|

Proprietary Data Insights Top Residential Construction Stock Searches This Month

|

||||||||||||||||||

|

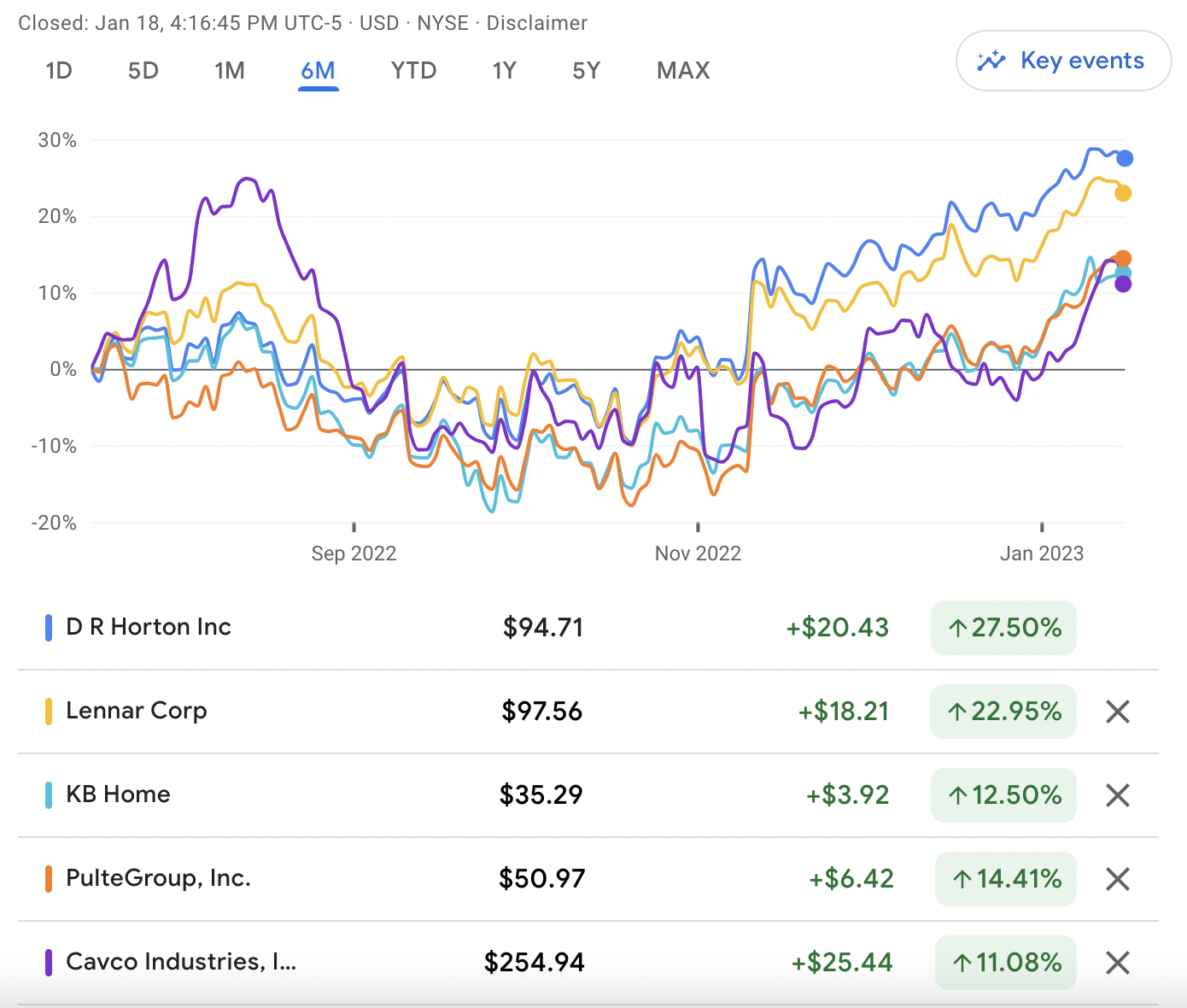

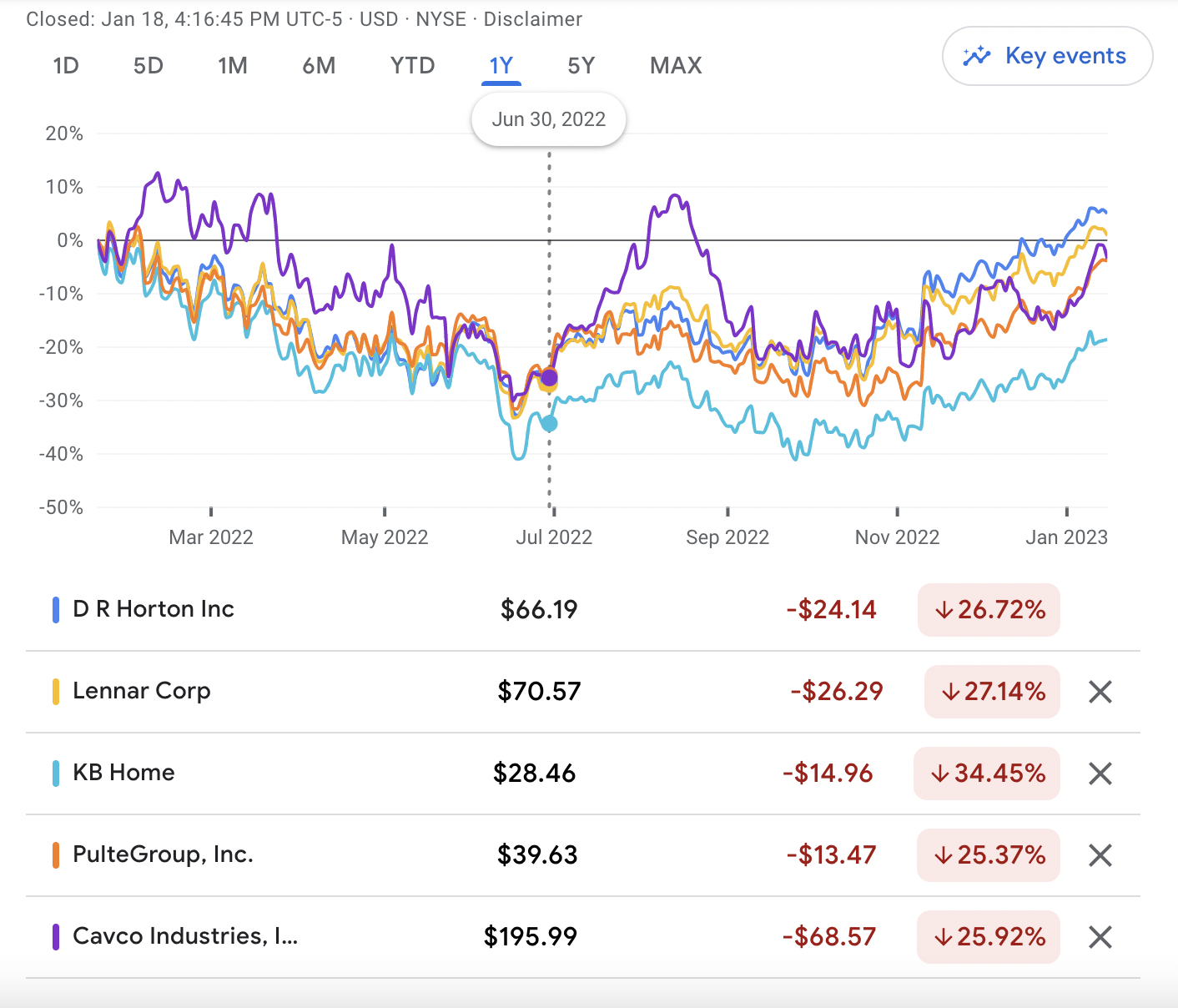

The Worst Should Be Behind Homebuyers Source: Google Finance Homebuilder stocks have crushed it over the last six months. We think it’s a textbook example of the forward-looking stock market. The idea that investors often value companies based on what we anticipate will happen. That means future bad news is often already priced into stocks. As homebuilders report earnings this month, we’re certain to see mixed results. For example, Lennar (LEN) already reported. It beat analyst expectations on earnings per share, but missed on revenue. The news wasn’t as good at KB Home (KBH). The company missed on sales and profits and offered tepid guidance for the first quarter of 2023 as it focuses on price cuts in an effort to boost demand. These results represent moments in time, particularly in the purview of long-term investors. Maybe not all the bad news, but the worst news is likely behind the housing market. This view might be one reason homebuilder stocks have surged in the second half of 2022 and the start of 2023 after tougher times during the first half of last year: Source: Google Finance As we expand on below, any home-price cuts will certainly increase demand, helping fuel meaningful but still relatively modest declines in the broad housing market. But these drops won’t last long… If we’re right, there’s a window of opportunity for prospective homeowners on the strongest financial footing. For the rest of the people still chasing the runaway American dream (name the song!), housing still isn’t affordable and might not be for the foreseeable future.

|

|

Housing |

A Housing Cooldown Doesn’t Mean Affordable Housing |

Key Takeaways:

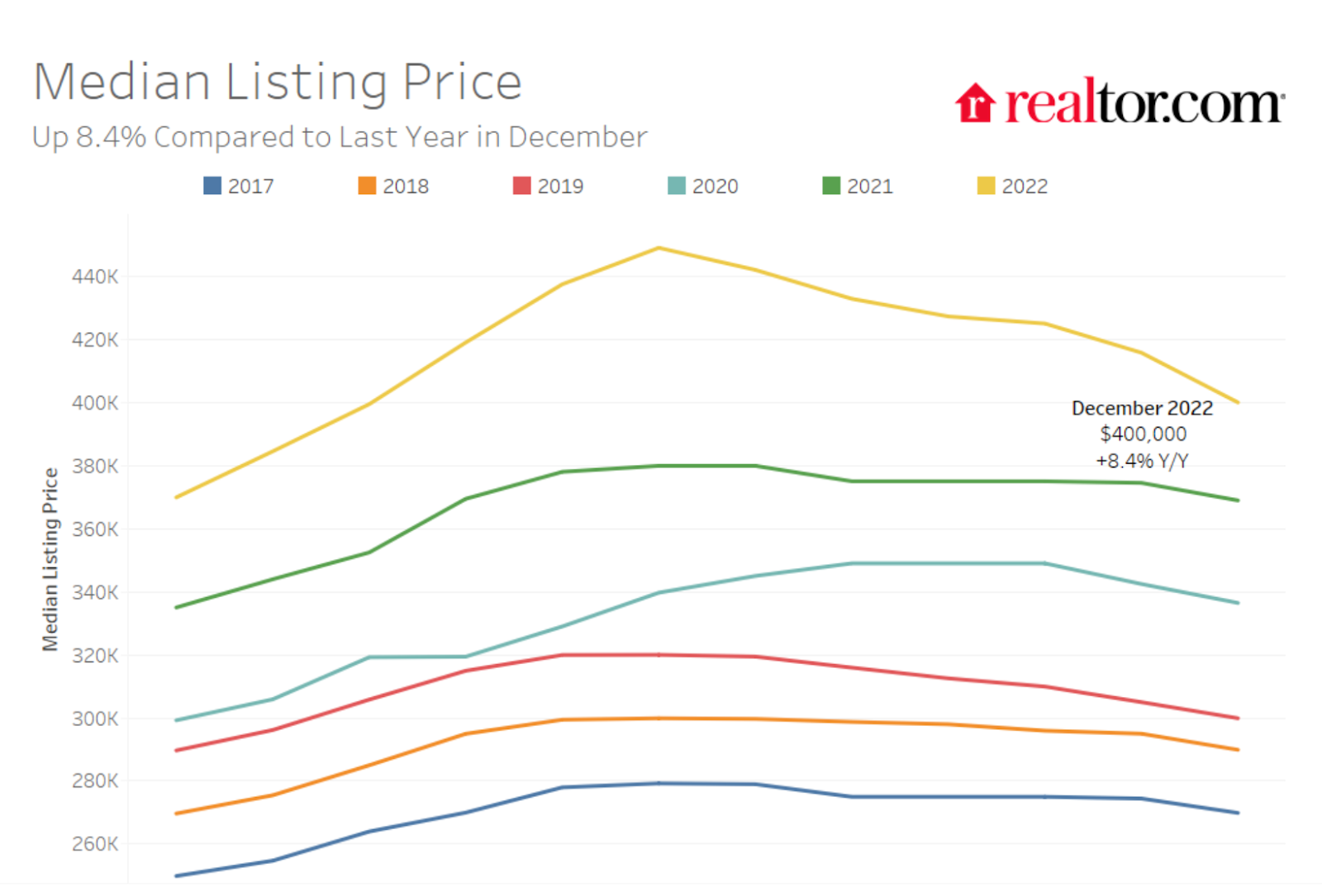

Source: Realtor.com The two main takeaways from the above December 2022 Realtor.com data on median housing prices:

So when you hear that, for the first time in 12 months, housing prices didn’t rise by double digits, it might not be time to get super excited. Because here’s what The Juice thinks is going down… The worst time to buy a home in 2022 was when the interest rate on a 30-year mortgage surpassed 7% at the same time housing prices hovered at or near record highs. Like in fall 2022, when the rate hit 7.3% and the median home price nationally was around $425,000. After a hefty 10% down payment of $42,500, your $382,500 30-year loan generated a monthly payment of $2,622 before we even factor in fees, insurance, property tax, and maintenance. In January 2023, the rate has cooled to around 6%. Prices have cooled to a median of about $400,000. If you’re able to come up with the now $40,000 down payment, you’ll pay $2,158 each month for the typical house before the aforementioned additional expenses. Significant savings of $464 a month, yes. But consider a few more factors. We’re talking the national median here. Across the country, in cities big (San Francisco, Los Angeles, New York) and medium (Austin, Portland, Denver), median list prices are still in the mid-to-high six figures:

Even though prices are moderating in these markets – as they are nationally – they’re still freaking expensive. Even if you can snag something below asking, it’s still freaking expensive. The relatively modest drop will bring some once priced-out people off the sidelines. But only the most job-secure and financially confident. They’ll look at lower rates, lower prices, and the subsequent lower monthly payments and pounce, biding their time until (they assume) they can refinance in 2024 or 2025 at much lower interest rates. This will, at the very least, construct a solid floor for housing prices (as in, they won’t crash), if not put them back on an upward trend. They’ll likely start to go back up by 2024, if not at some point in mid-to-late 2023. Another case of the super well-off and well-positioned doing super well in our dichotomous economy of haves and have-nots. The have-nots will worry about persistent inflation. They’ll worry about losing their jobs. They’ll worry and wonder if interest rates will really come down and, if so, how much. Even with monthly payments several hundred dollars lower than they were six months before, they’ll still wonder if they’re biting off more than they can chew. They’ll remain on the sidelines. They’ll remain priced out of a cooling, but still pretty damn expensive, housing market. The Bottom Line: Uncertainty still reigns across the economy in 2023. But we feel good about our assessment of the housing market. There’s a reason homebuilder stocks are performing well: The housing market’s worst days might be behind it. And they weren’t even all that bad. While things might get a little worse, we think more housing-market upside will happen sooner than many doomsdayers predict. Whether or not you think this is good news depends on your perspective. If you’ve been priced out of the housing market over the last year or two, there’s a good chance you’ll remain priced out, unless of course you sat on the sidelines in optimal financial condition and you stay there not only today, but throughout 2023 and beyond. |

|

News & Insights |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |