|

Proprietary Data Insights Financial Pros Top Gold Miner Searches in the Last Month

|

|

Basic Materials |

A Better Way to Play Gold |

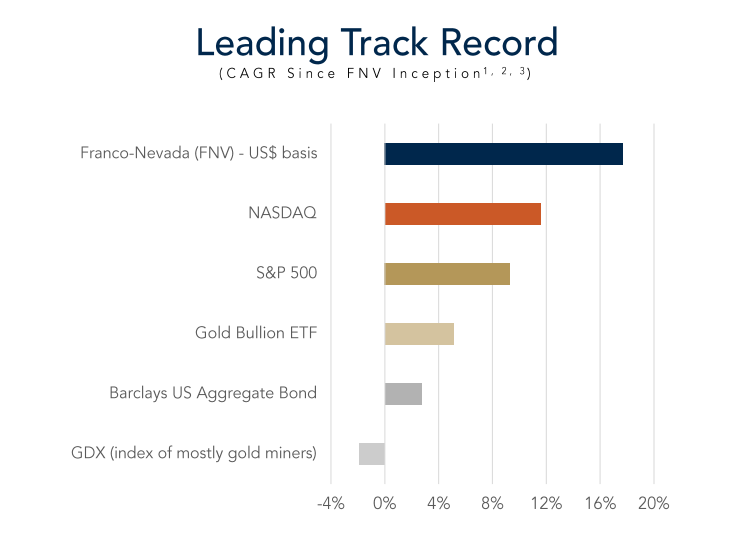

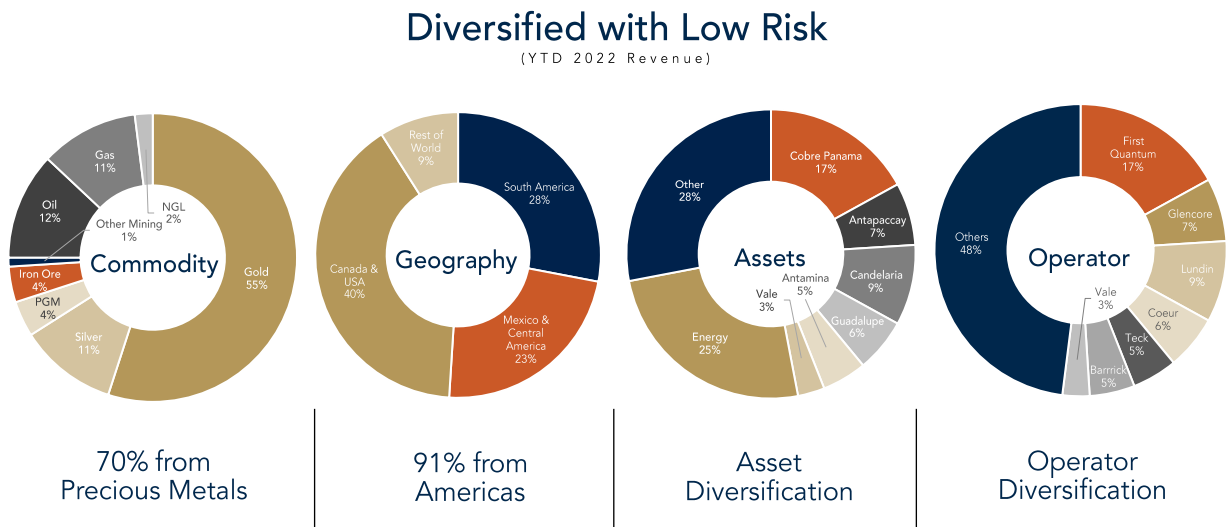

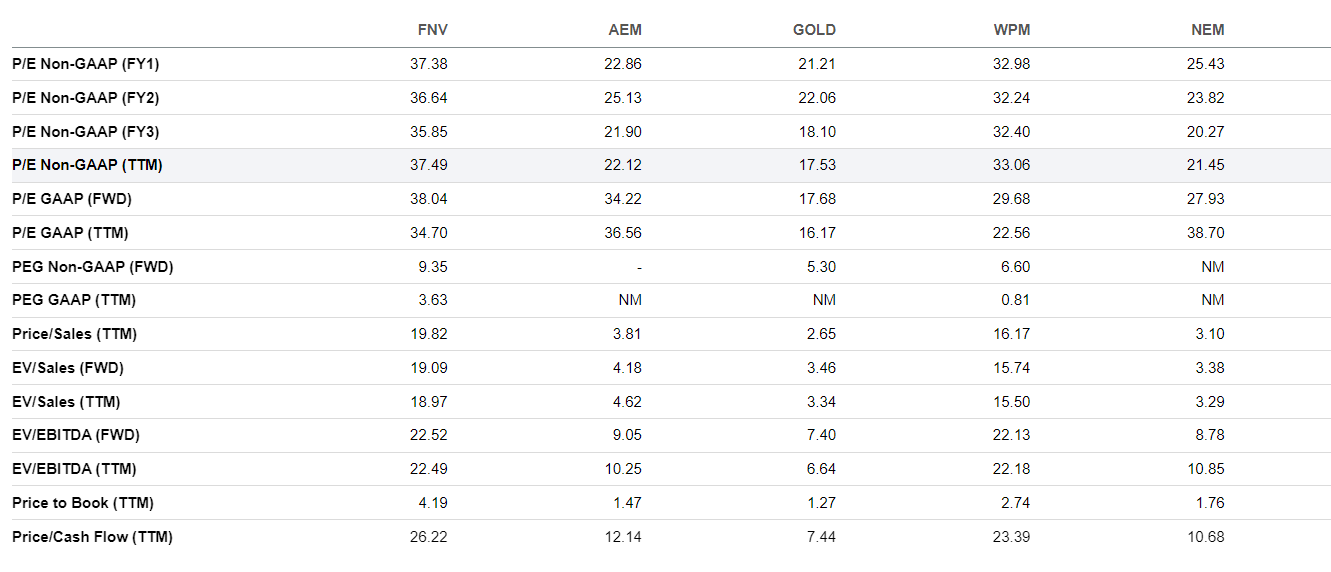

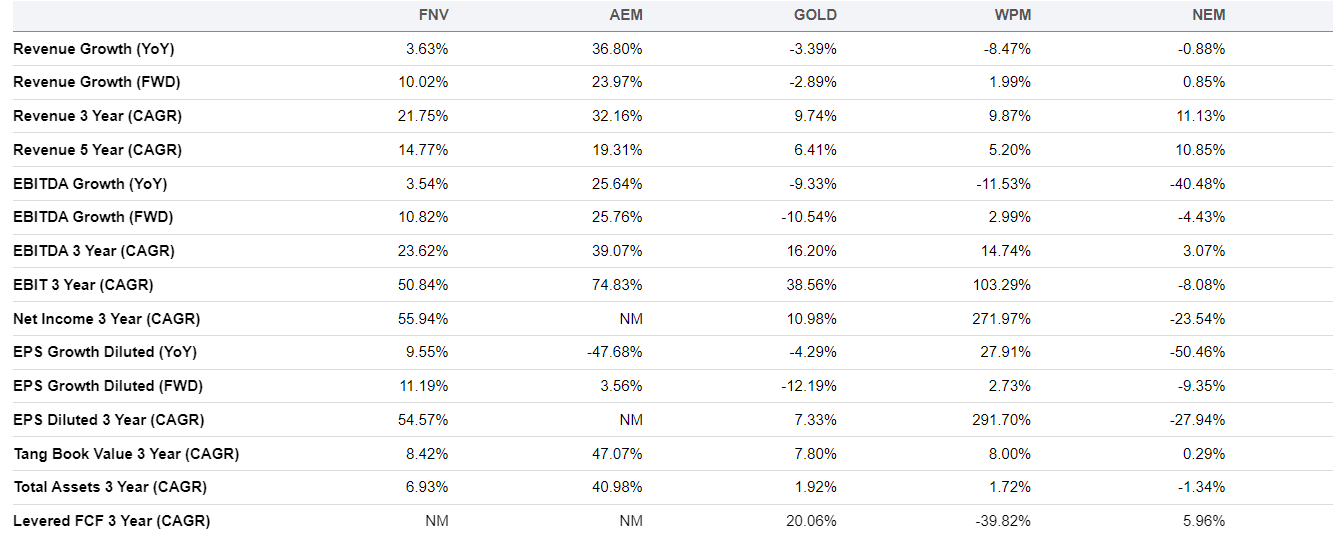

Inflation hit a multi-decade high in June 2022, spiking nearly 9% from the prior year. Although it’s receded some, investors are still looking for assets that can hedge against it. At least that’s what we assume, given the data we uncovered in Trackstar, our proprietary sentiment indicator. According to Trackstar, there’s been an unusual spike in searches for gold stocks, especially those surrounding Pan American Silver (PAAS) and Agnico Eagle Mines (AEM)’s proposed acquisition of Yamana (AUY). Yet when we looked at the top five gold miners, #5 Franco-Nevada (FNV) is the one that stood out. Unlike gold, FNV pays its investors a dividend. The company has a mountain of cash and no debt. In fact, since its inception, it has outperformed the Nasdaq, S&P 500, and SPDR Gold Trust gold bullion ETF (GLD). Source: Franco-Nevada Financial pros like the company’s free-cash-flow business and diversified portfolio. Its high margins and low overhead make it appealing, particularly in this environment. At first glance, FNV seems expensive relative to its peers. But we found some interesting reasons you should consider this gold miner. Franco-Nevada’s Business Franco-Nevada has the largest and most diversified portfolio of cash-flow-producing assets of all the miners in our Trackstar top five. Its mineral assets include 112 producing assets, 42 in the advanced stage, and 250 in the exploration stage. In 2022, 70% of its revenues came from precious metals. 55% of its revenues were from gold. FNV generates revenues from royalties and streaming. It collects a fixed percentage of revenue each mine generates, plus it gets physical metals. Streaming means providing financial support to other miners in exchange for a percentage of the gold they produce. FNV is focused on growth, with free cash flow a top priority. Its long reserve and resource lives distinguish it from many other gold operating companies. Source: Franco-Nevada Income investors will be excited to hear FNV has increased its dividend for 15 consecutive years. Financials Source: Stock Analysis Franco-Nevada has $999.2 million in operating cash flow. It repays its investors with an annual dividend of $1.75 a share, a yield of 1.28%. The company’s price-to-free-cash-flow ratio of 26.2x is its lowest in over eight years. Moreover, its current ratio of 24.3x is its highest since 2017. One of the reasons for its long-term success has been the company’s ability to limit cost inflation. Streams are not exposed to cost inflation based on how the company structures its agreements. FNV isn’t exposed to capital calls on debt because it’s a free-cash-flow business, meaning it uses its cash flow to fund its streaming agreements. Valuation Source: Seeking Alpha FNV trades at a P/E GAAP ratio of 34.7x, making it relatively cheaper than its peers AEM at 36.6x and Newmont (NEM) at 38.7x. But Barrick Gold (GOLD) at 16.2x and Wheaton Precious Metals (WPM) at 22.6x have more competitive valuations. Franco-Nevada’s price-to-cash-flow ratio of 26.2x is rich compared to AEM at 12.1x, GOLD at 7.4x, WPM at 23.4x, and NEM at 10.7x. The same goes for Franco Nevada’s price-to-sales ratio of 19.8x. Its competitors trade at notably smaller multiples. AEM is at 3.8x, GOLD at 2.7x, WPM at 16.2x, and NEM at 3.1x. Profitability Source: Seeking Alpha While some investors may be concerned with Franco-Nevada’s valuation, they can’t complain about the company’s profitability, as it’s head and shoulders above its peers. Its net income margin of 57.3% is considerably higher than AEM at 10.4%, GOLD at 16.4%, and NEM at 8.3%. Only WPM is higher at 71.8%. But none of these competitors can match FNV’s EBITDA margin of 84.4%. AEM is at 45.0%, GOLD is at 50.3%, WPM is at 69.9%, and NEM is at 30.3%. Franco-Nevada’s management is highly effective, as its return on assets of 11.8% and return on equity of 12.5% show. Its closest peer is WPM, with a return on assets of 10.7% and a return on equity of 12.7%. None of the others come close to posting double digits in these categories. FNV can maintain high margins and low overhead. Growth Source: Seeking Alpha FNV grew modestly over the last year, with revenues up 3.6%. While that doesn’t sound like much, many of its peers had negative revenue growth. GOLD was at -3.4%, WPM at -8.5%, and NEM at -0.9%. AEM was the only one that grew revenues by double digits at 36.8%. But the key considerations here are the three- and five-year average growth rates. FNV holds the second-highest spot in revenue, EBITDA, and EPS average growth over these periods. And since its inception, FNV has had a greater compound annual growth rate than the Nasdaq, S&P 500, and GLD. Our Opinion 8/10 FNV offers investors an alternative to buying physical metals and ETFs. The company’s track record over the years is outstanding. Management has shown it can work through hard times, and we have no reason to believe it can’t continue posting strong results while rewarding shareholders. We like the stock long-term and believe it’s a worthwhile addition for anyone’s portfolio. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |