|

Proprietary Data Insights Financial Pros Top Software Infrastructure Searches This Month

|

|

Stock Analysis |

Has This Tech Stock’s Bubble Burst Again? |

With the S&P 500 and Nasdaq entering bear market territory, investors wonder how much worse can get things? Some economists believe that a recession isn’t out of the question. After all, oil prices are through the roof, and inflation runs wild. The S&P 500 experienced its 7th straight losing week. The last time that happened was 2001, during the dot-com collapse. Some analysts on Wall Street believe that it will get worse for stocks, even resemembling a dot-com-like collapse. While most internet-related companies got wiped out during the dot-com bubble, a few not only survived, but went on to thrive. They include Microsoft, Amazon.com, Adobe Systems, eBay, and Oracle (ORCL). Now usually, Oracle receives a fair amount of interest from both retail and financial pros. Yet, it landed at #7 for the top software as that interest waned since the start of May.

Year-to-date, the stock is down 16%, but from its highs in 2021, over 31%. Will ORCL survive this latest market crash? And is now a good time to get in? Check out our analysis below. Oracle Corporation (ORCL) Business ORCL is a software company that offers enterprise solutions. Oracle offers cloud software as a service. In addition, it offers:

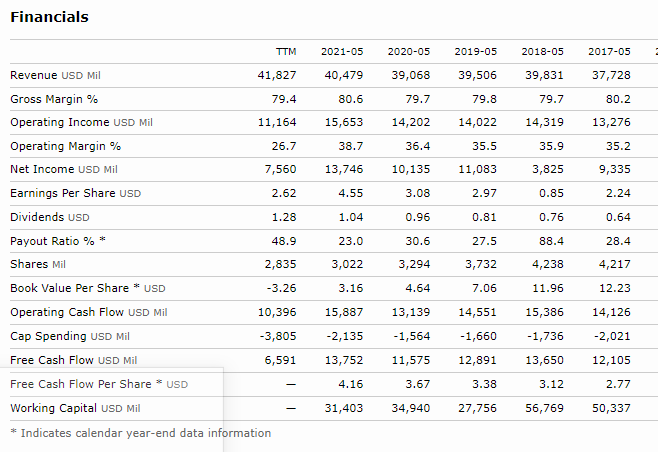

The company provides cloud and licenses business’ infrastructure technologies, like Oracle Database and Java. Government agencies, educational institutions, and public and private businesses all rely on Oracle systems for a variety of applications. An impressive client roster includes Hilton, Vodafone Group, Albertsons Companies, Canon Inc., DHL Supply Chain, Dallas Fort Worth International Airport, Akamai Technologies, Zoom, Rutgers University, Kraft Heinz, and First Bank of Nigeria, just to name a few. In fact, ORCL has over 430,000 customers and over 200,000 cloud community members. ORCL reported total cloud revenue (IaaS plus SaaS) of $2.8 billion, up 245 and 26% in constant currency. The firm’s Fusion enterprise performance cloud revenue was up 33% and 35% in constant currency. And its Netsuite enterprise performance cloud revenue shot up 27% and 29% constant currency. Financials

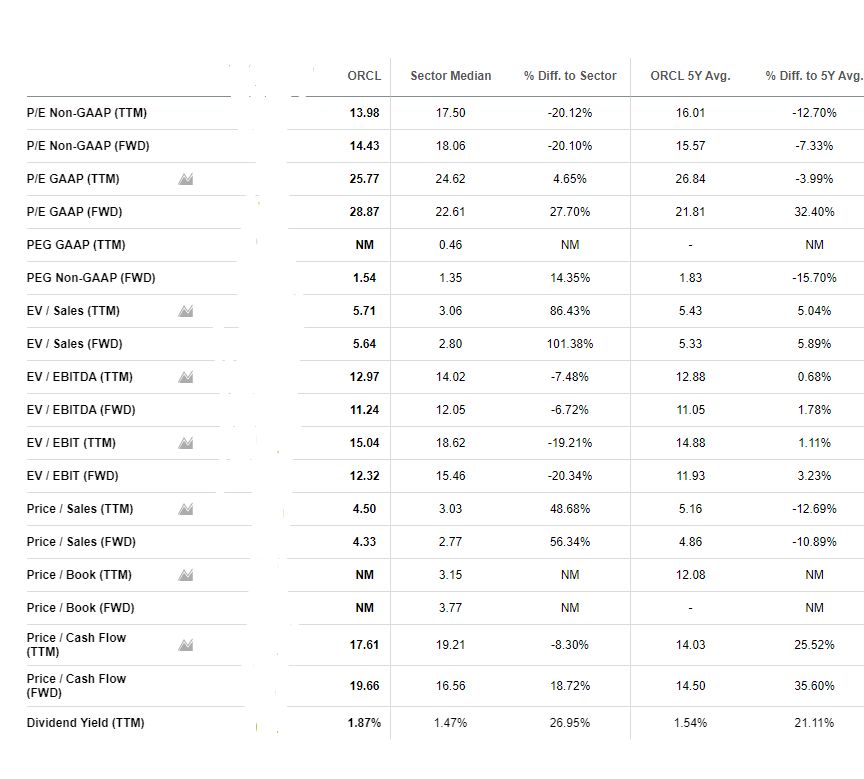

ORCL delivered over 7% constant currency revenue growth in Q3 2022, its highest quarterly organic growth rate since it began its transition to the cloud. The company operates at an extremely high gross margin. In 2021 it clocked in a gross margin of 80.6% The firm has an EBIT Margin (TTM) of 37.93%, which is insane compared to the sector median of 8.69%. In 2021 ORCL had a current ratio of 2.3x, which means its assets were 2.3x greater than its short-term liabilities. Furthermore, ORCL in 2021 had a quick ratio of 2.15x, which means its highly liquid assets were 2.15x greater than its short-term liabilities. The capital structure for ORCL is as follows: total debt of $78.41 billion and cash upwards of $23 billion, and a market cap of approximately $183.12 billion. Valuation ORCL has a price-to-sales ratio of 4.5x, which is worse than the sector median of 3.03x. One thing investors are paying closer attention to is P/E ratio. High P/E firms are getting punished in this market. ORCL has a P/E ratio of 13.98x, which is better than the sector median of 17.51x Although it isn’t a high yield, ORCL does offer an annual dividend of $2.80 per share. The price to cash flow ratio at 17.61x is slightly better than the sector median. However, its forward price to cash flow of 19.66x is significantly about the sector median. Nonetheless, its cash balances are robust with significant cash generated each year. Our Opinion – 7/10 Tech stocks have gotten slaughtered in 2022. Some investors are comparing this sell-off to the dot-com bubble. ORCL survived the dot-com bubble, and we believe it will continue to thrive regardless of how bad the economy gets. And while not known for its growth, the firm is showing improvements in its cloud business, as witnessed by its latest earnings release. If you want to have some exposure to tech, we believe it is one of the better stocks to invest in. We like it for the next six to twelve months. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |