|

Proprietary Data Insights Financial Pros Real Estate Services Stock Searches in the Last Month

|

|

Real Estate |

|

Real Estate Looks Ugly |

|

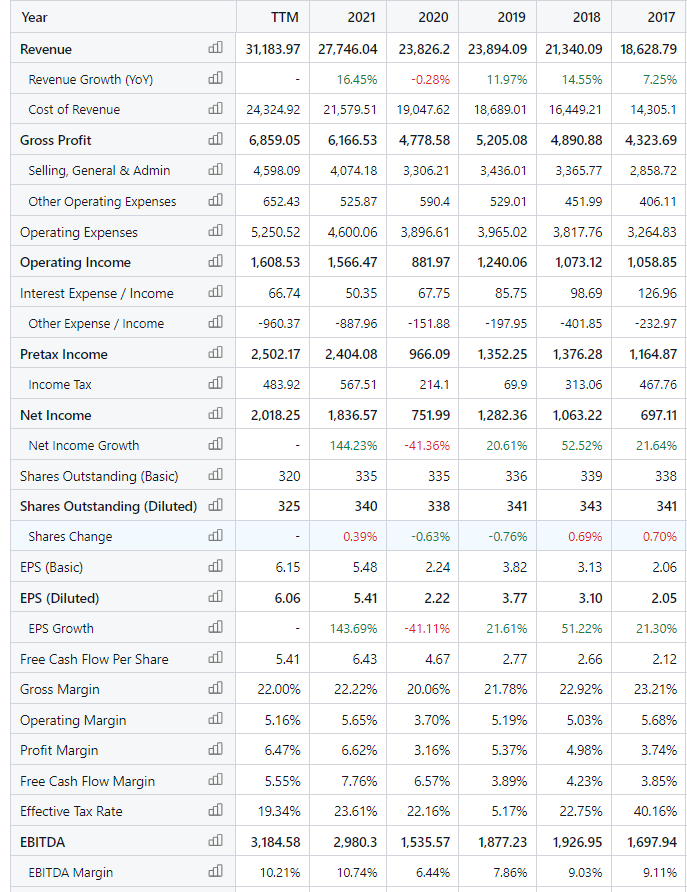

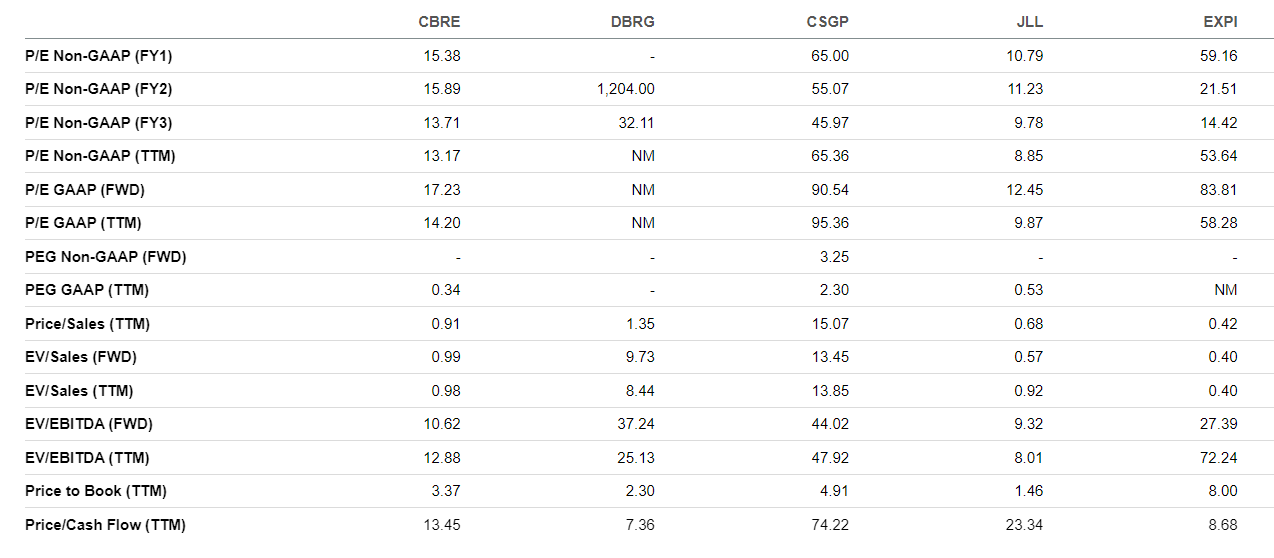

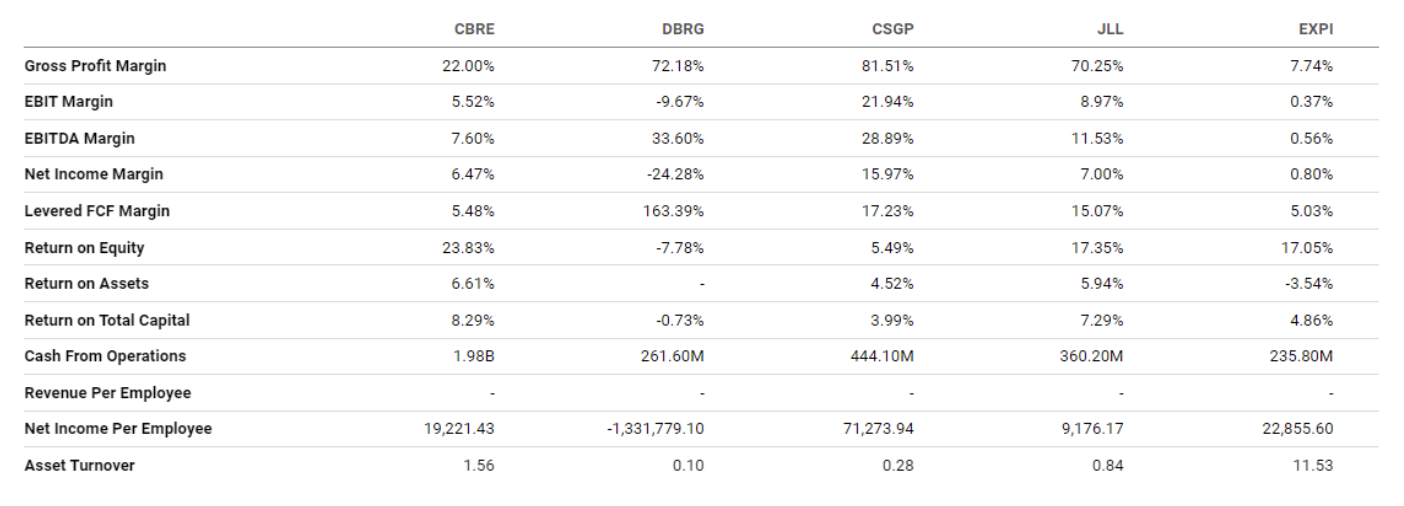

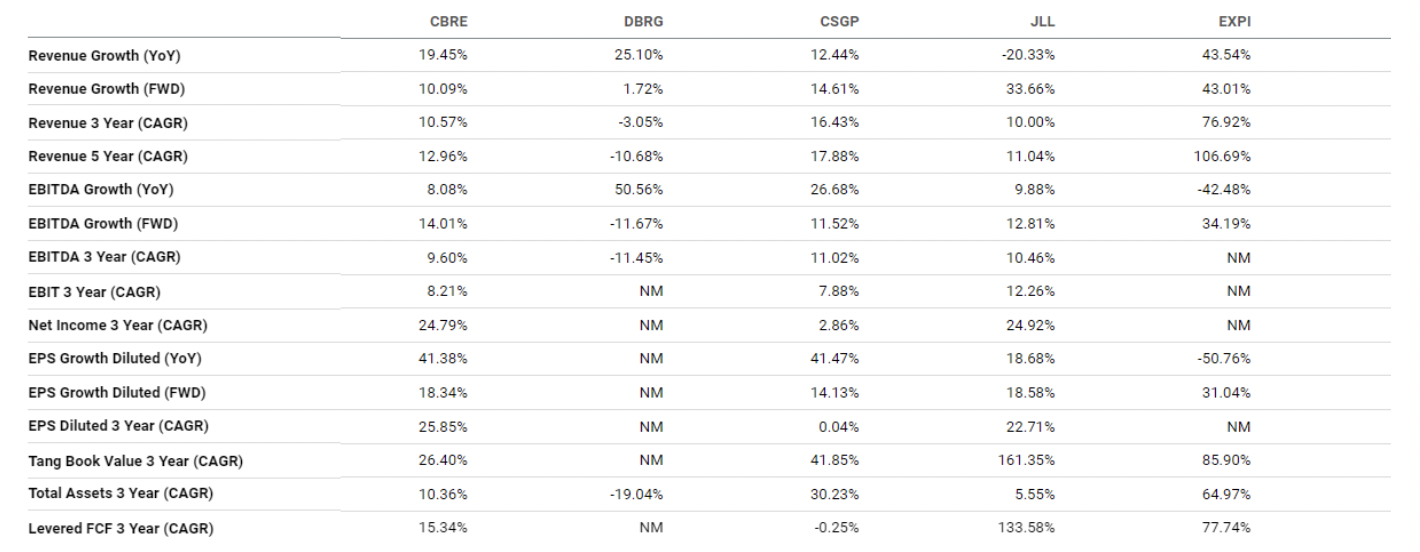

Experts expect commercial real estate deal activity to shrink 15% from last year, according to CBRE Group (CBRE). Rising interest rates, a looming recession, and less available credit all threaten real estate. Many believe related stocks will perform poorly. But that hasn’t stopped investors from showing interest in them, according to the latest search data from our proprietary Trackstar sentiment indicator. Financial pros are specifically eyeing CBRE, the largest commercial property developer in the country. Perhaps they’re confident the company’s robust financial position will allow it to withstand challenges. After all, the company gained valuable insights from previous real estate market downturns, emerging stronger than ever. And shares are up 13.7% over the last three months. CBRE isn’t financial pros’ most widely searched commercial real estate company on our list. But there’s good reason for you to consider this steady Eddie. CBRE Group’s Business To be clear, CBRE isn’t a real estate investment trust (REIT). It’s one of the world’s largest publicly traded commercial real estate services and investment companies. It offers property sales, leasing, facilities management, valuation, and advisory services. The company operates in more than 100 countries, runs 500 offices, and employs over 105,000 people. It manages nearly $144 billion of assets. CBRE divides its business into the following segments: advisory services, Global Workplace Solutions, and real estate investments. Its real estate investments business has taken a huge hit, as development operating profit fell from $100 million in Q3 2021 to $17 million in Q3 2022. The firm said this was due to expected deal timing, as it paused selling certain development assets because of weaker capital markets. In addition, investment management operating profit, a subset of the category, dropped 12% due to lower co-investment gains. The deterioration in the macro environment led to less capital available for transactions. However, Global Workplace Solutions net revenue rose 8% YoY in Q3 2022. The service offers a range of solutions that help businesses manage their real estate and facilities needs, including property management, project management, engineering, and transaction management. The advisory services business’ revenues rose 1% from the prior year’s quarter. The firm blamed weaker capital markets for the lack of growth. This business offers strategic consulting, research and analysis, valuation and appraisal, portfolio optimization, project management, and occupier services. Shares of CBRE hit a low of $29.17 in March 2020 and rose to as high as $111 in January 2022. Financials Source: Stock Analysis CBRE did phenomenal during the pandemic. The firm’s revenues only modestly dropped in 2020 and recovered swiftly in 2021. In fact, 2022 was its highest revenue year ever. But the company now faces new challenges, including higher interest rates, corporate layoffs, a correction in the real estate market, and companies downsizing office space. As it did during the pandemic, CBRE is prepared to reduce expenses and headcount to face upcoming challenges. The firm has plenty of cash, $1.1 billion, according to its Q3 2022 earnings report. Moreover, it has a current ratio of 1.1x, indicating it has plenty of capital to handle its near-term liabilities. Its debt-to-equity ratio of 0.5x is lower than it was a decade ago, and its operating cash flow over the last 12 months is close to $2 billion. Valuation Source: Seeking Alpha CBRE’s P/E GAAP ratio of 14.2x is its lowest since 2018. Relative to its peers, it trades at an attractive multiple. For example, CoStar Group (CSGP) trades at a P/E GAAP of 95.4x, eXp World Holdings (EXPI) at 58.3x, and DigitalBridge Group (DBRG) at NM (not meaningful). Only Jones Lang LaSalle (JLL) is cheaper at 9.9x. At a price-to-cash-flow ratio of 13.7x, CBRE is in the middle of the pack. DBRG is at 7.3x, CSGP at 74.2x, JLL at 23.3x, and EXPI at 8.6x. CBRE expects to invest more aggressively, utilizing free cash flow and its balance sheet during periods of market weakness. Profitability Source: Seeking Alpha CBRE believes it can reduce upwards of $400 million in spending before it impacts its ability to turn a profit. Its net income margin of 6.5% is middle-of-the-road compared to DBRG at -24.3%, CSGP at 16.0%, JLL at 11.5%, and EXPI at 0.6%. But none of them generate the amount of cash CBRE does at $2.0 billion. CSGP is its closest rival at $441 million, while DBRG is at $261.6 million, JLL at $360.2 million, and EXPI at $235.8 million. In addition, CBRE has the highest return on equity of the group at 23.8%. DBRG is at -7.8%, CSGP at 5.5%, JLL at 17.4%, and EXPI at 17.1%. This is a key metric for asset-heavy businesses. Growth Source: Seeking Alpha CBRE revenue grew a strong 19.5% YoY, though it wasn’t the highest among the group. DBRG and EXPI outperformed with 25.1% and 43.5% revenue growth, respectively. But it’s worth noting that CBRE has a significantly higher market cap, 12x that of DBRG and EXPI. Meanwhile, CSGP, the largest company in the group, had revenue growth of 12.4%. Moreover, CBRE’s EPS diluted compound annual growth rate over the last three years is the best of its peers at 25.9%. Meanwhile, DBRG is at NM, CSGP at 0.04%, JLL at 22.7%, and EXPI at NM. Our Opinion 7/10 Experts expect commercial real estate deal activity to shrink by 15% this year. But we could argue that the real estate market has seen darker days than the present and has recovered. CBRE has proven it can deliver over the years. Its stock price has risen 78.1% over the last five years. Shares currently trade above $82. Now might not be the right time to buy CBRE, after the stock has risen by 13.7% over the last three months. But there could be an opportunity in the second half of the year to get in at a more attractive entry level of $75 or less. If you can buy on weakness and hold for the future, it should pay off. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |