|

Proprietary Data Insights Financial Pros Top Discount Stores Stock Searches in the Last Month

|

|

Consumer Defensive |

This Discounter Is Making the Right Moves |

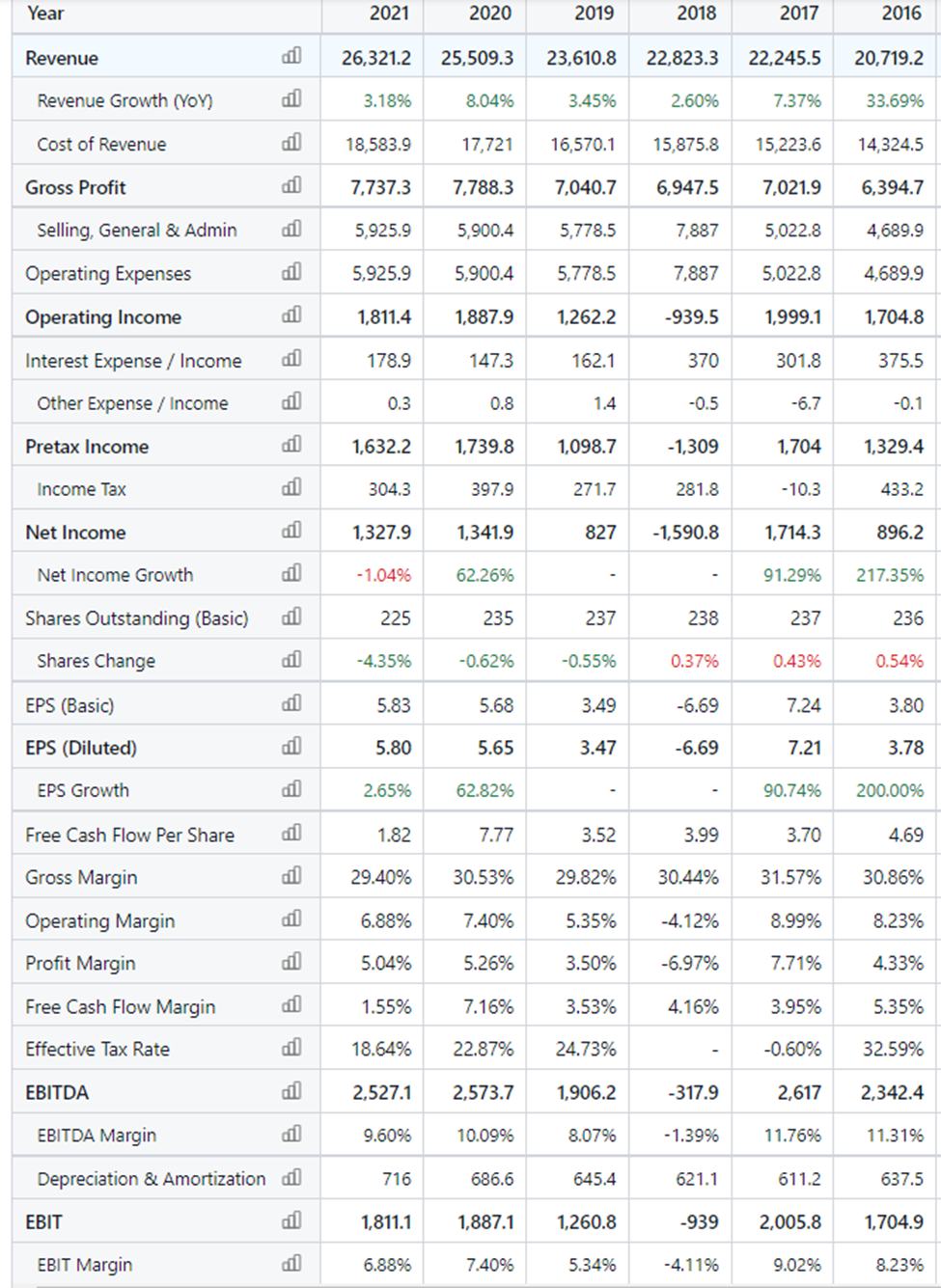

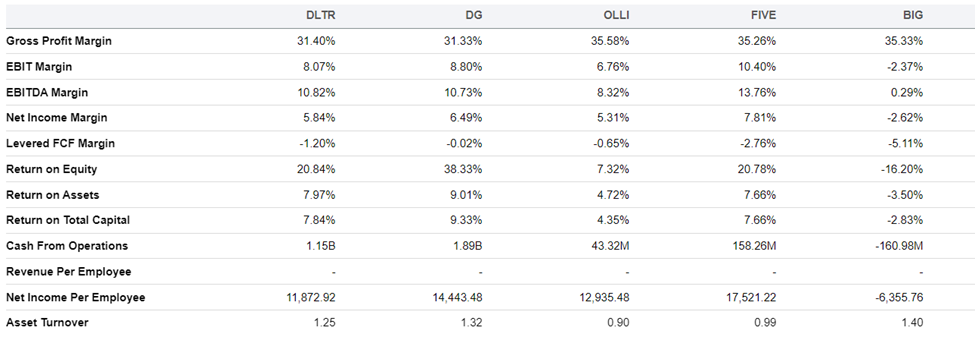

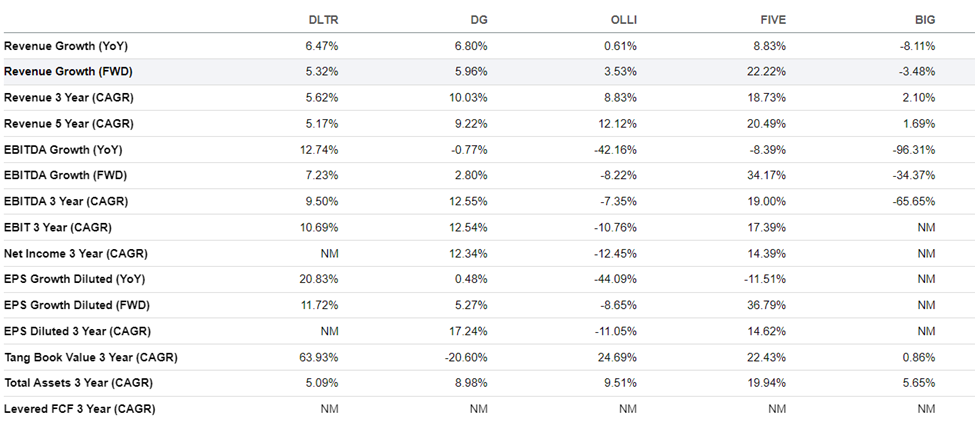

As food-price inflation hit a record high of 13.3% during Christmas, shoppers turned to discount stores to meet their needs. Our proprietary Trackstar database picked up on a recent surge in searches for discount stores by both financial pros and retail investors. This comes after fairly lackluster interest through most of December. Second on that list of discount-store searches was Dollar Tree (DLTR). Among its peers, it’s the best overall value. The company is focused on driving traffic to its consumables business, and it’s paying off. Financial pros have recognized that for two consecutive quarters, consumables comps (quarter-over-quarter change) have outpaced discretionary comps at Dollar Tree. Despite a challenging year, Dollar Tree produced its highest company revenue in 2022. Can it continue its momentum? And more importantly, is it a company investors should add to their portfolios? Dollar Tree’s Business Dollar Tree is a leading operator of discount variety stores. It operates under the brands Dollar Tree and Family Dollar. It transitioned from selling its lowest-priced items for $1.00 to selling them for $1.25, enabling merchants to enhance value significantly for their shoppers. The company has more than 16,200 stores across 48 states and five Canadian provinces. In addition, DLTR has put a greater emphasis on consumable products. As we said, for two consecutive quarters, consumable comps have outpaced discretionary comps at Dollar Tree. The leaders have been food and beverage, snacks, cookies, and candy. Discretionary items include nonperishables such as clothing, home goods, and toys. Dollar Tree also expanded its $3 and $5 offerings into more stores. DLTR believes it’s in its best pricing position in over a decade. To further strengthen margins, the company has focused on developing its private brands, which can further enhance brand loyalty. Source: Dollar Tree Family Dollar delivered its strongest quarterly same-store sales increase since 2020 and grew store traffic comparable to Dollar Tree stores’ growth for the first time in 12 quarters, according to the company’s Q3 2022 report. Financials Source: Stock Analysis DLTR has a debt-to-equity ratio of 1.25x, its lowest multiple since 2018. Meanwhile, the firm’s revenues rose from $22.8 billion in 2018 to $27.7 billion in 2022. In Q3 2022, the company repurchased 2.86 million shares at an average price of $139.04, which cut its cash from $701 million to $439 million. Despite inflationary pressure and higher costs from suppliers, mainly in China, the company improved margins with the price bumps on its lowest-cost items. It generated $1.1 billion in cash from operations in the last year and is financially stable with a current ratio of 1.3x. Valuation Source: Seeking Alpha DLTR trades at a P/E GAAP ratio of 19.7x, relatively cheaper than its peers Dollar General (DG) at 23.9x, Ollie’s Bargain Outlet Holdings (OLLI) at 31.1x, Five Below (FIVE) at 42.8x, and Big Lots (BIG) at NM (not meaningful). DLTR’s ratio looks high now, but its five-year average is around 19.0x. And that’s not all. Dollar Tree’s price-to-sales ratio of 1.1x is lower than that of its competitors. DG is at 1.5x, OLLI is at 1.6x, and FIVE is at 3.3x. BIG is lower at 0.08x, but BIG isn’t profitable like DLTR. Furthermore, DLTR has a lower price-to-cash-flow ratio than its peers at 27.2x. DG’s is 29.1x, OLLI’s is 67.2x, FIVE’s is 62.0x, and BIG’s is NM (not meaningful). Profitability Source: Seeking Alpha DLTR has a profit margin of 5.8%, lagging DG at 6.5% and FIVE at 7.8%, but better than BIG at -2.6% and OLLI at 5.3%. Management plans to improve margins by offering higher-priced items at Family Dollar, offering more consumables at Dollar Tree, and developing private brands. Its operating margin of 8.0% is not far from its largest competitor, DG, at 8.8%. It’s notably higher than OLLI at 6.7% and BIG at -2.3%, but it lags FIVE at 10.4%. Dollar Tree’s management is fairly effective, with a return on equity of 20.8%. Only DG is higher at 38.3%. The company’s return on assets is nearly 8.0%, which only DG beats at 9.0%. Growth Source: Seeking Alpha Most discount stores grew revenues modestly over the last year, with FIVE leading the pack at 8.83%. Meanwhile, DLTR grew revenues 6.4%, DG 6.8%, OLLI 0.6%, and BIG -8.1%. DLTR is focused on driving sales per square foot, unit sales growth, and transaction growth under a new management team. The company has adjusted prices and enhanced its advertising and marketing, which it believes can lead to further growth. Our Opinion 7/10 Consumer behavior is shifting to focus on needs as the economy weakens. DLTR has recognized this and is offering consumables and products catered to the shift. While it’s smaller than DG, it’s relatively cheaper than its peers from a valuation standpoint. Yet its P/E ratio compared to its historical average says it’s fairly valued. We believe DLTR can do well in the current environment and deliver positive returns to investors in 2023 and beyond. Shares are $145.88 at writing. They generally look good at $140 and below. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |