|

Proprietary Data Insights Financial Pros Top Oil & Gas E&P Stock Searches in the Last Month

|

|

Energy |

Over Two Decades of Dividend Hikes |

2023 is poised to be another challenging year for investors. The name of the game very well may be survival. Many financial pros believe the companies that outperformed in 2022 are likely to do so again. That’s probably why we’re noticing so much search activity in oil and gas exploration and production companies in our proprietary Trackstar sentiment indicator. One name that’s popped up on the Trackstar radar is Canadian Natural Resources Limited (CNQ). While it hasn’t been the top oil and gas exploration company financial pros search, our deep dive found it more attractive than its peers. Financial pros are likely impressed by its:

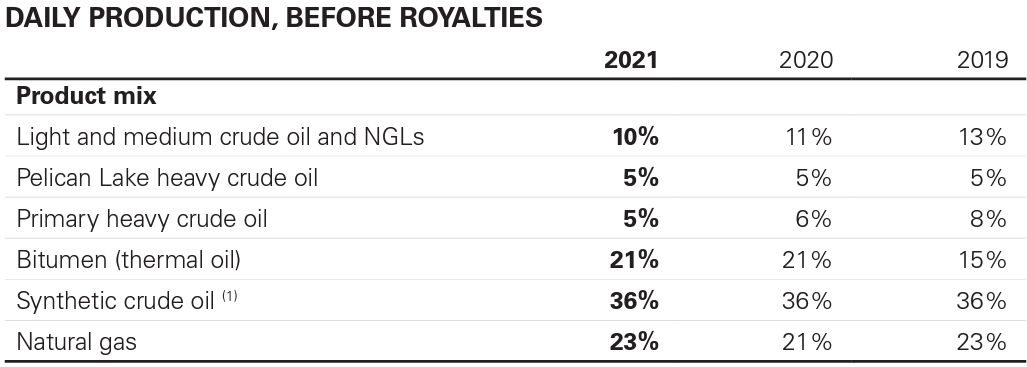

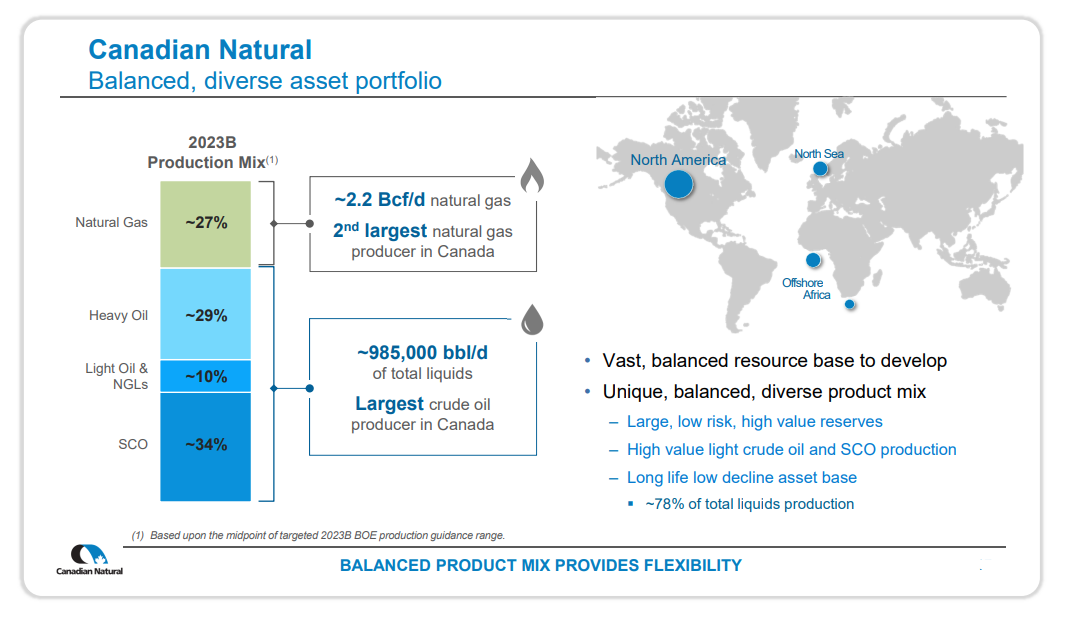

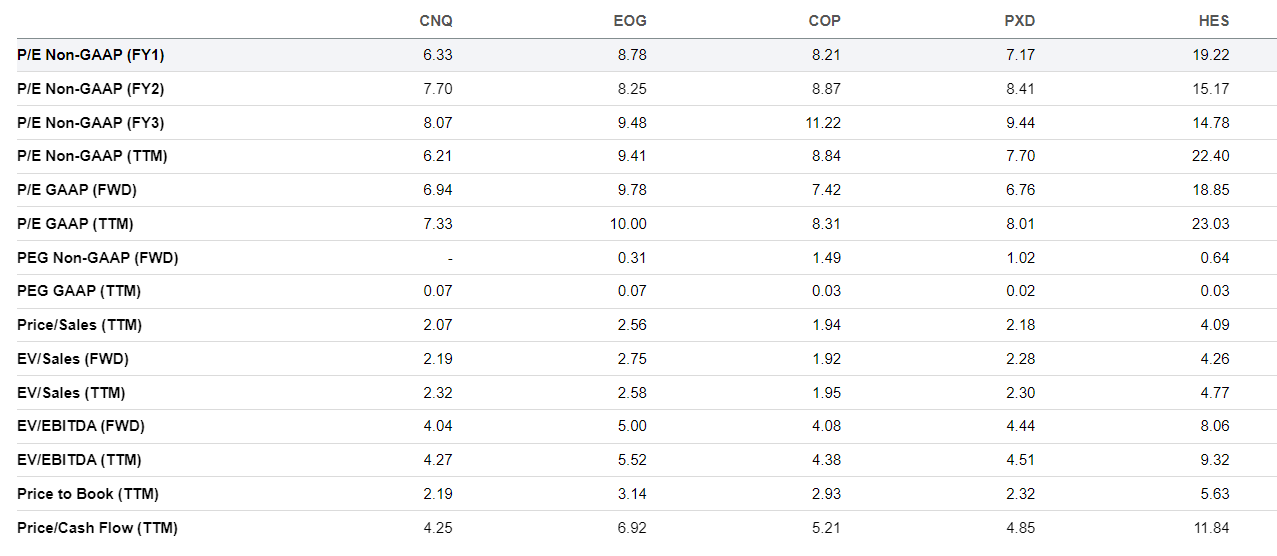

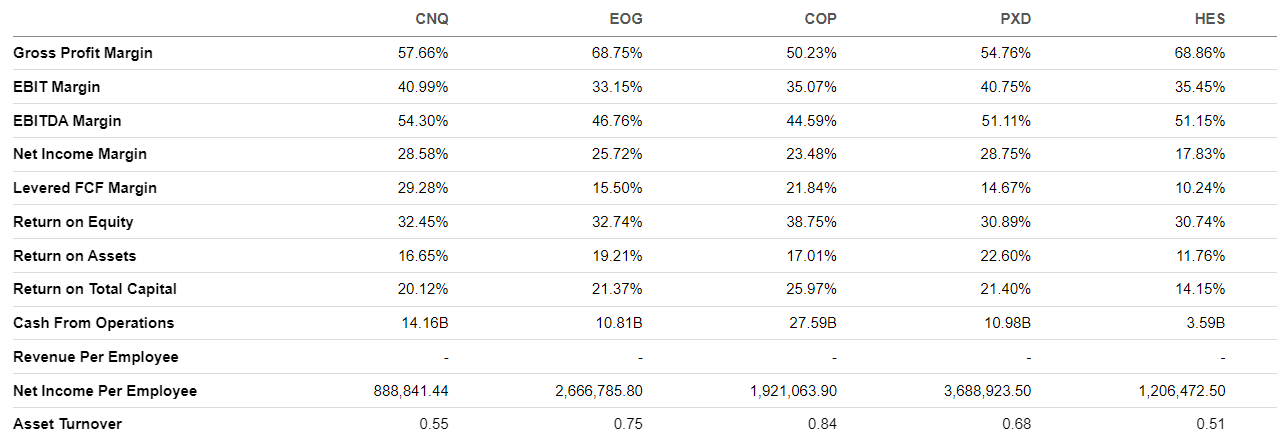

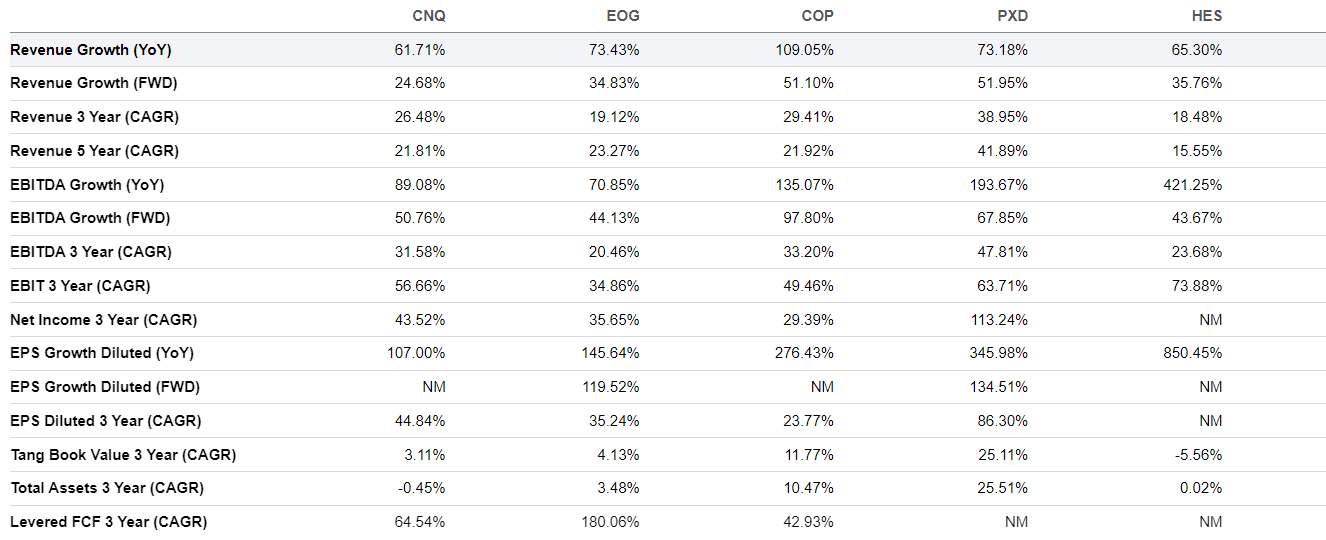

But is it a good investment in 2023 and beyond? Read on for our analysis. Canadian Natural Resources Limited’s Business Canadian Natural Resources Limited is an independent crude oil and natural gas exploration, development, and production company, meaning it lives and dies by the price of crude oil and natural gas. It holds a balanced and diverse portfolio of primarily Canadian-based assets, with international exposure in offshore Africa and the U.K. section of the North Sea. It divides production into light crude oil, medium crude oil, primary heavy crude oil, Pelican Lake heavy crude oil, bitumen, synthetic crude oil, and natural gas. Source: Canadian Natural Resources CNQ boasts the largest natural gas reserves in Canada and is the largest crude oil producer there. Moreover, 60% of its reserves are high-value synthetic crude oil, light crude oil, and natural gas liquids. It gives CNQ a competitive advantage over its peers. For example, long life and low declining assets provide sustainable production and free cash flow even in a lower-price environment. Additionally, CNQ can exercise capital flexibly by cutting spending on low-capital-exposure assets and ramping up production with improving prices. Source: Canadian Natural Resources CNQ focuses on generating free cash flow, maintaining a strong balance sheet, growing its dividend, increasing its share repurchases, growing margins, and getting strategic acquisitions. Its game plan worked well in 2022, as shares gained more than 35%, significantly outperforming the S&P 500. Financials Source: Stock Analysis From 2018 to 2021, CNQ’s cost of revenue climbed from $10.6 billion to $13.7 billion. Meanwhile, its total revenue spiked from $21.0 billion to $30.0 billion during that same period. Over the last 12 months, CNQ generated a whopping $41.8 billion in revenue. Higher realized energy prices helped margins improve substantially, with gross margins climbing to 54.23% and operating margins at 34.45%. The current ratio improved from 0.63x in 2018 to 0.78x in 2021. The debt-to-equity ratio fell from 0.64x in 2018 to 0.34x currently. Since Q3 2022, CNQ has returned $10 billion to shareholders, $4.9 billion in dividends and $5.1 billion through share repurchases. Plus, the company raised its dividend twice in 2022. Valuation Source: Seeking Alpha CNQ trades at a price-to-sales ratio of 2.0x, its lowest since 2018. This level is very competitive compared to its peers’. In fact, it’s lower than EOG Resources (EOG) at 2.5x, Pioneer Natural Resources (PXD) at 2.1x, and Hess (HES) at 4.0x. The largest player in the sector is ConocoPhillips (COP), which has a price-to-sales ratio of 1.9x. But CNQ is cheaper than its rivals, with a P/E GAAP ratio of 7.3x. Compare that to EOG at 10.0x, COP at 8.3x, PXD at 8.0x, and HES at 23.0x. And CNQ has the lowest price-to-cash-flow ratio at 4.2x, compared to EOG at 6.9x, COP at 5.2x, PXD at 4.8x, and HES at 11.8x. Profitability Source: Seeking Alpha CNQ is extremely profitable, with profit margins at 28.5%, notably higher than EOG at 25.7%, COP at 23.4%, and HES at 17.8%. PXD has a slightly higher profit margin at 28.7%. CNQ beats its peers with an operating margin of 40.9%, compared to EOG at 33.1%, COP at 35.0%, PXD at 40.7%, and HES at 35.4%. As we mentioned earlier, management focuses on generating free cash flow and maintaining a strong balance sheet. To that end, the company generates $14.1 billion in cash from its operations, compared to EOG at $10.8 billion, COP at $27.5 billion, PXD at $10.9 billion, and HES at $3.5 billion. Growth Source: Seeking Alpha CNQ’s revenues have risen 61.7% YoY. While that’s impressive, it’s not as strong as its peers. EOG grew revenues 73.4%, COP 109.0%, PXD 73.1%, and HES 65.3%. Moreover, CNQ has a notably lower forward revenue growth of 24.6% compared to its rivals. EOG is at 34.8%, COP at 51.1%, PXD at 51.9%, and HES at 35.7%. Our Opinion 8/10 CNQ has raised its dividend for 23 consecutive years. The company is in a strong financial position with a debt-to-EBITDA ratio of 0.5x, and debt is targeted to decline further. Its free-cash-flow allocation policy is unique and balanced, giving shareholders an excellent opportunity for significant returns. CNQ was one of the big winners in 2022, and we believe that will likely be the case again in 2023. The company is positioned for long-term success, and we’d buy at these levels. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |