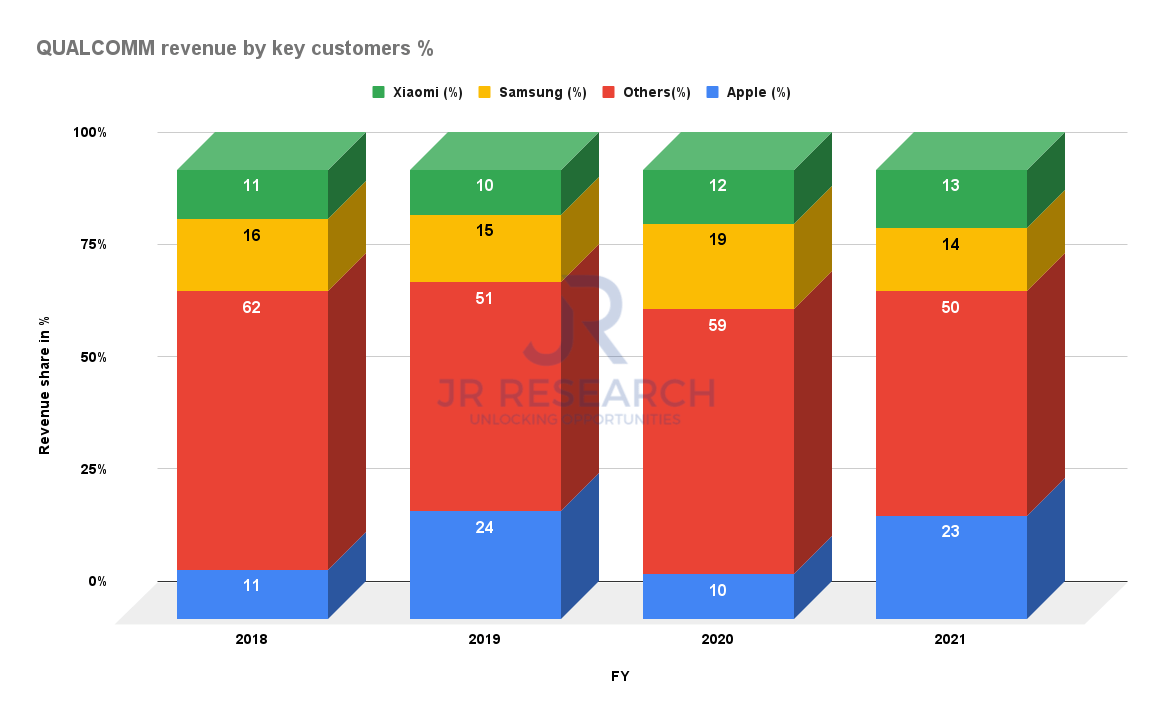

Year to date, the VanEck Semiconductor ETF (SMH) is down 16%. Companies like Nvidia (NVDA) are off more than 20%. Qualcomm (QCOM) showed relative strength to its peers with shares 10% year-to-date. We began diving into the searches for semiconductor stocks by financial pros over the past month. It seemed reasonable that given the recent pullback and a strong outlook, there had to be some value in the mix. That’s when we came across Qualcomm. The company’s laser focus on mobile devices centers it on a key growth segment within the semiconductor industry. Not only does it play to the current product base, but it’s positioning itself for the eventual rollout of 5G, which stands to become a massive revenue stream for the next decade. However, when we stacked it up to its peers, one company gave it a run for its money. But let’s take a step back and look at the company’s business as a whole. Qualcomm’s Business Based in San Diego California, Qualcomm designs, manufactures, and markets digital wireless telecom products and services based on Code Division Multiple Access (CDMA) technology. Products include CDMA-based integrated circuits and system software for wireless voice and data as well as GPS. In other words, they make the processors that make wireless devices work. The company is a leader in 3G, 4G, and now 5G technologies. Yet, their products find homes in other industries and applications including auto and the internet of things. The company operates two main segments – CDMA technologies (83% of revenues), which encompasses owned and operated products, and technology licensing (17% of revenues). CDMA technologies can be further split into the different subgroups they support. What’s impressive here is that non-handset revenue has more than doubled over the past two years. That means outside of their key segment which is already in high demand, Qualcomm’s other areas have grown even faster. In fact, management sees the total addressable market as 7x larger than the current product makeup. One of Qualcomm’s challenges has been its reliance on a few key customers.

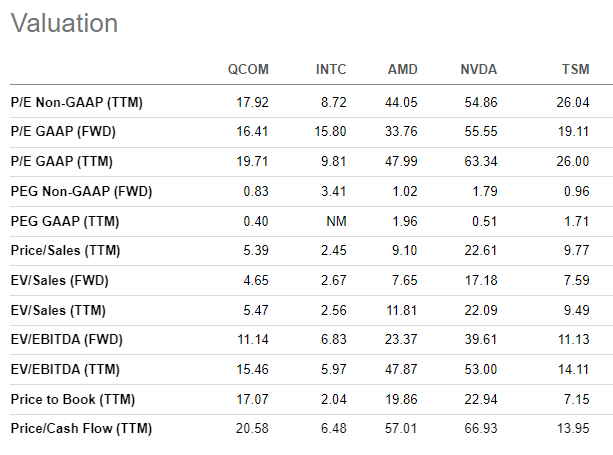

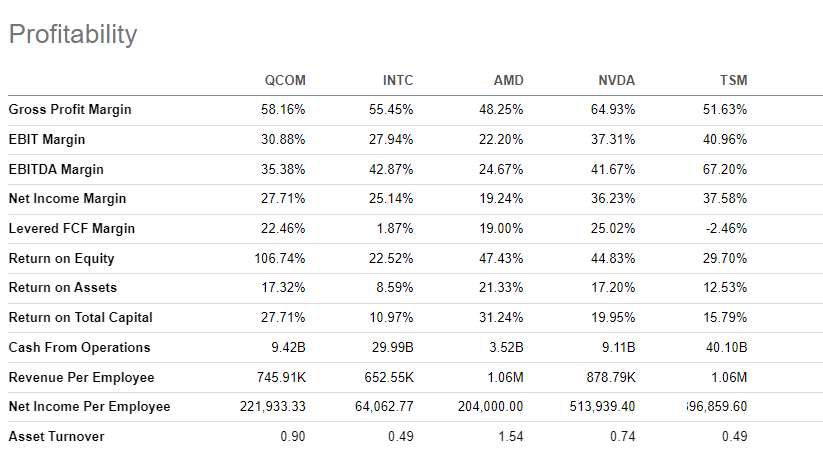

Source: JR Research That’s left the company expensed to a few big players over the years. However, Qualcomm’s managed to maintain a healthy mix of android customers (especially in the other category) to avoid too much exposure. One new point in the favor of Qualcomm. As the geopolitical environment continues to shift, the risk to Chinese OEMs becomes greater. Should we start to see outright bans, it would help Qualcomm capture additional market share. Financials Despite the enormous challenges facing semiconductor companies, Qualcomm has done an excellent job of managing its supply chain to keep costs in line. At the moment, management simply wants to build more to meet demand. The last couple of years have seen sales explode as higher prices and demand drove revenue growth of 42.65% in 2021. That’s incredible given the 10 year average in 2019 was 8.83%. What’s equally impressive is management’s ability to expand operating margin even as it held the line on gross product margins. That led to $8.65 billion in free cash flow generated last year, nearly double what it saw in 2019 and its highest amount ever. All this come s for a company with $13.7 billion in long-term debt and $19.2 billion in total long-term liabilities. However, the $11.3 billion in cash tends to take care of that. That leaves management plenty of room to expand operations to capture more demand in current verticals and adjacent segments. Valuation At the beginning, we mentioned that Qualcomm demolished most of its peers with the exception of one, Taiwan Semiconductor (TSM). Next to its peers, Qualcomm has the best P/E ratios with the exception of Intel (INTC). However, as we’ll see in a minute, Intel can’t grow revenues to save its life. Across most other metrics, whether it be price to sales or enterprise value to sales of EBITDA, Qualcomm is the best or darn near close. The one measure where it’s not the best is in price to cash flow. While Intel holds that prize, Taiwan Semiconductor (TSM) has a better metric. This likely means TSM recently spent money on capital investments that it’s currently reaping the cash benefits from. As we turn to profitability, we find that Qualcomm and Taiwan Semiconductor drive solid net income margins. Though Nvidia has the best across the board. It’s worth nothing that Qualcomm does a nice job balancing return on assets, equity and capital. Lastly, we wanted to cover growth. This is where Qualcomm really shines. Other companies may have higher growth, but only Qualcomm has that right balance between revenue growth, profitability, and valuation. Our Opinion – 8/10 Qualcomm is definitely a great company with a lot of avenues for success. Right now, shares are priced well. However, a broader market correction or global recession could easily wipe out the stock’s recent gains. That’s why we don’t mind it at these prices for a nibble, but prefer something closer to $120 per share. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |