|

Proprietary Data Insights Financial Pros Top Silver Stock Searches in the Last Month

|

|

Basic Materials |

Does This Silver Miner Deserve Its Spike in Search Volume? |

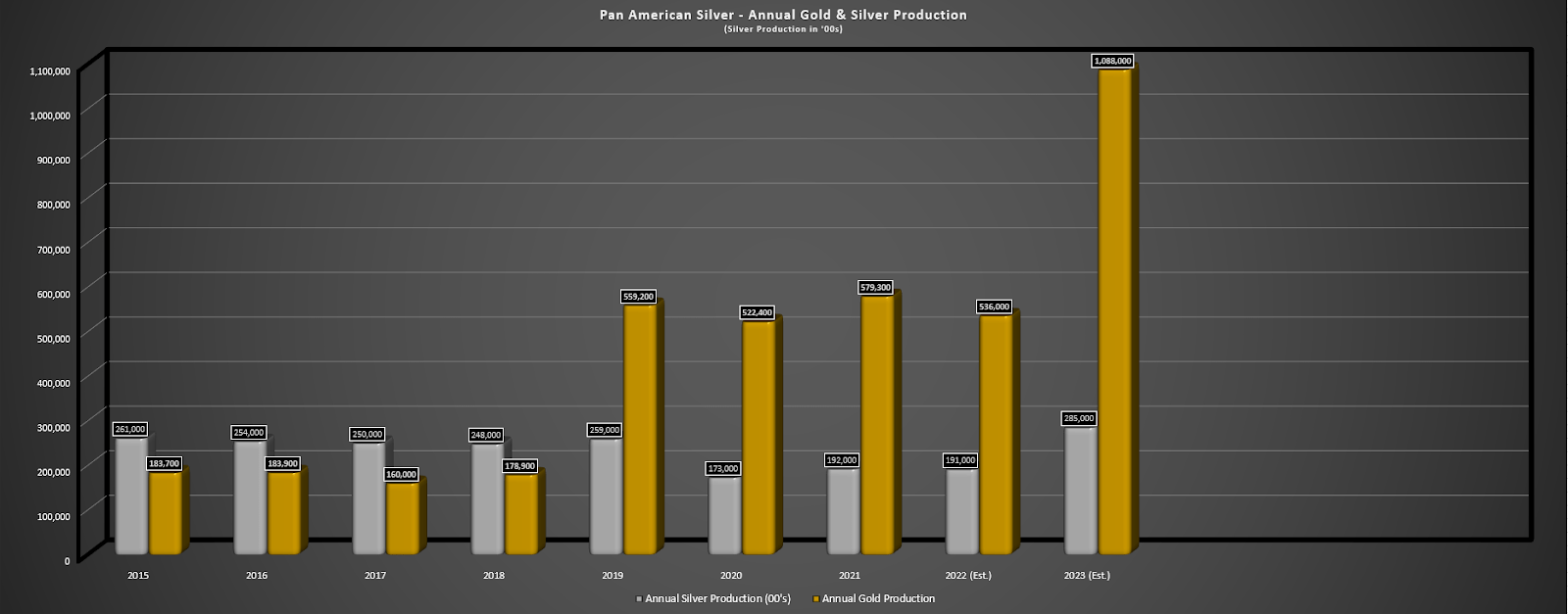

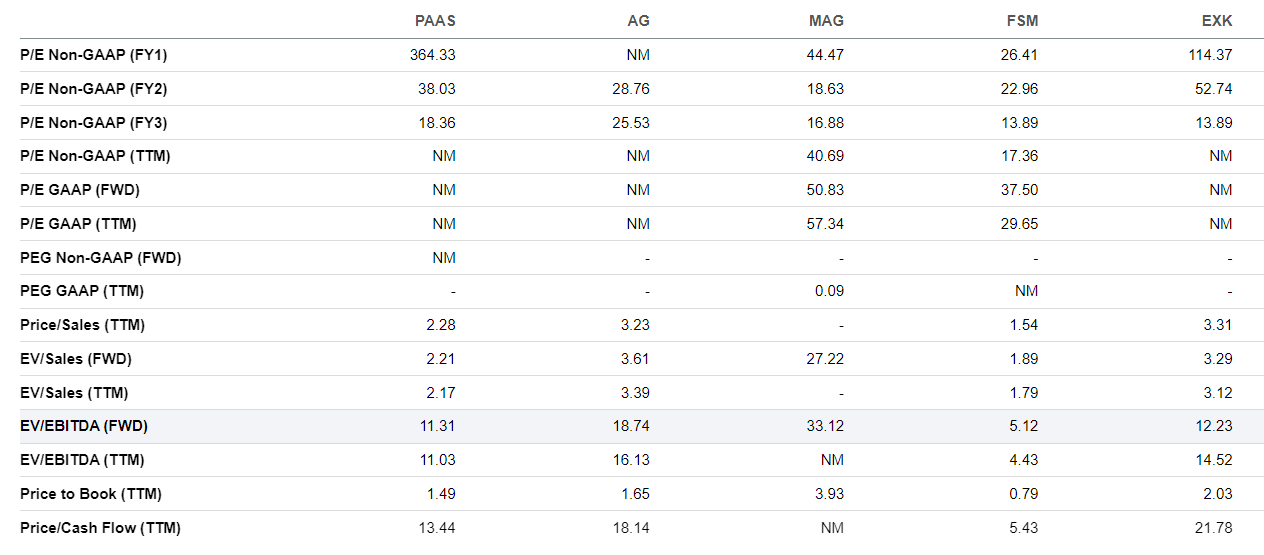

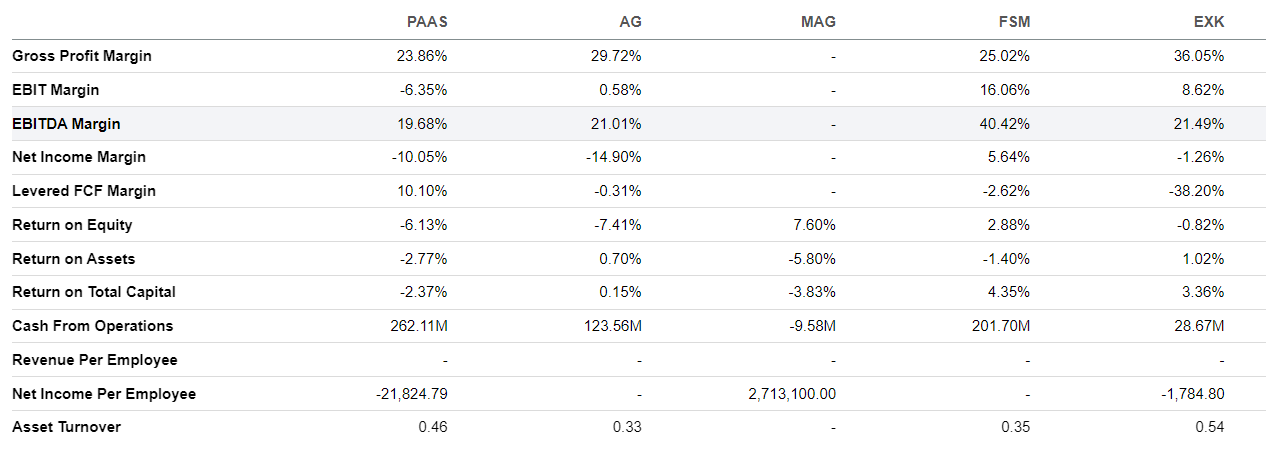

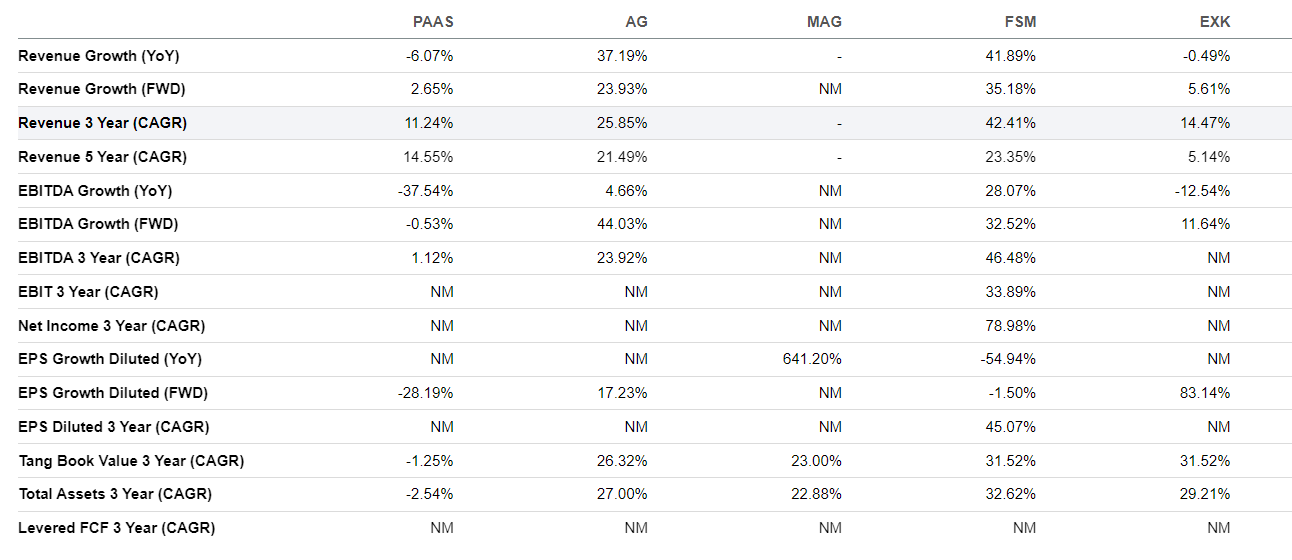

Pan American Silver (PAAS) was one of the worst-performing silver miners in 2022. But financial pros have searched for it the most out of silver mining stocks in the last month, according to our proprietary Trackstar database. And last week, searches briefly surged fivefold. In November, the company entered an agreement with Agnico Eagle Mines to acquire Yamana Gold. That led to a massive spike in search volume. And the move will significantly improve PAAS’ trading liquidity with a pro forma $5.6 billion market capitalization, increase its annual silver and gold production, and lower its overall cost structure. So we looked at PAAS to determine if it’s a viable investment this year. Pan American Silver’s Business Pan American Silver produces and sells silver, gold, zinc, lead, and copper through mines across the Americas. Estimates say its mineral reserves contain approximately 514.9 million ounces of silver and 3.6 million ounces of gold as of June 30, 2022. The company also owns interests in exploration projects, investments, and advanced-stage development properties. The Yamana Gold acquisition adds an operating mine in southern Argentina, a region where Pan American already operates. Pan American expects post-tax synergies of $400 million to $600 million over 10 years. The transaction would boost its silver production by approximately 50% and double its gold production by adding long-life, low-cost assets in Latin America. Source: Seeking Alpha Financials Source: Stock Analysis From 2018 to 2021, PAAS’ revenues rose from $784.5 million to $1.6 billion. But it took a step back to making $1.5 billion over the last 12 months. The company’s facing higher energy costs and inflationary pressures. But it maintains a strong financial position with cash and short-term investments of $187.2 million. In addition, it has an undrawn line of credit of $500 million as of the close of Q3 2022. PAAS has a debt-to-equity ratio of 3.7x and a current ratio of 2.1x. It pays a quarterly dividend of $0.10 per share, a yield of 2.4%. Valuation Source: Seeking Alpha Inflationary pressure and supply chain cost increases hurt Pan American’s business. The company wasn’t profitable in 2022. The same was true for rivals First Majestic Silver (AG) and Endeavour Silver (EXK). On the other hand, MAG Silver (MAG) and Fortuna Silver Mines (FSM) traded at P/E GAAP ratios of 57.3x and 29.6x. PAAS trades at a price-to-cash-flow ratio of 13.4x, stronger than AG at 18.1x and EXK at 21.7x, while FSM is at 5.4x and MAG at NM (not meaningful). Profitability Source: Seeking Alpha Higher input costs compressed gross margins, which led to PAAS running a profit margin of -10.1%. That’s not as bad as AG at -14.9%, but it’s notably weaker than FSM at 5.6% and EXK at -1.3%. On a brighter note, PAAS generates $261.1 million in cash from its operations, significantly more than AG at $123.6 million, MAG at -$9.6 million, FSM at $201.7 million, and EXK at $28.7 million. But its operating margin of -6.3% is disappointing compared to AG at 0.6%, FSM at 16.0%, and EXK at 8.6%. Management has struggled to make the pieces work. PAAS’ return on equity of -6.1% is weaker than MAG at 7.6%, FSM at 2.9%, and EXK at -0.8%, but better than AG at -7.4%. Growth Source: Seeking Alpha PAAS’ revenue declined 6.1% YoY, while some of its peers’ revenues have actually substantially improved. AG grew revenues 37.2% and FSM 41.9%. EXK had a slight decline of 0.5%. Pan American hopes its transformative acquisition of Yamana Gold will steer the company back in the right direction. If the transaction gets approved, it’ll increase PAAS’ net asset value and improve its margin profile. Our Opinion 5/10 Pan American Silver was one of the worst-performing silver miners in 2022. If the Yamana Gold deal goes through, PAAS may be an attractive buy in the future. But we’d wait to see instead of buying now. If the deal falls through, we’ll stay away. Management hasn’t done well operating the company, which shows in its stock performance.

|

|

News & Insights |

Just Spilled |

|

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |