|

Proprietary Data Insights Financial Pros Top Social Media Stock Searches This Month

|

|

Stock Analysis |

A Bad Stock That Got Worse

|

|

We don’t typically cover a poorly run company we know is bad. Yet, interest in Snapchat (SNAP) skyrocketed to the point where we felt an obligation. Searches for the social media company skyrocketed after shares took a beating, cutting the price of the once beloved $80 stock into in the teens. And it’s indicative of the broader story behind the company. Imagine launching a startup and one day receiving an email from one of the wealthiest people in the world, telling you that they love your business and want to have a sit-down. Well, that’s exactly what happened to SNAP’s Evan Spiegal when he received an email from Mark Zuckerberg’s Facebook in 2012. Shortly after that email, Facebook offered to buy SNAP for $3B. Spiegel declined the offer, which ten years later, made Spiegal look like a genius when SNAP reached a $120 billion valuation. And that’s just the beginning of this poorly run company.

7 Free Stock Picks (Sponsored) Don’t let market volatility get you down. Schaeffer’s Top Stock Picks for 2022 are exactly what you need to profit in any market. My team of traders and I put together seven hot stock picks for 2022 that every investor needs on their radar, ASAP! This complimentary gift is yours today! Get ready to deep dive into the 7 hot stocks that we believe you need on your radar this year. Click here to gain instant access! FREE

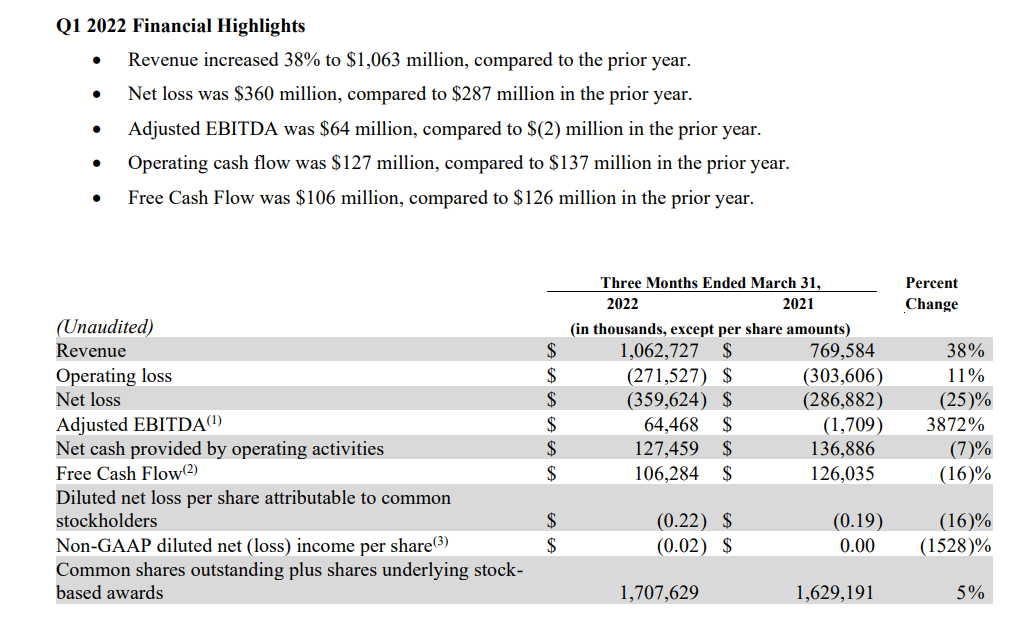

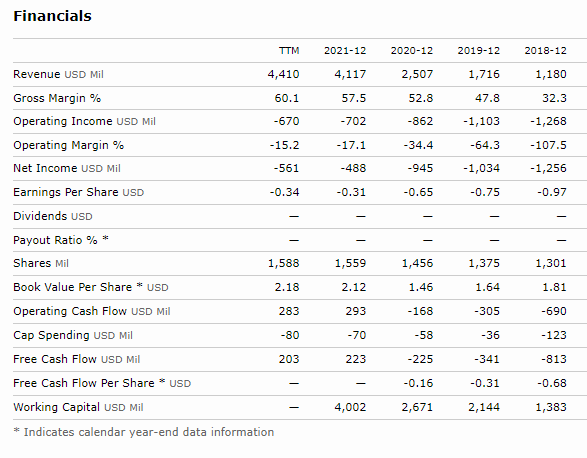

Snap Inc. (SNAP) Business SNAP is a social media company. It offers Snapchat, which offers functionalities like Camera, Communication, Snap Map, Stories, and Spotlight, which allows users to communicate visually through short videos and images. These short videos are viewed once and then deleted forever, which is odd to say the least. SNAP also offers an eyewear product called Spectacles. It connects to Snapchat and captures photos and videos from a human perspective. Although SNAP is mainly recognized for being a social media company, that is not how the firm defines itself. Rather, they would like to be known as a camera company. Snapchat has 332 million daily active users. It has over 6 billion AR Lens plays per day on average. And over 250 million daily active users engage with augmented reality every day. Over 75% of the users on the app are of the ages 13-34, and can be found in over 20 countries. 90% of its users are between the ages of 13 to 24 years old. The firm has over 800 partners. SNAP generates a majority of its revenues from advertisers on its platform. Snapchat’s biggest problem is that many users see it as a ‘fad.’ The stickiness relative to other social media platforms just isn’t as strong. Financials Like most social media platforms, Snapchat lived and died by its growth. After nearly doubling from 2020 to 2021, revenue gains slowed markedly as advertisers pulled back on spending. Still, the company carries a gross profit margin (TTM) of 60.13%, which is considerably better than the sector median of 50.74%. Thankfully, the company began to turn cash flow positive in 2021. That won the hearts of investors, if only for a little while. In 2021 SNAP had a current ratio of 5.70x, which means its assets were 5.70x greater than its short-term liabilities. Furthermore, SNAP in 2021 had a quick ratio of 5.59x, which means its highly liquid assets were 5.59x greater than its short-term liabilities. The capital structure for SNAP is as follows: total debt of $4.22 billion and cash upwards of $5 billion, and a market cap of approximately $23 billion. So the good news is that the company remains well-capitalized even if it’s not profitable. Valuation

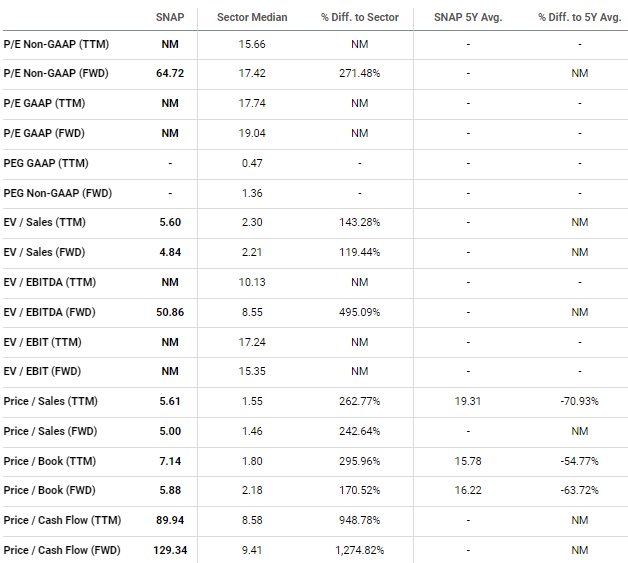

SNAP has a price-to-sales ratio of 4.54x, which is worse than the sector median of 1.37x and a key metric for a high-growth company. The company is an absolute valuation nightmare. Its price to cash flow ratio is 81.74x, which is horrendous when compared to the sector median of 7.96x. As you can see from the above image, it scores poorly on nearly every valuation metric. Our Opinion – 3/10 SNAP has some exciting products in the pipeline. However, the company doesn’t make enough money to truly justify its current price. It’s incredible to believe that less than a year ago shares were trading above $83 per share. But now we’ve seen a decline of more than 65% The firm recently announced that growth is slowing down due to the macroeconomic environment. And let’s face it…this isn’t a camera company. It’s short-form video without a sustainable advantage right now. This is a toxic stock that survives because it managed to become cash-flow positive last year. |

|

Want to get content like this directly to your inbox? |