|

Proprietary Data Insights Financial Pros Top Stock Searches Last Week

|

|

Stock Analysis |

Buy Amazon? No |

If you own any major index, you own Amazon (AMZN). Do a 360 degree turn where you stand and chances are something in your eye line came from Amazon. From a garage startup that traded books to a worldwide behemoth, Amazon is one of the largest companies in the world. When news hit that the company planned to do a 20 for 1 split, finally lowering the share price from nearly $3,000, investors went wild. In search results amongst financial pros for last week, the stock jumped to #5 among the top searches. Astonishingly, we’ve never taken a deep dive into the stock that puts packages at our doorsteps making everyday Christmas. What most people don’t realize is that Amazon was unprofitable on paper up until 2014. It’s only been in the last decade that its actually turned a positive earnings per share, and that’s largely due to Amazon Web Services (AWS). We wanted to take an objective look at this retail behemoth that’s managed a 10 year average growth rate near 30%. Here’s what we found.

These AI Stocks Could Explode in March (Sponsored) Did you know that A.I. is one of the most accurate tools ever conceived for maximizing opportunities and avoiding losses in a volatile market such as the one we’re facing now? Now more than ever, today’s markets are globally connected. By utilizing the power of A.I., VantagePoint has continued to empower traders for nearly 40 years. Our goal is simple: Identify trades that will help you grow your nest egg exponentially while protecting your hard-earned capital. Sign up now for a FREE live training session.

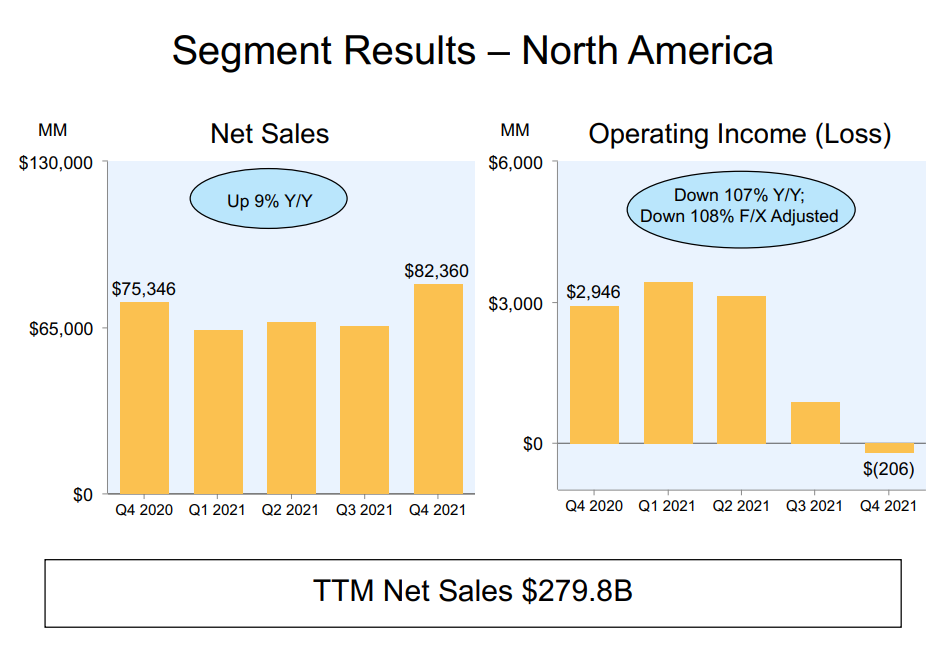

Amazon’s Business Amazon needs no introduction. If you don’t know who they are you probably shouldn’t be investing. The $1.5 trillion market cap company has more than 1.6 billion employees and does nearly $470 billion in sales annually. While the company has its hands in everything from grocery with Whole Foods to cloud with streaming content, its business is primarily divided into three categories: North America (60% of sales), International (27% of sales), and Amazon Web Services (13% of sales). AWS is the fastest growing segment at 37.1% YoY, with international at 22.4% and North America at 18.4% Yet, AWS comprises 74.5% of profits, North America 29.2%, and international at a loss of 3.7%. Financials We wanted to quickly move to the financials because that’s where the meat of the story is. And we want to first look at operating expenses. Given Amazon’s massive logistics and fulfillment network, we wanted to see how much inflationary pressures would weigh on its operations. Sure enough, as a percentage of sales fulfillment costs rose substantially from 14.3% to 16% in 2021. That led to an increase in sales that coincided with an operating loss in Q4 of 2021 in North America. The decline was mirrored by a similar decline in operating income for international sales. Liek most businesses, Amazon faced inflationary pressures from higher wages and transport costs as well as labor issues due to a tight market costing them $4 billion. However, the company has had to nearly double operations in the last two years as demand exploded when the pandemic hit. That helped propel the company to a 37% YoY sales growth in 2020. Yet, the most recent quarter was a paltry 9.44% Despite management’s $10 billion buyback, bears wonder whether Amazon’s heavy growth days are behind it. To be fair, the company still generates $46 billion in cash from operations, and capital expenditures should ease in the coming years. What many people don’t realize is that Amazon has $282 billion in long-term liabilities, most of which come from the $55 billion in debt and $67.7 billion in capital leases. At a cost of $1.361 billion annually, management might want to think about bringing this down as interest rates rise. Valuation Here’s where things get tricky. Amazon has never been known to deliver on traditional valuation metrics because of its immense growth. Consequently, we get an odd picture. Compared to the rest of the consumer discretionary sector, Amazon is incredibly expensive. Yet, it’s probably best to compare it to technology, which still comes in much higher than the average. Yet, Amazon trades much lower than its 5-year average on nearly every category. And that’s what’s so odd. Investors are willing to pay a premium for Amazon, just not the same one as they would have in the past. That’s not entirely surprising given the forward revenue growth forecasts are 17.96%, far below the historical average of 24.52%. Our Opinion – 4/10 We love Amazon as a company. As a stock, it’s tough to make a case for a $1.5T market cap to keep growing at +20% YoY and retain profitability as inflation hits it more directly than most. If shares were to get carved by a third or half, it becomes an attractive investment. Yet, when we look at quality large cap names, Apple (AAPL) is more our speed. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |