|

Proprietary Data Insights Financial Pros Top Credit Services Searches This Month

|

Use BNPL, Stay Away From The Stocks |

We stand by the position we took in March on Buy Now, Pay Later (BNPL) stocks: … it’s hard to believe that BNPL services can truly outperform credit card companies, let alone compete with their war chests. In all likelihood, we expect more established players, who are already integrated with retailers, to simply offer the same products, pushing out companies like Affirm (AFRM) that are one-trick ponies. That’s why we prefer companies like Visa (V) or American Express (AXP). Source: Google Finance Since we wrote about BNPL in mid-March and suggested avoiding pure plays in the space, Affirm Holdings (AFRM), a heavily-searched BNPL stock in our proprietary Trackstar database, is down roughly 40%. These companies face two major headwinds:

Invest in leaders and true disruptors. Reinventing old school layaway (ask anybody over 40 what that is) doesn’t feel all that disruptive. This said, we’re not exactly freaking out over BNPL debt the way lots of other people are.

|

|

Debt |

The Debt Bubble That’s Unlikely To Burst |

Key Takeaways:

Source: Lending Tree In case, you couldn’t find someone over 40 or you’re Gen X or older and simply can’t remember, layaway used to be my Mother’s jam. We’d go to K-Mart. She’d pick out a bunch of stuff, bring the items to a counter in the back of the store, and leave them. Every few weeks, we’d go back to the same counter. She’d make a payment – in cash. After a few visits, we were paid in full. A K-Mart employee collected our merchandise from the back, handed it over, and we were on our way. We used layaway for two reasons:

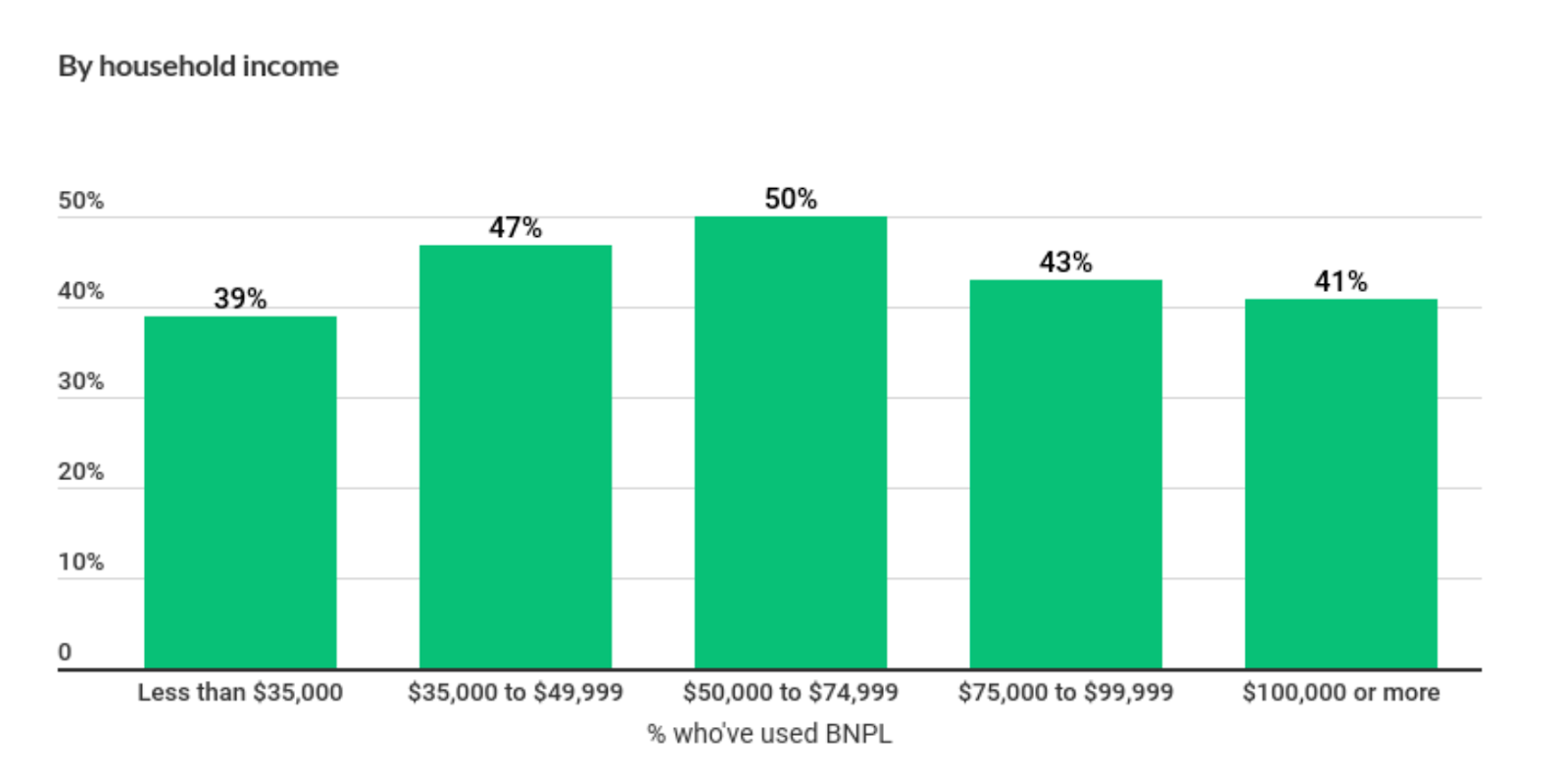

Concern Over BNPL BNPL is the modern day iteration of layaway, except you get your merchandise right away and pay over a handful of, often, interest-free installments. As the chart shows, consumers across incomes heavily use BNPL. There’s significant concern over BNPL, with some people calling it a debt bubble about to burst. Expect increasing government regulation of BNPL in the coming weeks and months. There’s concern, in part, because 42% of BNPL users say they’ve missed a payment. Of these people, 23% regret using BNPL. Close to 70% admit they’ve spent more than they could afford without a BNPL option. Sounds A Lot Like Credit Cards Earlier this month The Juice sounded the alarm over the debt bubble that really should worry us: Revolving debt (that’s credit cards) surged by $35.3 billion in March. That’s a 21.4% annual increase and blows away the $16.2 billion monthly increase we saw in February. If delinquencies follow – and we bet they will – we’ve got a problem. Credit card debt piles up. You carry a balance. You can’t keep up with it. So you make the monthly payment and barely dent your balance. Worst case – you can’t afford the monthly payment. You wind up in collections. For comparative perspective, by 2025, BNPL is expected to comprise 5.3% of global transactions, or about $438 billion. Credit card debt reached $841 billion in Q1 of this year. Total household debt (including credit cards, but not BNPL) hit a record $15.84 trillion. So BNPL remains a relative blip on the radar screen. Why Is BNPL So Popular? Go back to the widespread use of BNPL across incomes. And the second point on why Mom used K-Mart layaway so much. Even if you’re comfortable, there’s something about parting with money all at once that’s unsettling. It messes with our sense of cash security. Like with credit cards, you have a choice to make at the point of purchase. We often charge something or, lately, use BNPL, not because we don’t have the cash to cover the purchase in full, but because we don’t want to part with all of the cash, all at once, to cover the purchase in full. I do this all the time. Occasionally with BNPL. And every single time Airbnb asks if I want to split my payments into two installments. There’s something comforting about keeping your checking account balance that much higher, for that much longer. Until you raid it to pay off your debt. [instory_ad] The Bottom Line: It’s funny to see people freaking out over BNPL. Where were they when credit card debt spun and stayed out of control? No matter the debt – it comes down to financial discipline. With credit cards, it’s about paying your balance in full every single month. Collect your airline rewards or whatever. Pay no interest in the process. With BNPL, it’s about ensuring you have the cash to cover your initial and subsequent payments. Debt isn’t the problem – be it debt we’re desensitized to, such as credit cards, or debt we choose to suddenly get hysterical about, such as BNPL. It’s how we use that debt. If you can use BNPL, or credit cards for that matter, to feel cash secure, it’s not a problem. It’s only a problem when you use debt to live beyond your means. BNPL didn’t start that fire.

|

News & Insights |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |