Editor’s Note: |

It’s Friday. Time to give you a stock pick from our sister newsletter, The Spill, so you can think about it over the weekend and maybe make a move Monday morning. While The Juice helps you be better with money across the board, The Spill focuses on stocks financial pros are researching and judges how good of buys they are. If you’re already sold, you can sign up for The Spill – for free – here. |

|

Proprietary Data Insights Financial Pros Top Semiconductor Stock Searches in the Last Month

|

|

Technology |

A 10/10 Buffett Gem |

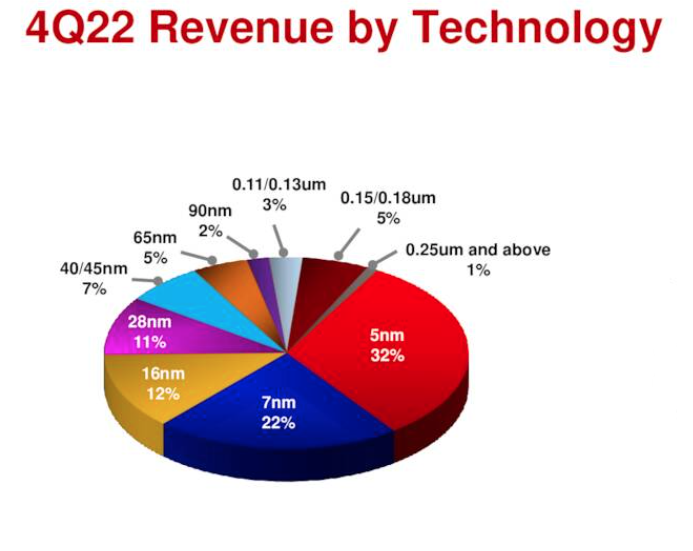

In Q3 2022, Warren Buffett’s company, Berkshire Hathaway, bought over 60 million shares of Taiwan Semiconductor Manufacturing (TSM). TSM is one of financial pros’ most searched semiconductor stocks, according to our proprietary Trackstar database. And after the company’s Q4 earnings announcement on January 12, which included a fairly upbeat forecast from management, search volume spiked. It might have to do with Buffett being a shareholder, the company’s 44.9% profit margins, and/or its $52.4 billion in net operating cash flow. If TSM is a good enough stock for Buffett, is it good enough for you? Taiwan Semiconductor’s Business Taiwan Semiconductor has the world’s largest semiconductor foundry, the part of the semiconductor supply chain that manufactures chips. TSM enables roughly 85% of worldwide semiconductor startup product prototypes. The company produces 12,302 products and employs 291 process technologies to serve hundreds of big-name customers with the world’s largest logic capacity. Excluding memory, TSM has 26% of the semiconductor market share. Across nearly every measure, it’s the largest semiconductor company in the world. Source: Taiwan Semiconductor TSM’s clients include some of the world’s largest tech companies, such as Apple, Qualcomm (#4 in financial pros’ semiconductor stock searches), and Huawei. TSM accounts for about 90% of the world’s super-advanced computer chips. Management plans to bring its most advanced chip manufacturing to Arizona in efforts to reduce delivery time along its supply chain. The company made $19.9 billion in revenues during Q4 2022, a jump of 26.7% from Q4 2021. The firm offered the following guidance for Q1 2023:

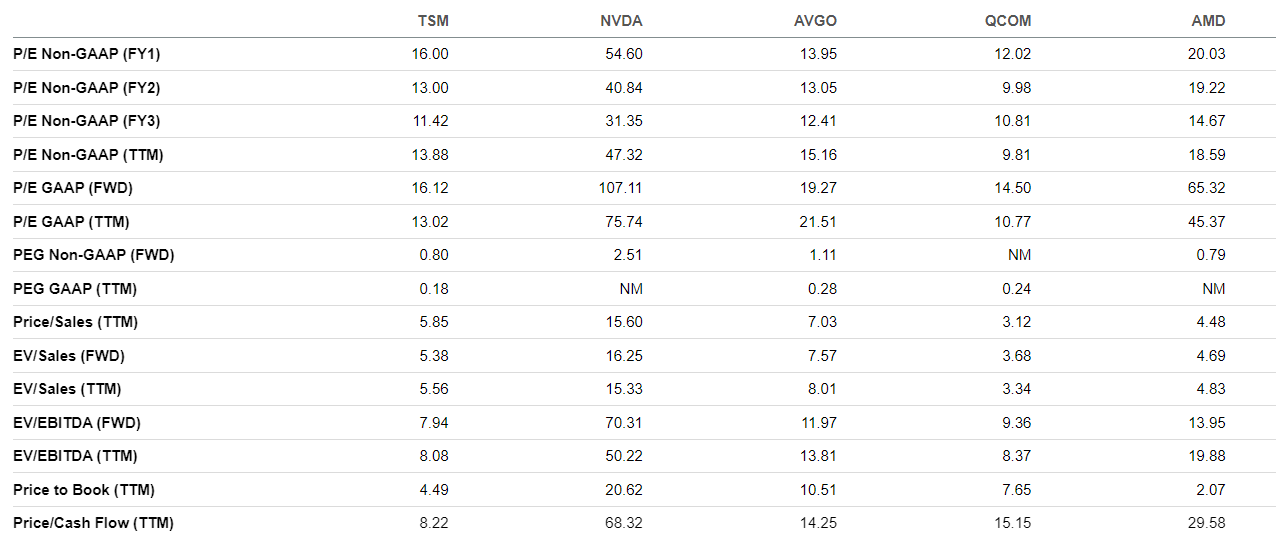

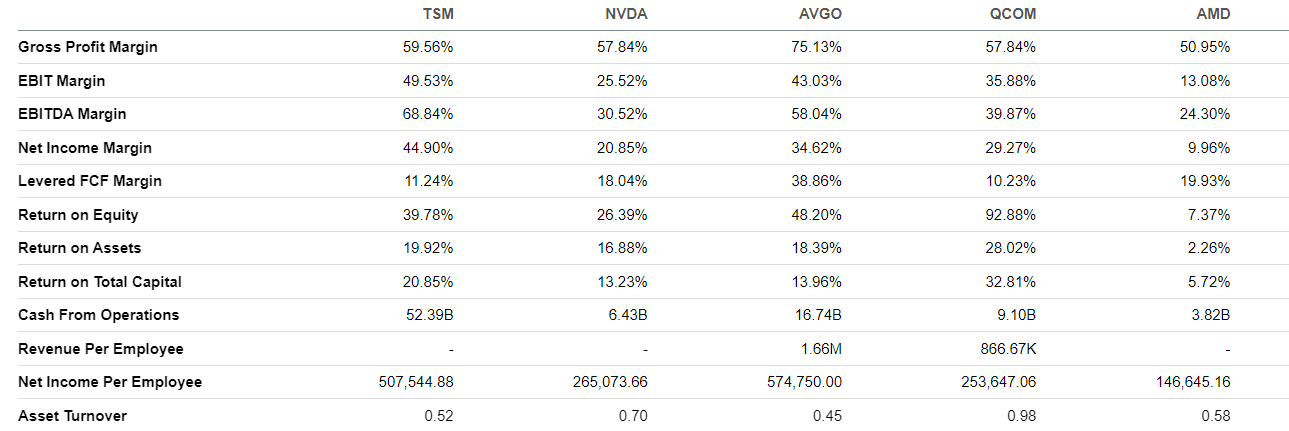

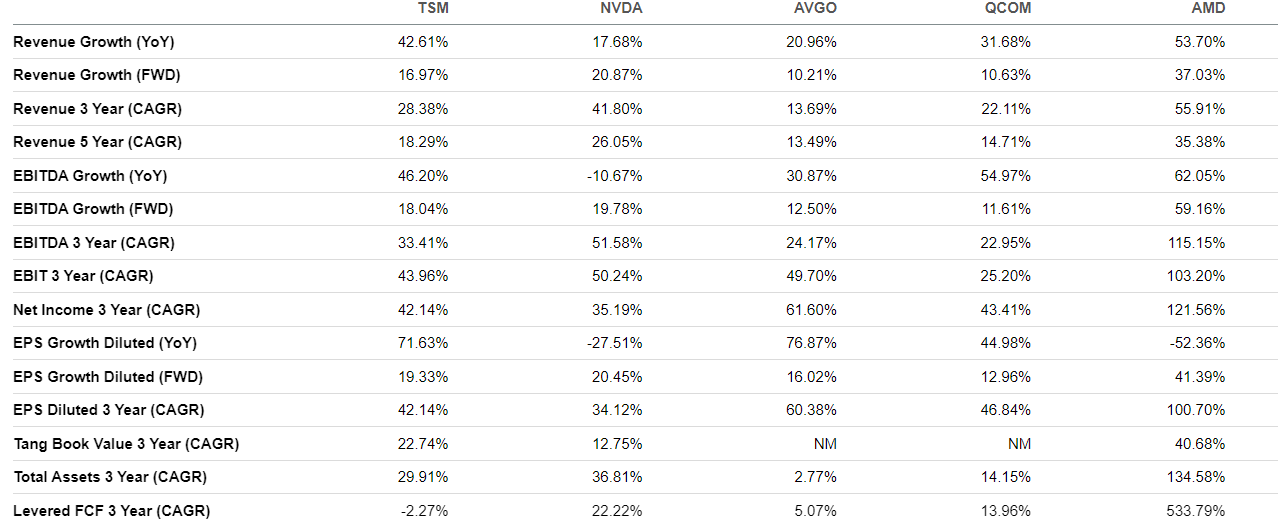

Much of the company’s optimism stems from tech companies’ upgrade cycle to more advanced chipsets as these companies vie for the top spot in their industries. Financials Financials are in millions of Taiwan dollars. Source: Stock Analysis TSM is financially stable, with a current ratio (current assets divided by current liabilities; the higher the ratio, the better financial position a company is in) of 2.2x. In Q4, revenues increased by 42.8%, and TSM’s net profit margin improved by 27.9% as demand for semiconductors outpaced supply. Moreover, operating income eclipsed 2021 by 77.6%. TSM’s Q4 2022 gross profit margin of 62.2% was 170 basis points better than the midpoint of its earlier gross margin guidance of 60.5%. Impressive figures like that are what attracted Warren Buffett to TSM. The stock also pays a steady income, with an annual dividend of $1.78 per share. Valuation Source: Seeking Alpha TSM trades at a 13.0x P/E GAAP (price-to-earnings generally accepted accounting principles) ratio, notably lower than peers Nvidia (NVDA) at 75.7x, Broadcom (AVGO) at 21.5x, and Advanced Micro Devices (AMD) at 45.4x. Qualcomm (QCOM) is cheaper, with a P/E GAAP ratio of 10.8x. It’s worth noting that TSM has 3x the market cap of QCOM and operates at a greater scale than QCOM. So TSM is larger and cheaper. Taiwan Semiconductor generates $52.4 billion in cash from its operations, significantly more than NVDA at $6.4 billion, AVGO at $16.7 billion, QCOM at $9.1 billion, and AMD at $3.8 billion. Additionally, TSM has a price-to-cash-flow ratio of 8.2x, much lower than NVDA at 68.3x, AVGO at 14.2x, QCOM at 15.2x, and AMD at 29.6x. Profitability Source: Seeking Alpha Taiwan Semiconductor’s net income margin of 44.9% is head and shoulders above its peers. AVGO is the second-highest at 34.6%, followed by QCOM at 29.3%, NVDA at 20.9%, and AMD at 9.9%. TSM plans to raise prices in 2023. It holds a near monopoly on advanced nodes, an area of the semiconductor space with insane growth. Advanced nodes give smartphones more powerful hardware, storage, and software capabilities. This momentum spurred the company’s upbeat forecast. Growth Source: Seeking Alpha TSM grew revenues 42.6% YoY, which is impressive compared to NVDA at 17.7%, AVGO at 20.9%, and QCOM at 31.7%. AMD grew revenues more at 53.7%. But AMD is 3.8x smaller than TSM. When you account for size, TSM’s growth numbers are downright eye-popping. There’s a lot of uncertainty in the semiconductor sector, including a global economic slowdown, supply disruptions, and geopolitical tensions between the U.S. and China. But TSM should grow revenues in 2023 as it starts raising prices. Our Opinion 10/10 TSM accounts for an estimated 90% of the world’s super-advanced computer chips. The company commands solid financials and robust profitability, and it pays a healthy dividend funded by cash, not debt. It trades at a discount in terms of P/E compared to most of its peers. No wonder Warren Buffett added it to his Berkshire Hathaway portfolio. The semiconductor sector incurred a massive correction over the last year, but we see it as a buying opportunity. We like TSM at these levels and rate the stock a strong buy. To get content like this daily, sign up for The Spill for free here. |

|

News & Insights |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |