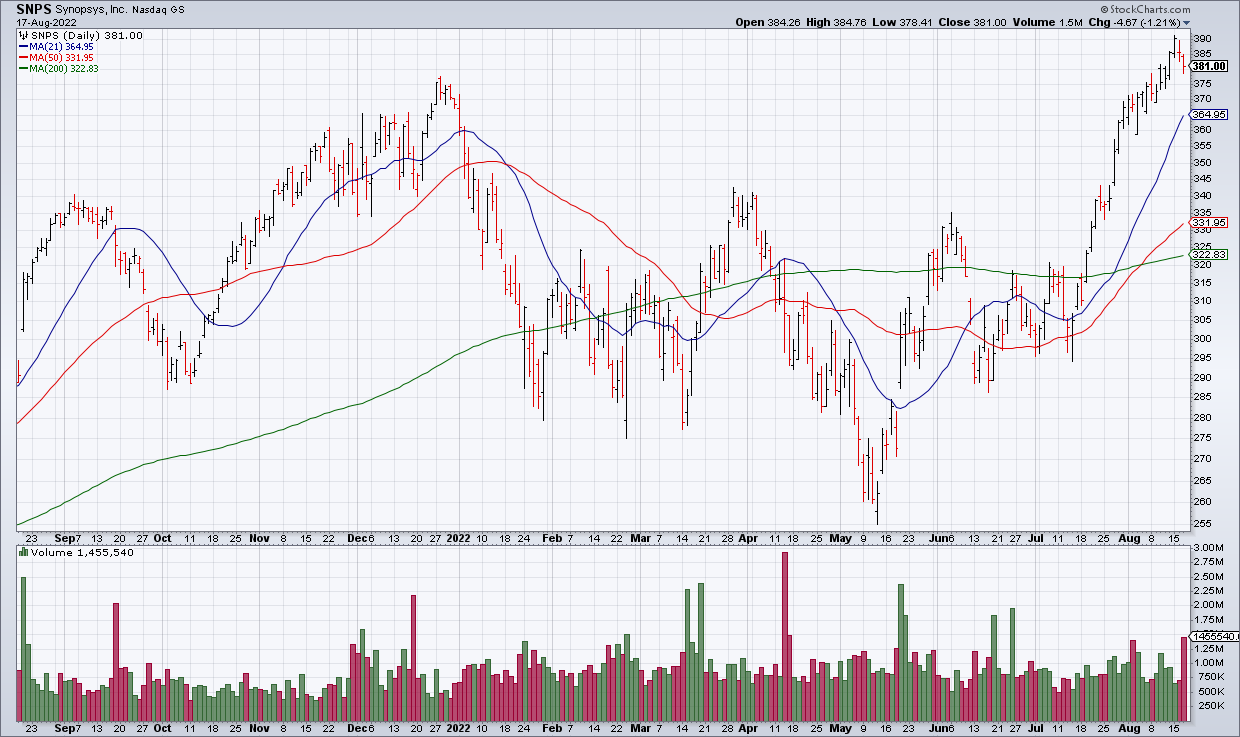

Synopsys (SNPS) – the largest maker of software for semiconductor design – reported 2Q22 earnings just now. While semiconductor companies have been warning recently SNPS may be immune. That’s because semiconductor makers don’t want to fall behind in an always fast evolving space and so are loathe to skimp on Research & Development (“Still Time To Chip In On Synopsys” [SUBSCRIPTION REQUIRED], Dan Gallagher, WSJ).

SNPS 2Q22 results support this thesis: Revenue was +18%, EPS +16% and they increased their outlook for the fiscal year ending in October. While the stock is quite expensive at more than 40x current year EPS guidance, SNPS is likely a long term winner as semiconductors become more and more integrated into all sorts of products.