|

Proprietary Data Insights Financial Pros Top Marine Shipping Stocks Last Month

|

|

Stock Analysis |

Global Ship Lease Plunders Ocean Gold |

Dry bulk shippers are all the rage. Companies like Star Bulk Carriers (SBLK) and Safe Bulkers (SB) have seen shares climb 500% or more in the last several years. The cause – higher shipping rates. At one point, the cost of moving freight from Shanghai to L.A. skyrocketed from $4,000 to nearly $30,000. While prices have eased some, they remain at historically elevated levels. Yet, we believe Global Ship Lease (GSL) is in a better position to weather the coming storm. With inflation through the roof and energy prices at extreme levels, major manufacturers like China will have no choice but to cut production. The same goes with other global players as central banks raise interest rates. That will hit dry bulk carriers first and foremost – those companies that ship iron ore, grains, coal, etc. However, we don’t expect demand for container ships to sour anytime soon. In fact, Global Ship Lease has slowly climbed the ranks in our top marine shipping stock search results for financial pros over the last few months. That lends itself to the same thesis we see in the market. Let us walk you through our case and see if you don’t agree.

Man who called 2020 Crash: Huge Event in 2022 (Sponsored) A historic event in 2022 will cause a massive shift in the wealth divide. It could soon impact the wealth of thousands of retirees.

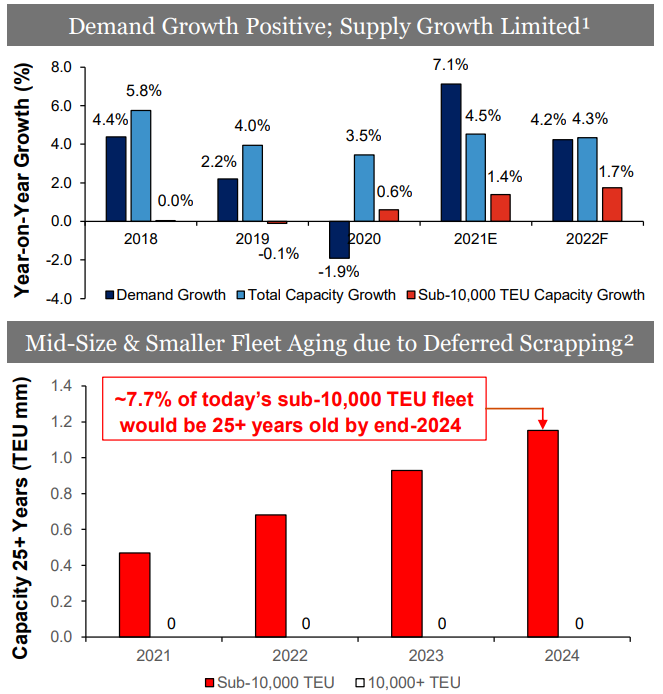

Global Ship Lease’s Business Based out of the United Kingodm, Global Ship Lease owns and charters containerships of different sizes under fixed-rate charters to container shipping companies. GSL’s focuses mainly on small and mid-size containerships, of which it owns 65 with 23 being recently added. In the company’s most recent earnings report, management laid out their expectations for demand and capacity growth over the next year. With total capacity growth set to only meet the demand growth in 2022, that implies charter rates should remain high for the remainder for the year. Management has managed to capitalize on the higher prices by adding 21 new charter agreements in 2021 that put another $897 into backlog.

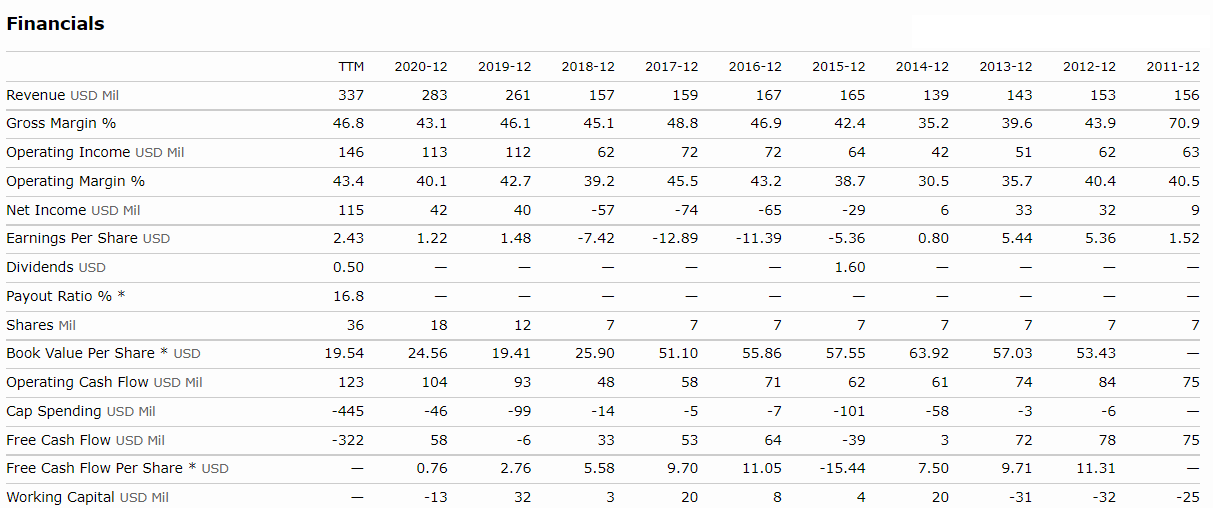

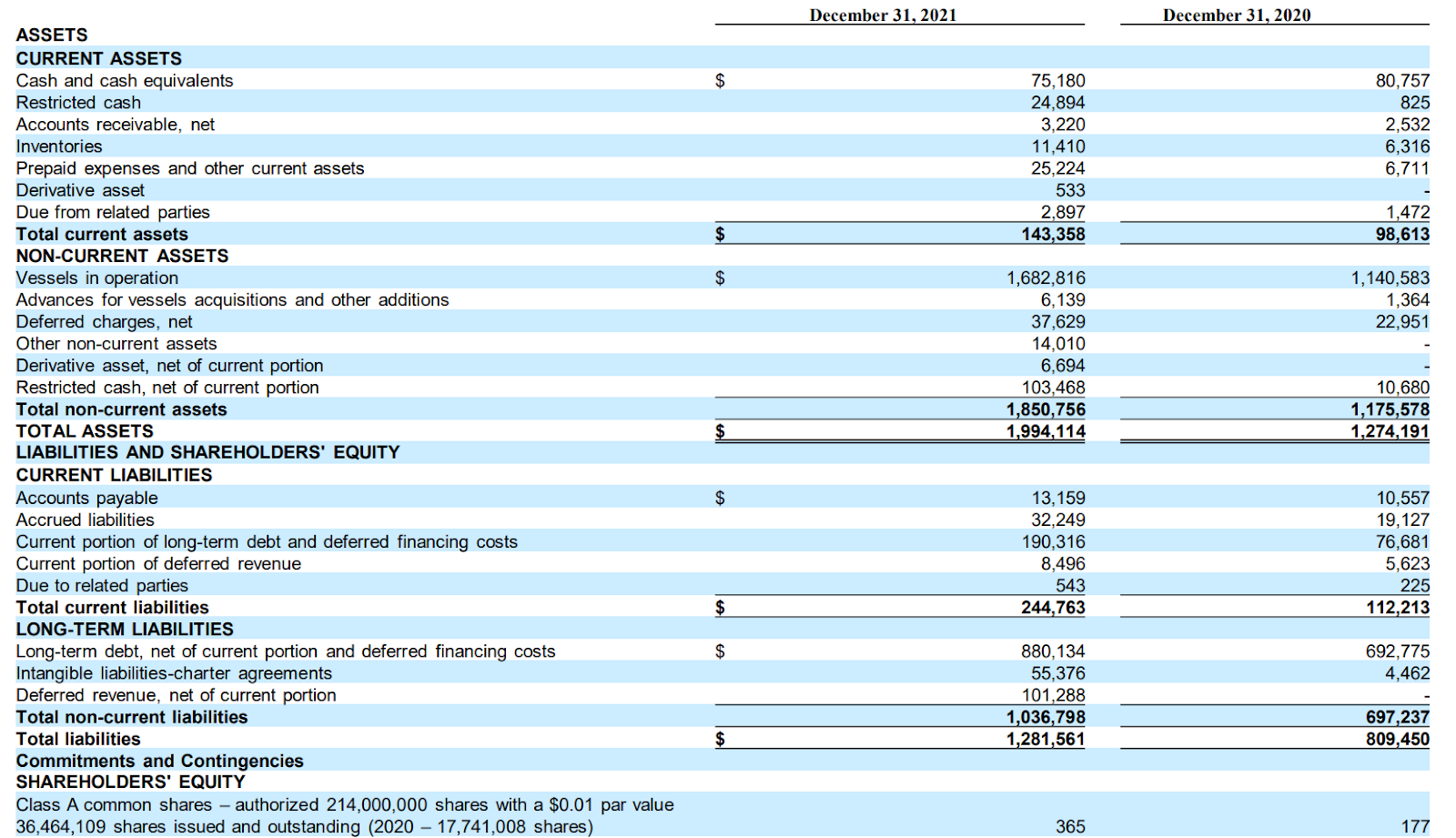

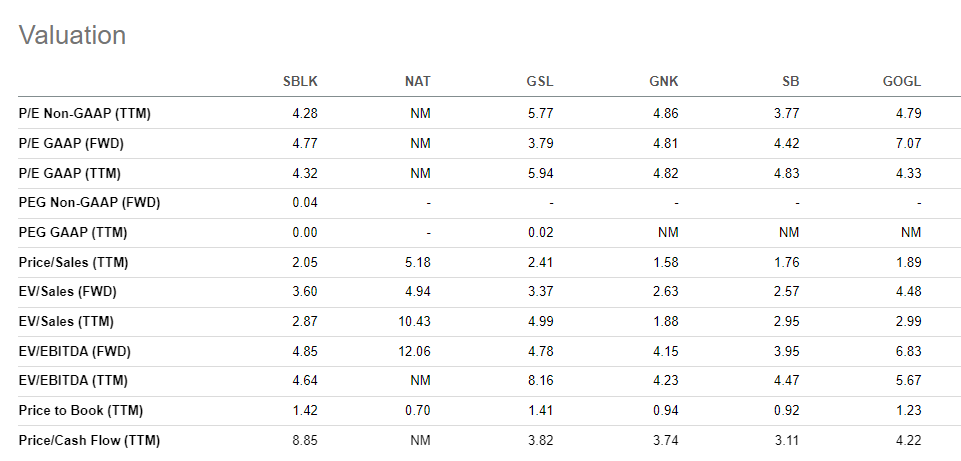

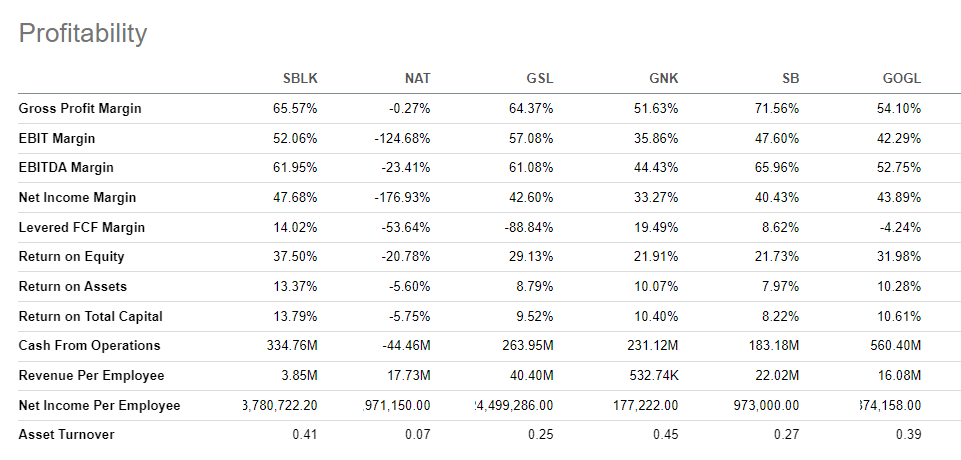

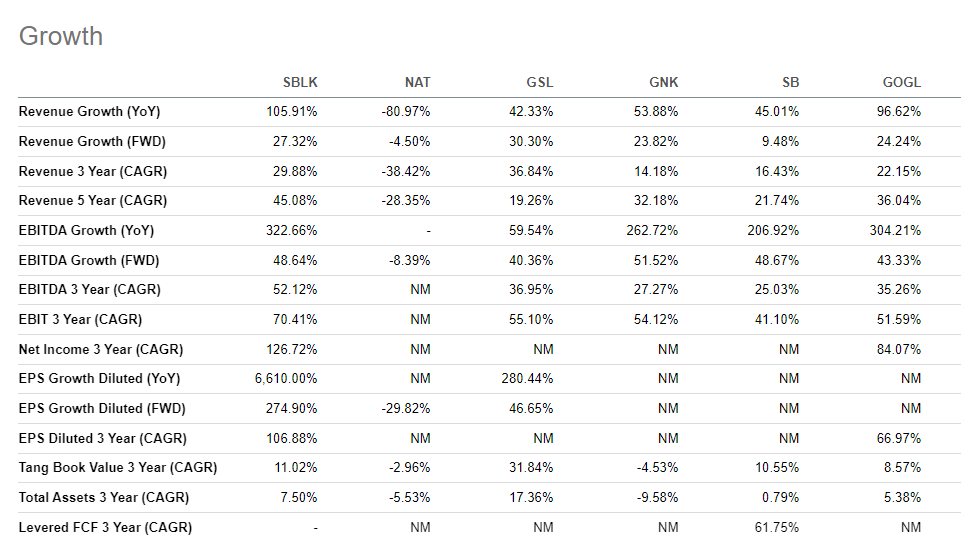

Financials Prior to the shipping boom, GLS operated a healthy business with fairly consistent margins and returns for shareholders. As was evidenced in 2015 and this past year, the company is known for issuing dividends from time to time. However, we’d be remiss if we didn’t describe the major transformation to its balance sheet. In 2019, GSL owned 39 vessels. Today, that’s at 65. While the company has taken on debt to finance the purchases, it’s done so in a smart fashion, with none of it due before 2024. High cash flows helped as well. That reduced the company’s debt payments by $21.2 million annually. While that’s resulted in some shareholder dilution, we believe the company’s doing so at a time that takes advantage of market opportunities. Plus, the company has authorized buybacks of $40 million and is paying another quarterly dividend in Q1 of 2022. Valuation Turning to valuation, we took Global Ship Lease and compared it to several other dry bulk carriers as well as the oil shipper Nordic American Tanker (NAT). Compared to the dry bulk and oil carriers, GSL trades at a lower forward P/E ratio and price to sales ratio. While it has close to the best price to cash ratio, Safe Bulk (SB) does come in slightly lower, but not by much. Next, we wanted to compare profitability ratios. GSL has one of the better gross margins, but really shines when it comes EBITDA and EBIT margins. The company also has a net income margin that’s comparable to the best in the group. Lastly, we wanted to look at the growth metrics. Here, GSL shows solid multi-year revenue growth as well as the best forward-looking revenue growth. Our Opinion – 9/10 It’s certainly tough to buy a stock that’s up as much as GSL. And while we’d prefer a pullback when prices have been so volatile, it’s tough to look at these valuation metrics and not see the potential here. Given the company’s spend on growing its fleet and high cash flow, we expect revenues to increase dramatically in the coming years while interest expenses hold or decrease from current levels. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |