|

Proprietary Data Insights Financial Pros Top Paper & Lumber Products Stock Searches Last Month

|

|

Stock Analysis |

Money That Grows on Trees |

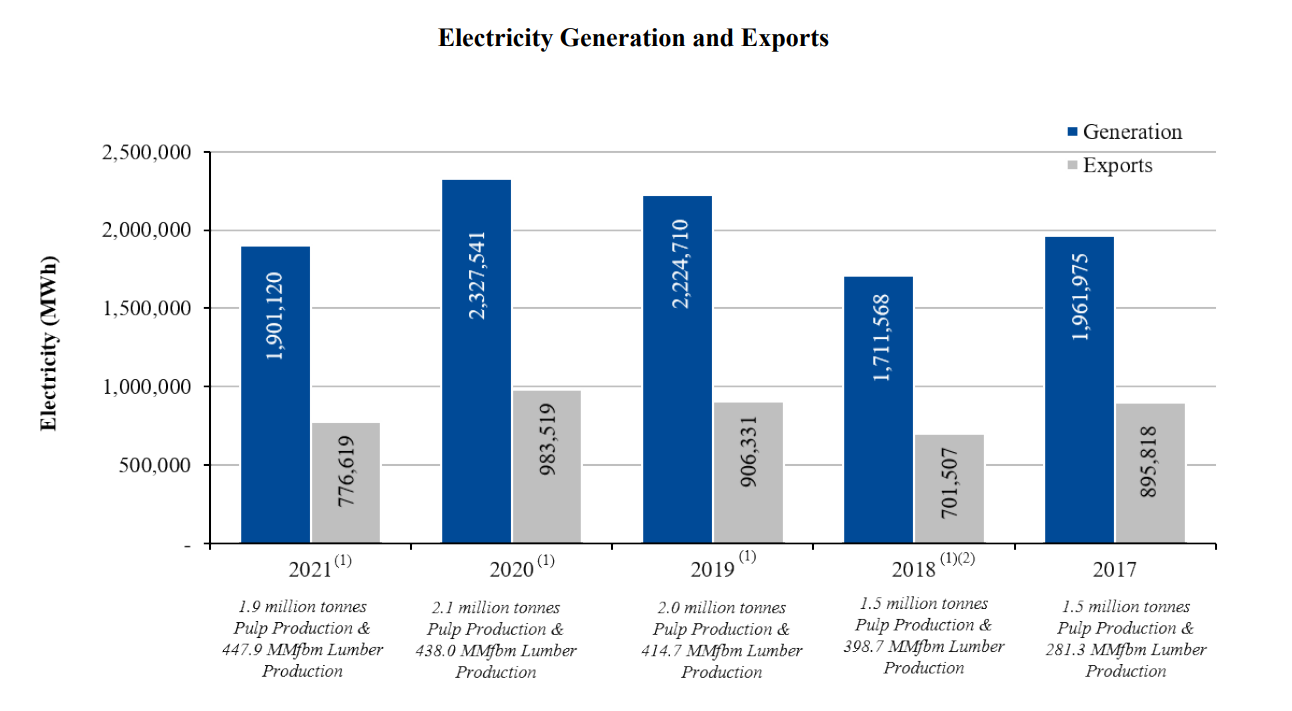

By now, most of us know that lumber prices soared during the pandemic. While the cost of a 2×4 has declined some, lumber mills are still making a pretty penny. One of the more interesting companies we’ve come across is Mercer International. As the third most searched for paper and lumber products stock search by financial pros last month, the company only garnered 8 pageviews. Clearly, investors aren’t looking to hard into this industry. But, we think they’re missing out. You see, Mercer is unique in that not only does it sell paper products and lumber, but it also generates and sells green energy produced from biomass at their mills. And that gives this company a unique twist that could lead to some undiscovered opportunities. To top it all off, shares trade at a paltry 6.45x forward earnings and a price to forward cash flow of 2.99x. Here’s the story behind the company. Mercer International’s Business Based in Vancouver Canada, Mercer International manufactures and sells wood and paper products. As we mentioned earlier, the company uses bioproducts that come from pulp production such as black liquor and wood waste. In turn, Mercer uses these products to power their plants while selling excess electricity to the local markets. The company’s operations fall into two segments:

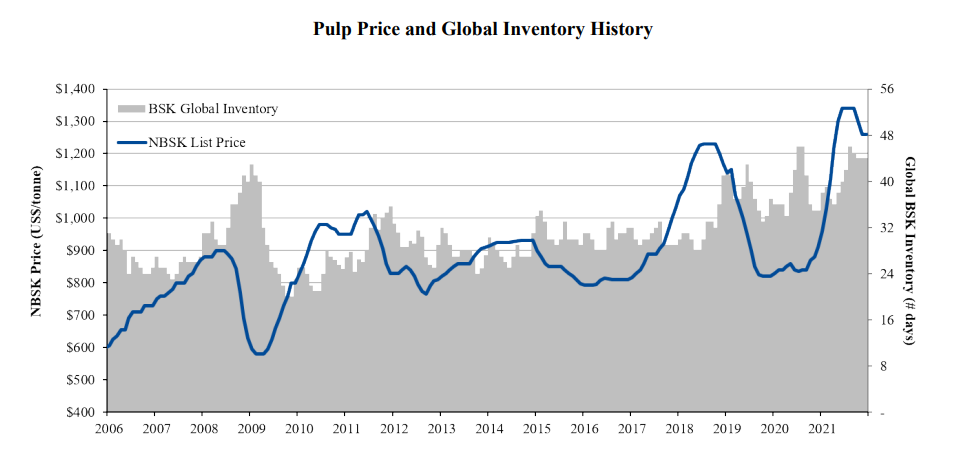

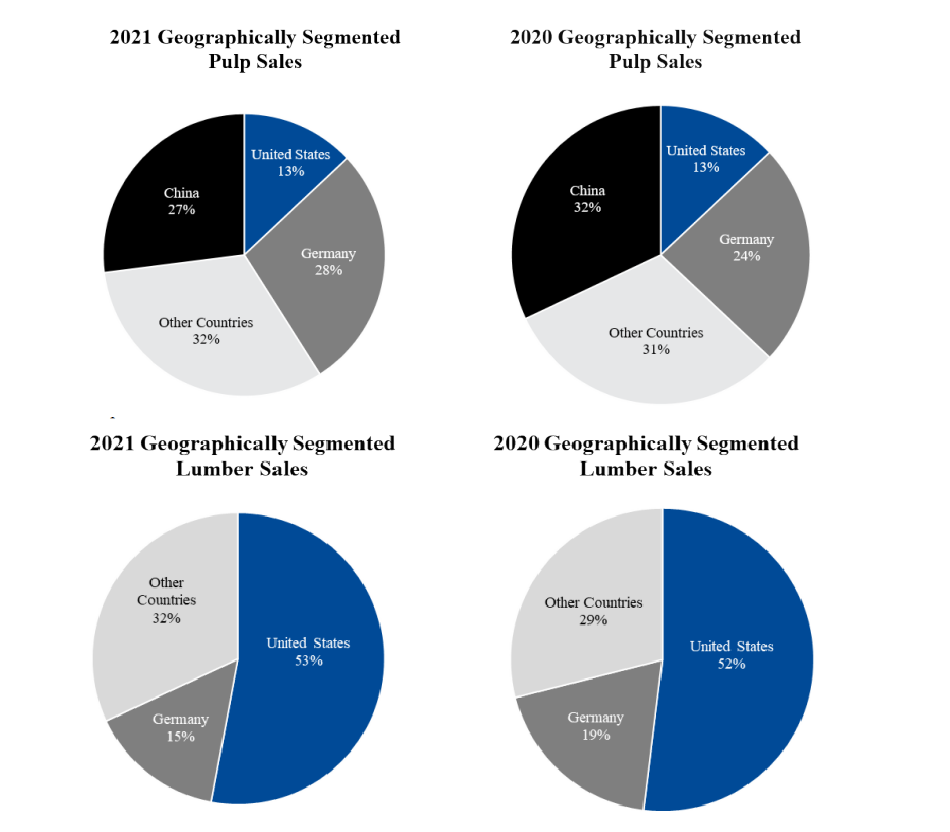

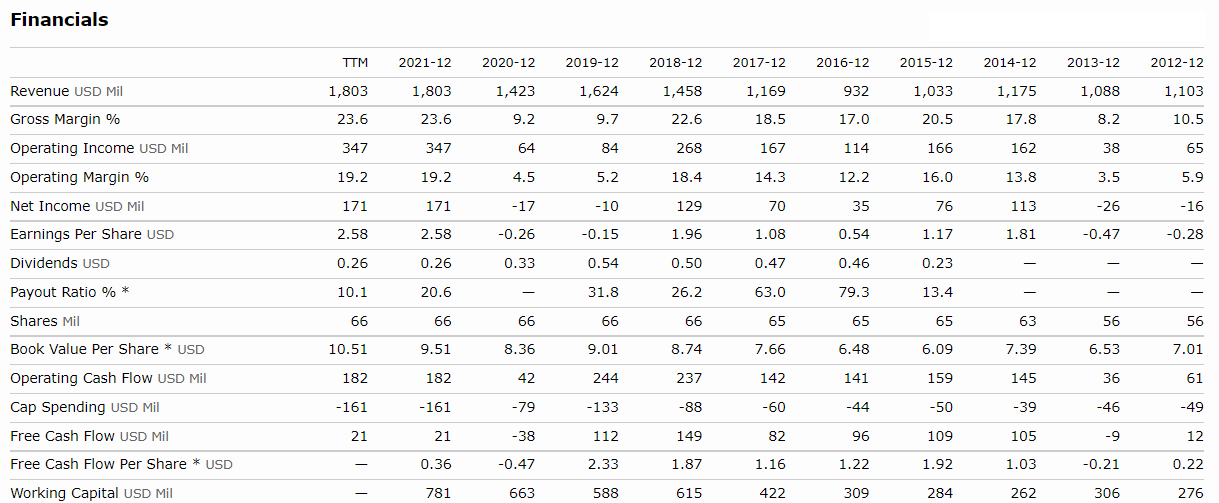

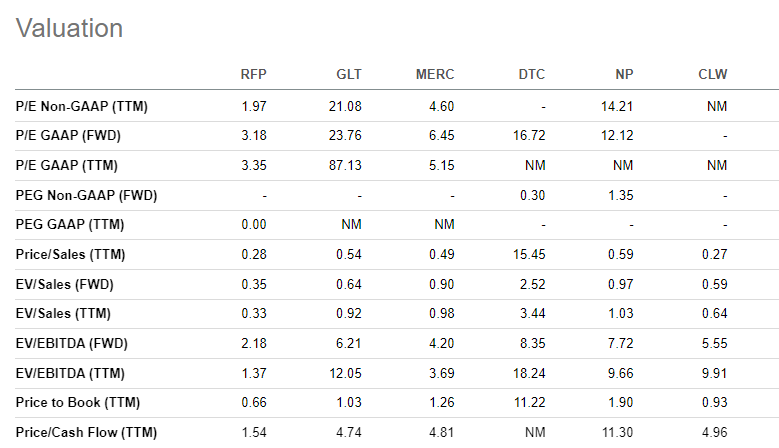

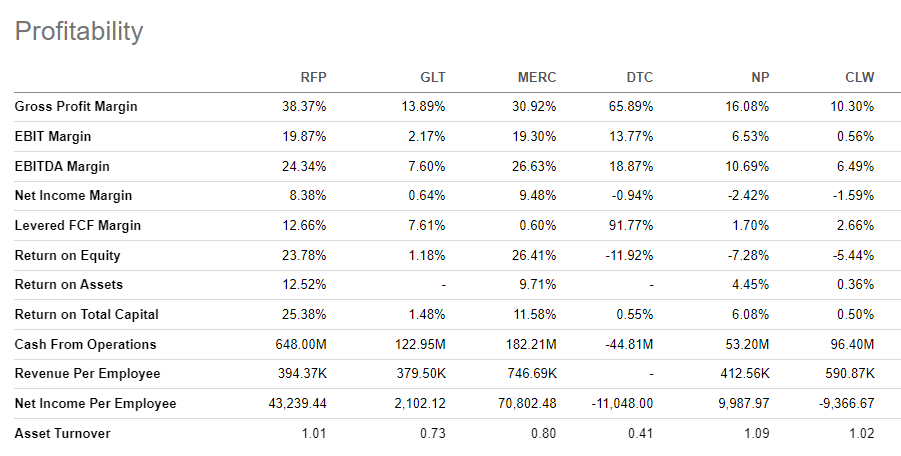

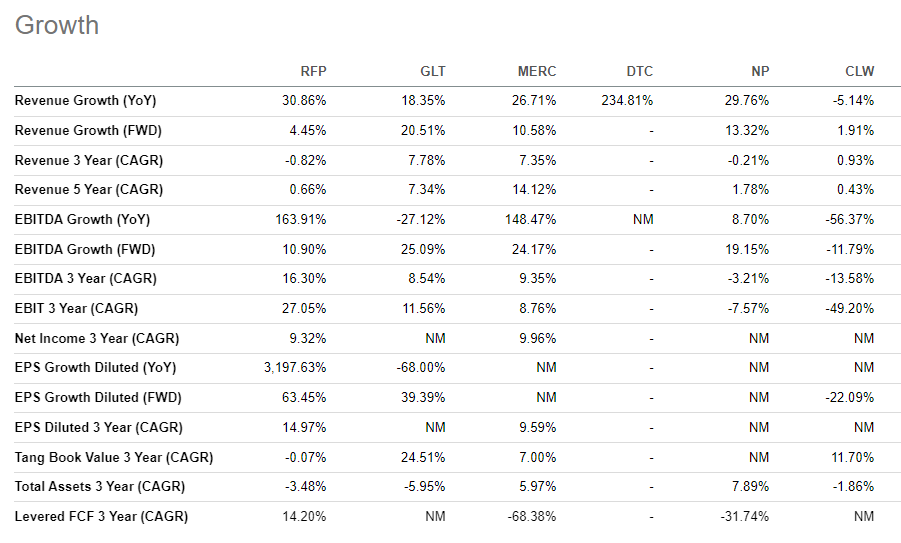

Mercer has benefited from higher prices in both the lumber and pulp markets. For example, the average realized lumber price jumped 74% to $699 mean thousand board feet. Pulp prices has climbed in the past year even as global inventory has grown. Lumber prices have been driven higher by demand for housing and construction in the U.S. while general tissue paper consumption has pushed pulp prices through the roof. Geographically, Mercer is split fairly evenly with pulp sales while it gets about half its lumber sales from the U.S. Financials It’s taken time, but Mercer has managed to nearly double revenues over the last decade while expanding margins. To be fair, gross margins cyclical with the demand for products, which impacts realized sales prices and gross margins. In the last year, the company has fed off higher lumber and paper prices to generate $182 million in operating cash flow and $21 million in free cash flow. That’s allowed them to maintain a healthy dividend that yields 2.26%. Now, the one thing Mercer hasn’t done is brought down its debt load. Currently, the company holds $1.2 billion in long term debt and $1.65 billion in long-term liabilities overall. However, the company’s current assets, including cash of $345 million, come out to $1 billion compared to current liabilities of $283 million. As a ratio, the company has current assets to total liabilities ratio of 0.549x or a total gap of $876 million. That excludes any long-term assets such as their mills. The point is that while debt is high, so are their assets. Still, with interest expenses of $17 million per year, it would be nice to see them pay down that debt rather than issue dividends in the short-term. That would also allow them to expand operations through acquisitions or investments. Valuations When we compared Mercer to other paper products companies, we found Mercer to trade at a better discount than its peers in most categories. Using our proprietary search data, we compiled a list of the top paper product stocks searched by financial pros. The comparison showed us Mercer and Resolute Forest Products (RFP) as tow of the better value stocks. RFP does trade at a better multiple for P/E ratios, P/S ratios, and P/Cash flow. The other companies really didn’t come close. So, we wanted to see if profitability was a separating factor between these two companies. Interestingly, both had solid gross and EBIT margins as well as returns on equity, assets, and total capital. So if profitability wasn’t the reason for the different valuations, then maybe it was growth. Here we gained a better understanding of the current share prices. While RFP grew revenues at a slightly higher rate last year, Mercer is expected to hit more than double what RFP will next year not just in revenues, by EBITDA. Our Opinion – 8/10 While we’re probably splitting hairs, we’d like shares below $12. Although the company is trading at extremely cheap multiples, it’s been stuck in a range of $8-$18 for the better part of a decade. Nonetheless, we think Mercer is a fantastic company to own if you can get it at the right price. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |