|

Proprietary Data Insights Top Asset Management Stock Searches This Month

|

||||||||||||||||||

|

If You Found $20 on the Sidewalk… You’d look around and make sure somebody else didn’t obviously drop it. Once you determined it was truly found money, you’d grab it and maybe treat yourself or buy a fraction of a share of Tesla. Whatever your choice, you’d somehow – even if super casually – factor it into that day’s budget. Plus, you’d feel lucky. Not win-the-lottery lucky. But lucky nevertheless. This is a good way to view Social Security. All day, every day, we’re reading articles and research about money here at The Juice. And one thing we’re pretty sure of is retirement planning discussions don’t mention Social Security a lot. When they do, they often malign it. While we don’t think you should focus on Social Security ahead of retirement or, subsequently, rely on it in retirement, we do think future recipients of the entitlement do themselves a disservice if they don’t even consider it. There’s nothing wrong with banking on money you have coming to you after having paid Social Security taxes over decades of employment. Best-case scenario, your monthly Social Security check is gravy. You can blow it, invest it, or set it on fire. Next-best-case scenario, it helps supplement a comfortable retirement you primarily fund with ample savings and investments. Worst-case scenario, you not only rely on Social Security, but can’t make ends meet without it and some form of employment in old age. Next-worst-case scenario… We’ll cover that below. It comes from some research that surprised us and reignited our thinking on Social Security and retirement. As we go back to basics on personal finance and investing in Q1 of the new year, we detail this research and consider ways to factor Social Security into your post-60-year-old budget. |

|

Retirement |

Something Big We Overlook in Retirement Planning |

Key Takeaways:

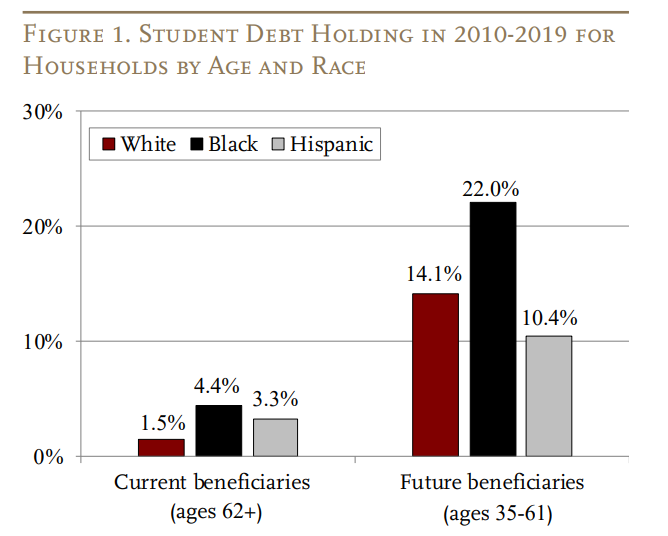

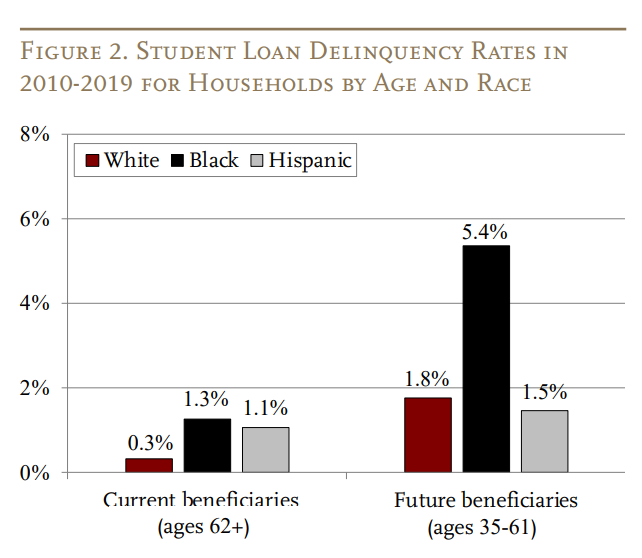

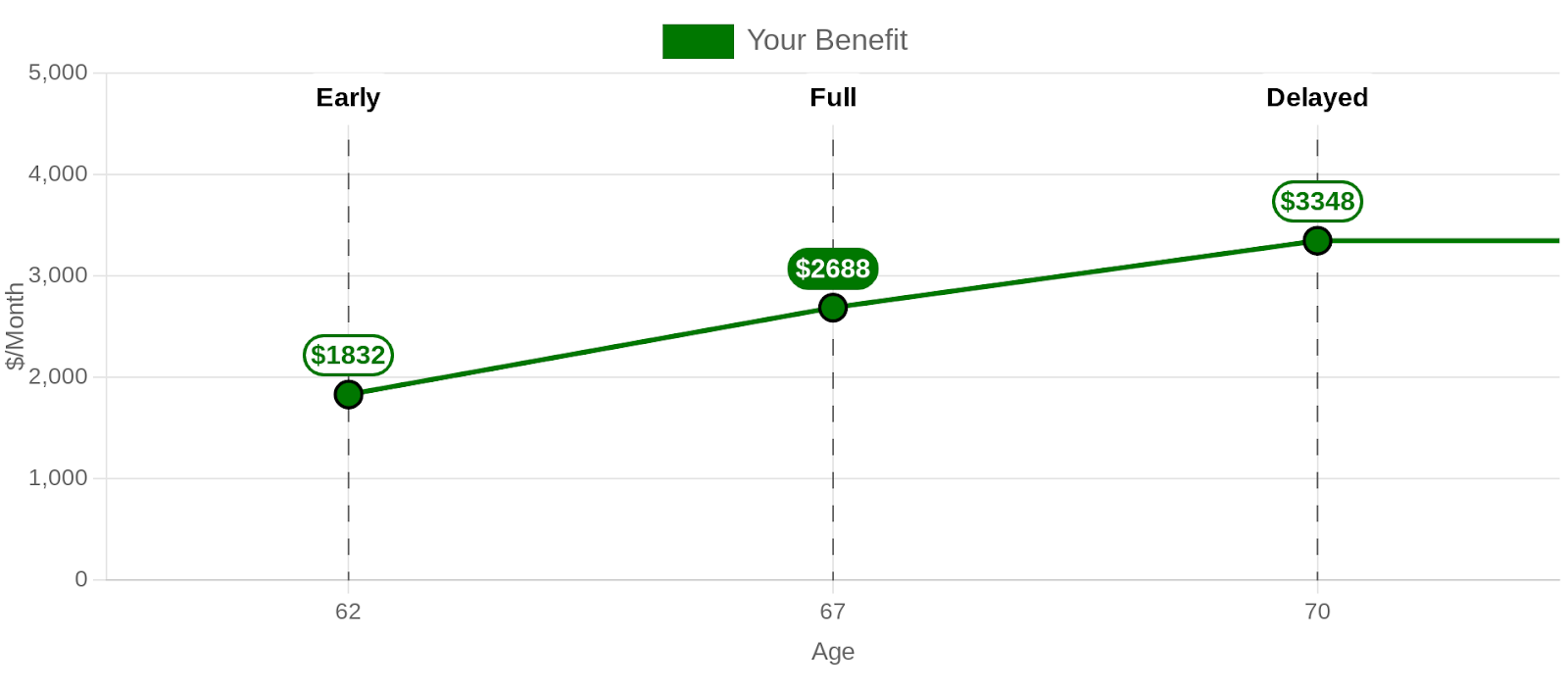

While it’s not a big problem now, recent research out of the Center for Retirement Research at Boston College says it could be: When you start collecting Social Security, the government can withhold part of your payment if you’re delinquent on federal student loans. Source: Center for Retirement Research at Boston College The chart above shows that future Social Security beneficiaries hold considerably more federal student loan debt than current beneficiaries. Not shocking, but still super important, because according to the research, delinquency rates will likely be much higher for future beneficiaires than current ones, particularly among Black households: Source: Center for Retirement Research at Boston College The data stops at 2019 because of the pause on student loan payment and collection the pandemic triggered. While President Biden’s forgiveness plan could provide some relief – if it ever sees the light of day – the average balances are higher than the anticipated relief. The average federal student loan balance for current beneficiaries (people 62 or older) is $30,600, compared to $35,300 for future beneficiaries (people between 35 and 61). First thing that took us by surprise: the amount of outstanding student loan debt among retirees. The second thing: We didn’t realize (or at least think about) the fact that the government can withhold 15% of your total monthly Social Security benefit or the amount by which the payout surpasses $750 – whichever is less – if you’re delinquent on your federal student loans. As the data shows, this could be a big problem for future beneficiaries, eating away at between 4% and 6% of household income. So pay your loans. Try to eliminate that debt before retirement. Even if this doesn’t apply to you, preach it to your kids, grandkids, siblings, and anyone who will listen. Because if they go delinquent on any of this outstanding debt, they’ll lose some Social Security income. And that’s a meaningful chunk of change. A willing mid-40s, upper-middle-class guinea pig here in The Juice’s office let us use their estimated Social Security benefits for illustration: Source: Social Security Administration The delinquent student debt angle aside, an extra $1,832 to $3,348 a month – depending on when this person starts collecting benefits – is nothing to sneeze at. Much more significant than finding $20 in front of the coffee shop. You can see your Social Security snapshot here. Run the numbers. Then, think about all the scenarios where that amount of money – every month – could come in more than handy in retirement. Even if your saving and investing over the years will more than fund a sweet retirement, an extra couple thousand or so could be fun money. If you plan to make investing your hobby in retirement, Social Security could give you firepower to put into the market. Or you could use Social Security to satisfy one or more of the expenses you worry about having in retirement. Maybe you’re on the fence about taking on a new mortgage in your 40s or 50s. Maybe you’re worried about the cost of healthcare in your 60s and beyond. All reasonable, real-life considerations that benefit from ample savings and a healthy investment portfolio. This supplement hitting your bank account every month makes things even better. The Bottom Line: There’s a good chance you help fund Social Security with your current income. Or you helped when you were working. Come retirement – or the age at which you decide to collect – you’re entitled to your share of Social Security. Social Security is an entitlement program. Not just 75-year-old Walmart greeters struggling to get by can benefit from Social Security. Even if you’ve already reached your target nest egg number for retirement through saving and investing, factor in the icing on the cake. It can help turn an already solid retirement plan and eventual lifestyle into an even better, more carefree one. |

|

News & Insights |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |