|

Proprietary Data Insights Financial Pros Top Apparel Stock Searches This Month

|

|

Stock Analysis |

Can You Find Profits Under There? |

Some things in life we just cannot live without. Food, water, and underwear. Unless swimsuits are a staple of your wardrobe, underwear is a part of your everyday life. Hanesbrands Inc. has been a leader in the industry for over a century. Today, the company owns well-established brands including Hanes, Champion, and Playtex to name a few. Although the company landed in sixth amongst the top apparel stock searches for apparel companies, the valuation relative to its peers on the list was quite compelling. And when we took a closer look at the stock, we found that its recent non-cash financials had been weighed down by the divestiture of its European innerwear operations. However, the company hasn’t seen solid growth in nearly three years. And with Michael Jordan no longer in their commercials, we wanted to know if Hanes’ best days were behind them. Hanesbrands Inc. Business Based out of Winston-Salem North Carolina, Hanesbrands designs, manufactures, sources, and sells apparel and undergarments for men, women, and children in the U.S. and internationally. The company’s brands include Hanes, Champion, Playtex, Bali, Just My Size, Barely There, and Wonderbra. Hanesbrands operates four main segments:

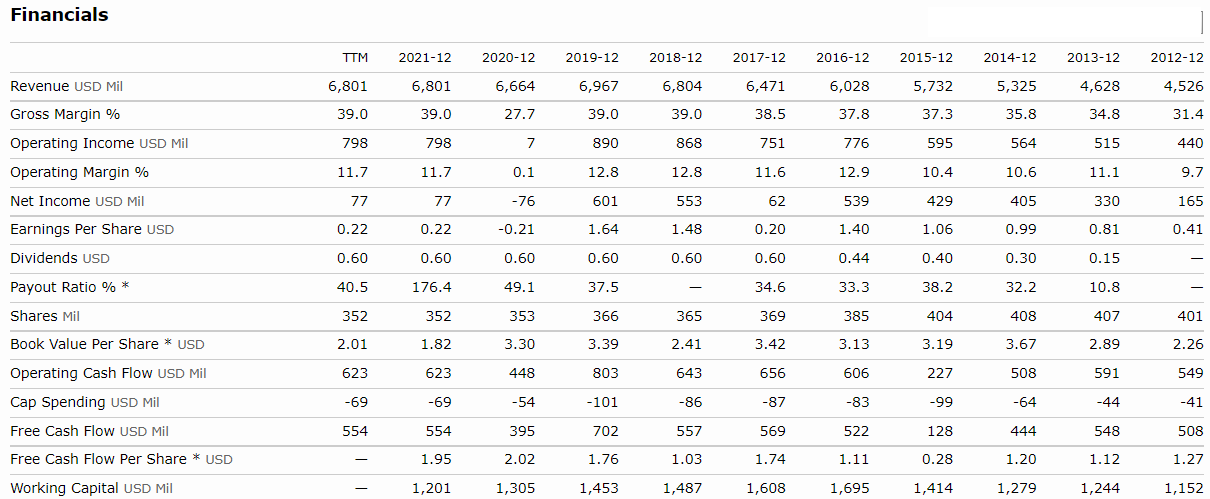

In 2021, management unveiled a turnaround strategy to streamline operations known as the Full Potential Plan. This strategy aimed to grow the burgeoning Champion brand, reignite innerwear growth, drive customer-centricity, and focus on the portfolio. This came on the back of the company’s divestiture from its European Innerwear operations which is expected to be completed this quarter. Management also plans to divest its U.S. Sheer Hosiery business. With a renewed focus on high-growth categories, Hanesbrands has spent more money on marketing to drive higher point-of-sale trends and increase market share. However, that’s led to increased spend on expedited shipments to ensure product rollouts during the last year’s supply chain congestion. Management expects this elevated spend to continue through the first half of 2022. However, we see this as more of a kitchen sink type event where they toss out all the costs at once so they leave nothing but upside afterward. Financials Hanesbrands isn’t what you would call a massive growth company. However, the company managed a 10-year average revenue growth of 6% going into 2020. Right now, management expects 2022 growth in the single digits. In 2021, Hanesbrands took a $444 million adjustment to its net income due to the divestiture of its European Innerwear operations. Without that hit, Net income would have been a robust $521 million with a margin of 7.7%. Some analysts say that Hanesbrands can’t maintain its current dividend payout, which yields 4% annually. However, the company generates enormous amounts of operational and free cash flow every year. We don’t see any danger. However, the company does carry a hefty amount of long-term debt at $6.4 billion with only $536 million of cash on hand. That’s led to interest expenses that exceed 2% of revenues at times. We’d like to see them repurpose the dividend to bring these costs down. Valuation As we mentioned earlier, Hanesbrands stood out when we looked at its valuation measures relative to the others from our proprietary data. Even with the discontinued operations, Hanesbrands trades at one of the cheapest price-to-earnings multiples looking back over the last 12 months. While it doesn’t have the absolute cheapest forward looking P/E ratio, it’s pretty darn close to the best on this list. What’s equally impressive is its low price-to-sales and price-to-cash ratio. The only company that beats it in both of these categories is Phillips Van Heusen (PVH). However, PVH’s sales have dwindled over the last decade. Despite YoY growth of 15.32%, PVH is expected to sell less next year. And its 5-year average sales is nearly 50% lower than HBI’s. That’s not to say HBI’s sales have been particularly robust. They saw a downturn during the pandemic. However, the type of clothing they sell is more resilient to economic cycles and acts more like a consumer staple than a consumer discretionary product. Lastly, we wanted to come back to the net income margin we discussed earlier. Even when you exclude the one-time item, the net income margin is still several percentage points below some of its more popular peers. That’s why we think it’s critical management pay down their debt to expand margins, especially when they’re investing in growth. Our Opinion – 6/10 When we look at low growth companies, we want to see seriously deep value. Hanesbrands has the potential to become a better company. We just need to see them prove it. With shares priced at just under $15, we’d rather wait for a selloff that took the stock closer to $10. That may not happen, and it might be unfair given the hefty dividend. But we’ve covered companies with better prospects and higher dividends. So we feel it’s justified here. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |