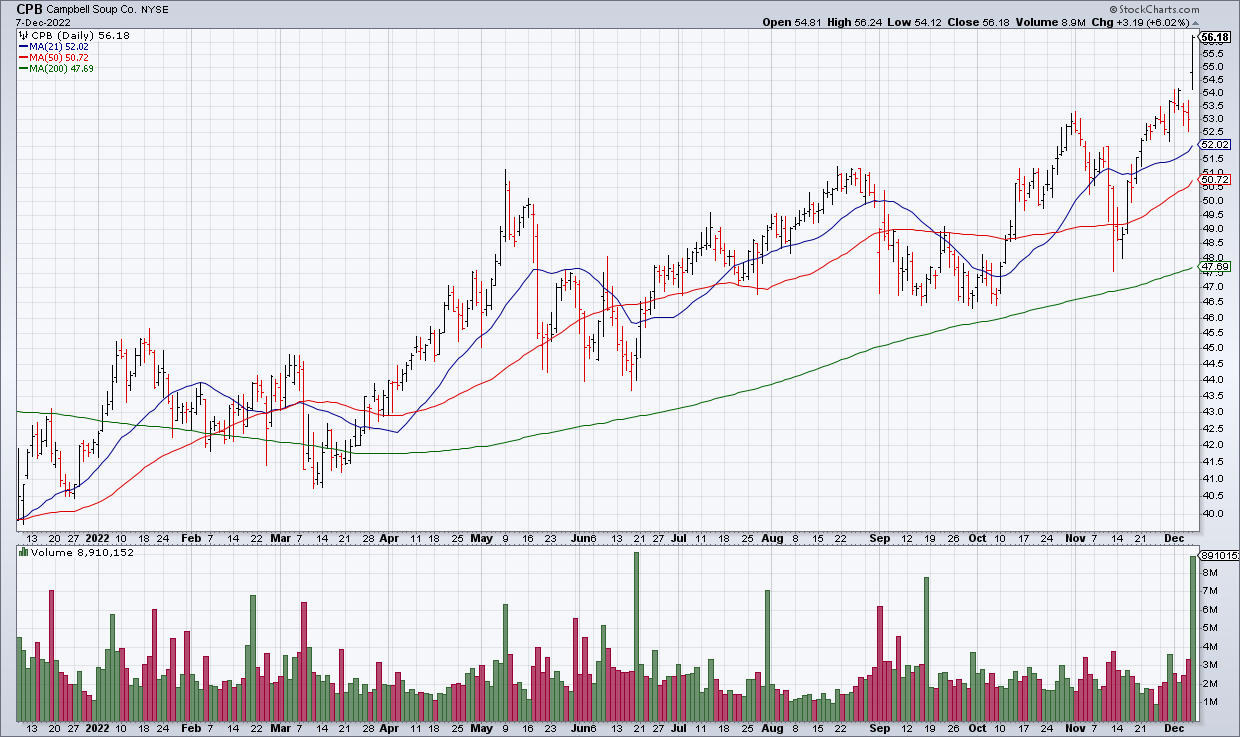

One of my best investments this year has been Campbell Soup (CPB). I bought it when it sold off after earnings nine months ago for $42.25. It closed Wednesday at $56.18 after another great earnings report – up 33%. At the time I called it “the perfect stock for this market” and that still holds.

Some people mistakenly assume CPB is just the stodgy soup we all know but it actually has a great portfolio of food brands such as Goldfish, Kettle and Pepperidge Farms. You can see all their brands here. As inflation and weakening economic growth squeeze consumers CPB’s staple of high quality brands represent affordable options.

But don’t just take my word for it. CPB’s 3Q22 report out Wednesday morning confirms it. Organic sales were +15% resulting in a 15% increase in EPS compared to a year ago. CPB also raised its FY23 organic sales guidance from +4-6% to +7-9% and its EPS guidance from $2.85-$2.95 to $2.90-$3.00. Clearly the stock is running on all cylinders – and I don’t expect that to stop any time soon. Nevertheless after such a big run you’ll want to wait for a pullback as I did when I first bought it in March. Keep an eye out for your opportunity.