|

Proprietary Data Insights Financial Pros Top Online Retail Service Stock Searches Last Month

|

|

Stock Analysis |

Down 68%, is Shopify Cheap? |

Shopify was one of the hottest stocks in 2020 and 2021. Its ticker consistently topped searches by retail and institutional investors. At the start of 2020, shares traded at $403. By the end of the year, it hit $1,132. Shares continued to climb until they peaked at $1,763 in November, 2021. And that’s when things took a turn for the worse. Shopify’s stock tumbled nearly 70% over the next several months to $566 where it sits today. Yet, many analysts think it has more room to fall. While we agree that’s likely the case, we want to get a sense of where this stock becomes a screaming buy. Even as its popularity amongst financial pros slips, as we see in the data above, the company kills it when it comes to growth. Plus, its stake in Affirm technologies gives it an unrealized gain of $3.9 billion! But let’s back up and start with an overview of what Shopify does. Shopify’s Business When you want to start up an online business or move your operations online, Shopify is where you go. The Ottawa, Canada-based company gives small and medium-sized businesses a platform that enables merchants to manage products and inventory, process orders and payments, ship orders, build customer relationships, and leverage analytics along with back-office integrated reporting. Shopify’s business breaks down into two main categories:

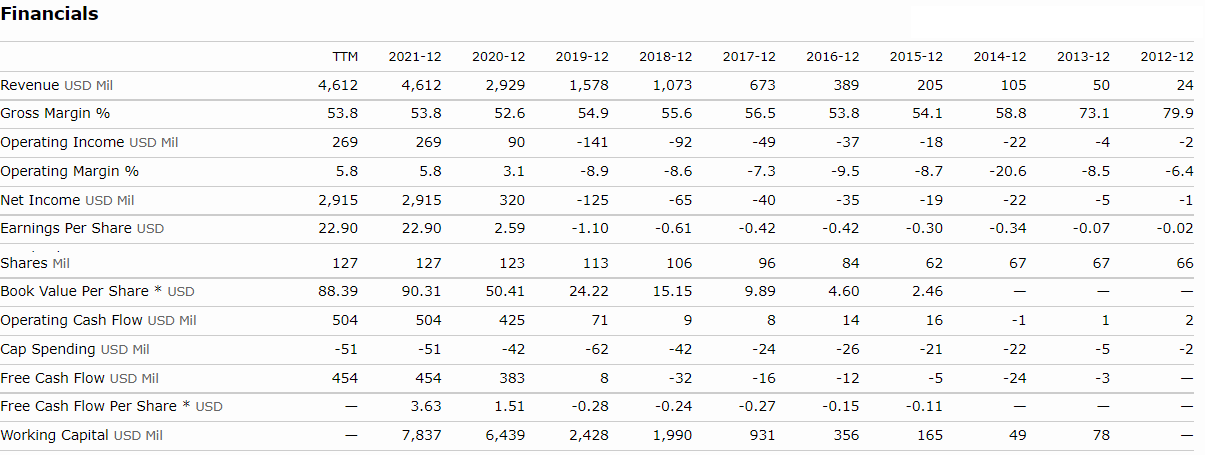

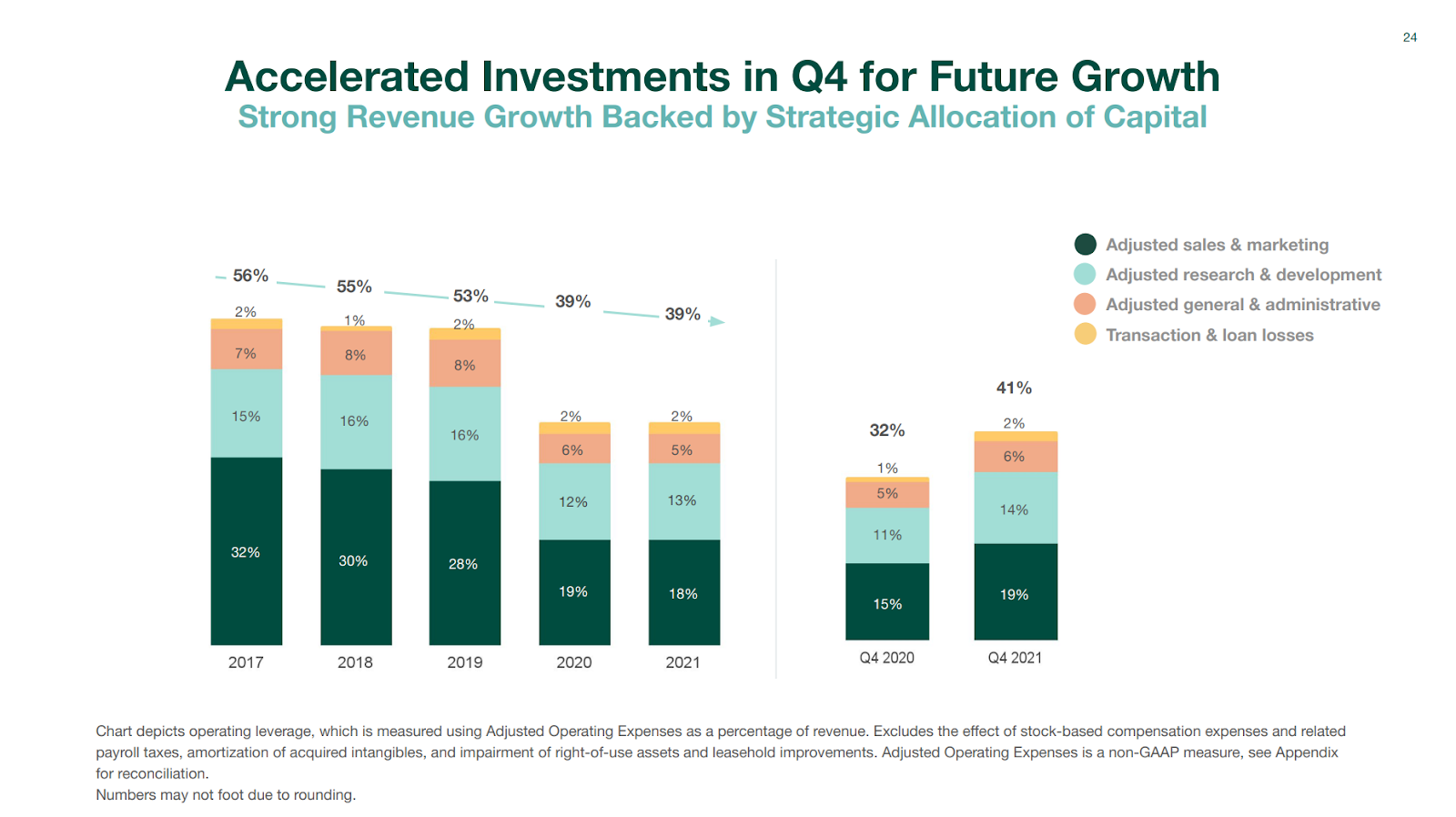

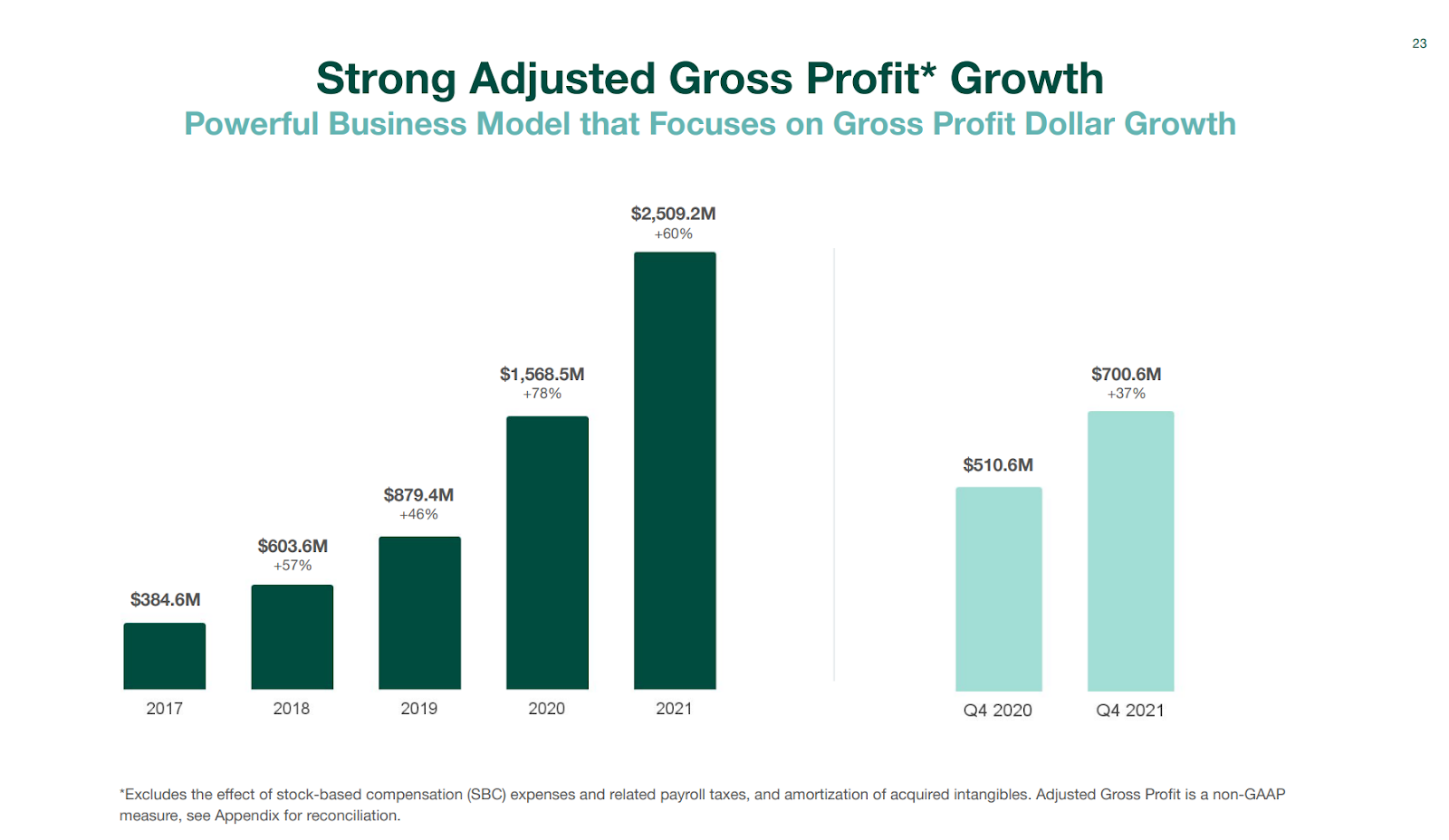

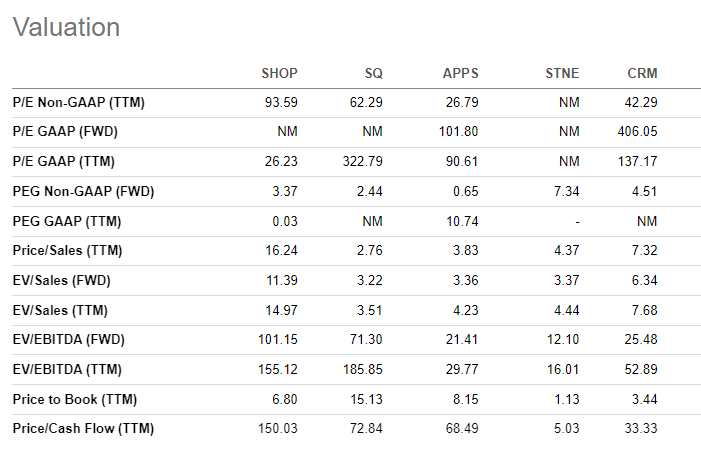

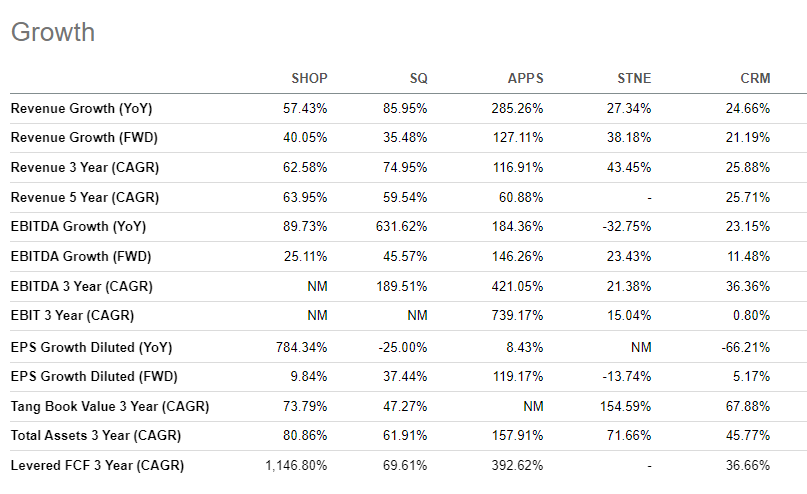

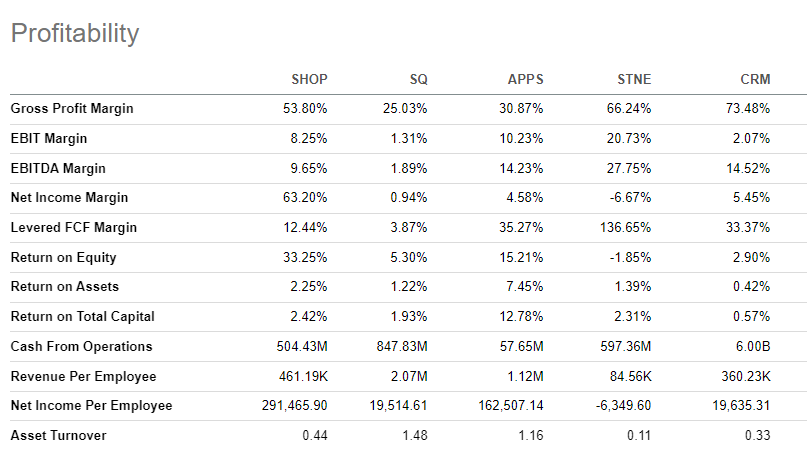

Currently, Shopify owns around 10.3% of the U.S. retail eCommerce market, coming in second behind Amazon’s 41% and ahead of Walmart’s 6.6%. Looking into the future, the company created initiatives based on the respective time frames needed to complete the project. Financials Shopify’s growth has been nothing short of breathtaking. The company’s 5-year average growth is 63.95%. Management expects the company to grow below this past year’s 57%. However, most analysts expect this to be well north of 40%. It wasn’t until recently the company managed to turn a profit. That came on the back of the massive expansion during Covid where online retail growth exploded. However, the company doesn’t generate much cash at the moment which is concerning. That’s evidenced by the low operating margins, which have begun to expand. A big piece of that comes from the reduction in R&D and sales and marketing costs over the last two years. That helped the company nearly triple adjusted gross profits from 2019 to 2020. Still, it should be pointed out that a big chunk of the company’s marketing costs are driven by referral fees for their affiliate network. Shopify has little to no debt. That gives it plenty of room to spend on business expansion. Lastly, we want to highlight the company’s investments worth $3.2B as of December 31. These include their $2B investment in Affirm (AFRM), Global-E, and several other companies. In total, Shopify holds nearly $4B in equity and other investments, or $31.50 per share. Valuation Shopify isn’t the easiest to value or compare. Though its core business model is relatively straightforward, the ancillary services it provides, such as Shop Pay, which have lower margins. Yet, these units drive growth, customer stickiness, and lower acquisition costs. To start, we looked at some basic valuation measures. What surprised us initially was the P/E GAAP of 26.23x. Looking back to the previous section, the price to adjust gross profit is just below 20x. Then again, as Shopify logs gains from its investments, that pads its income without adding cash. At the moment, there aren’t any great estimates for forward earnings due to since growth estimates offer a wide range. Given recent market volatility, these could land anywhere. Instead, we want to take a look at the price to sales and price to cash flow. In both cases, Shopify is the most expensive stock. The next question we have is whether Shopify’s growth makes up for the lack of value. Kinda… Revenue growth is quite robust. Only Digital Turbine (APPS) beats it consistently. Yet, the much smaller company also has a more limited total addressable market. What’s readily apparent here is Shopify isn’t profitable and doesn’t try to be, which is a bit concerning. Now that might seem odd given the following data. However, Shopify’s most recent year’s profitability was largely driven by gains on its investments. Hence the net income margin above the gross margin. In actuality, its net income margin is probably closer to 5%-15%. Our Opinion – 4/10 Shopify is top of its class in terms of the products it delivers to its customers. But for shareholders, it’s currently a dud. We don’t have any insight from management when they expect to become profitable and start generating cash. This company could be a monster in a decade. But until we get more clarity on what they will do in the next several years to become profitable, it’s not one we want to get close to. Where would shares start to become interesting? Probably closer to $300. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |