|

Proprietary Data Insights Financial Pros Steel Services Stock Searches in the Last Month

|

|

Basic Materials |

Revenues up Triple Digits in the Past 3 Years |

One of the hottest stocks so far in 2023 isn’t an earnings winner, AI company, or January-effect stock. Cleveland-Cliffs (CLF) is 176 years old and up more than 26% over the first three weeks of the year. And in the last month, it’s been the top steel services stock financial pros have searched, according to the latest data from our proprietary Trackstar database. The company had triple-digit revenue growth over the last three years as it continues to stage one of the most impressive turnarounds of this decade. A global recession could cool this hot-rolled stock. But we believe there are more reasons to love shares than leave them at the door. Cleveland-Cliffs’ Business Formerly known as Cliffs Natural Resources, Cleveland-Cliffs is the largest producer of iron ore pellet and flat-rolled steel in North America. Additionally, it owns and operates coal and iron ore terminals and iron ore pellet production facilities. The company sells iron ore to integrated steel companies as raw materials in steel production. With its three mines in Minnesota and two in Michigan, the company boasts a rated capacity of 27.4 million long tons of iron ore pellet production annually, which represents 55% of the total pellet production capacity in the U.S.. That’s kind of crazy considering that in 2019, CLF produced no steel. In December of that year, it merged with AK Steel Holding, giving CLF 68% of the combined company and AK Steel the other 32%. In December 2020, the company acquired all the operations of ArcelorMittal USA. CLF’s current structure considers most operations part of steelmaking, with the remainder part of “other businesses.” The company sells 31% of its products directly to automotive customers. Cliffs’ primary direct carbon automotive sales market is based on fixed pricing. So fluctuating spot prices don’t affect it. CLF projects fixed-price contracts will account for 40% to 45% of steel volume sales and more than half of total steel revenue in 2023. Source: Cleveland Cliffs The company was founded in 1847, making it one of the oldest mining companies in the United States. Financials Source: Stock Analysis CLF grew revenue from $5.3 billion in 2020 to a stunning $20.4 billion in 2021. Some of the critical factors contributing to its rapid growth include:

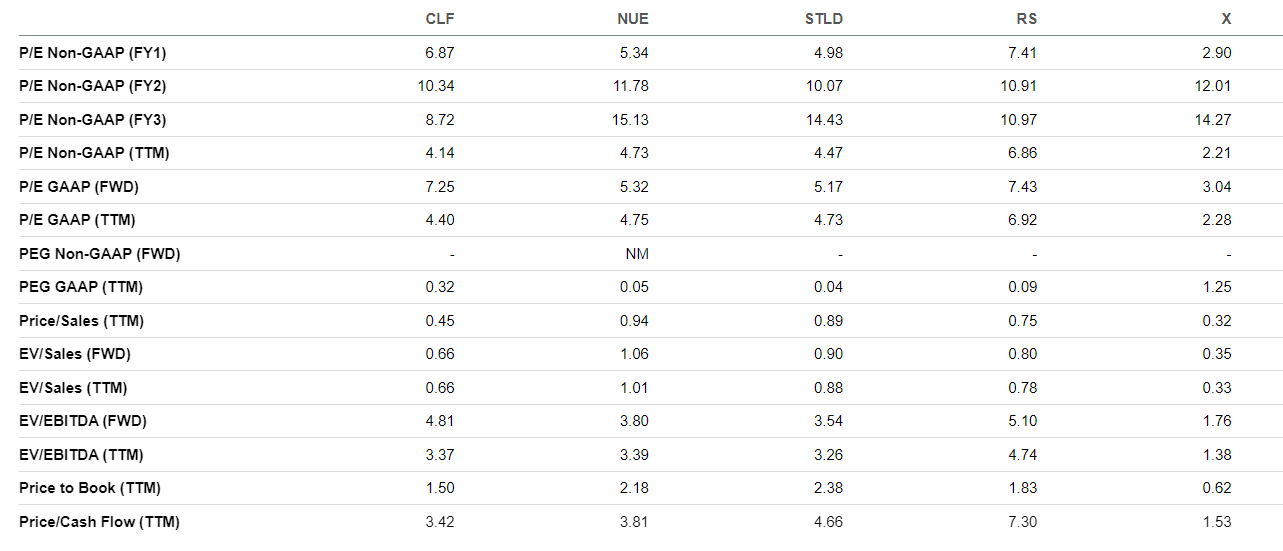

The company boosted its assets from $1.9 billion in 2016 to $19.6 billion in the trailing 12 months. Its liabilities began steadily declining in 2020, going from $13.6 billion to $12.4 billion TTM. And revenues continue to increase. Shareholder equity rose significantly over the last three years, from $358 million in 2019 to $7.0 billion TTM. The company’s current ratio of 2.3x is its highest since 2018. Valuation Source: Seeking Alpha Overall, CLF’s P/E GAAP ratio of 4.4x is relatively low compared to its peers Nucor (NUE) at 4.8x, Steel Dynamics (STLD) at 4.7x, and Reliance Steel & Aluminum (RS) at 6.9x, but it’s not as cheap as United States Steel (X) at 2.3x. But CLF is far less sensitive to fluctuations in steel prices than U.S. Steel or Nucor. It’s worth noting that Reliance Steel & Aluminum operates metals service centers and therefore is more aligned with overall steel and aluminum demand rather than spot steel prices. Price-to-sales ratio compares the market value of a company to its revenue. At 0.5x, CLF is cheaper than NUE at 0.9x, STLD at 0.9x, and RS at 0.8x, but not as cheap as X at 0.3x. CLF has a price-to-cash-flow ratio of 3.4x, notably lower than NUE at 3.8x, STLD at 4.7x, and RS at 7.3x, but higher than X at 1.5x. Profitability

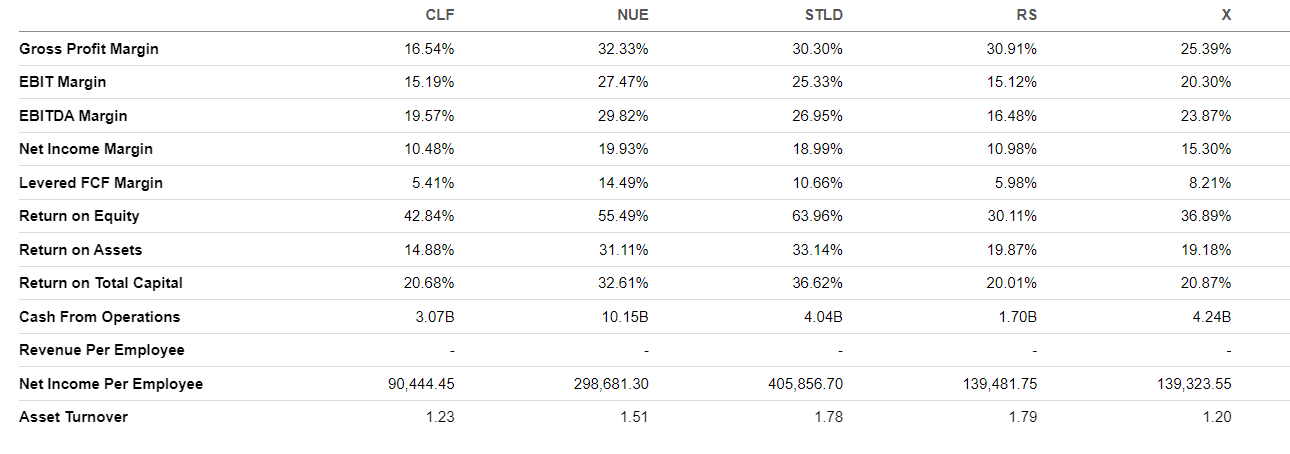

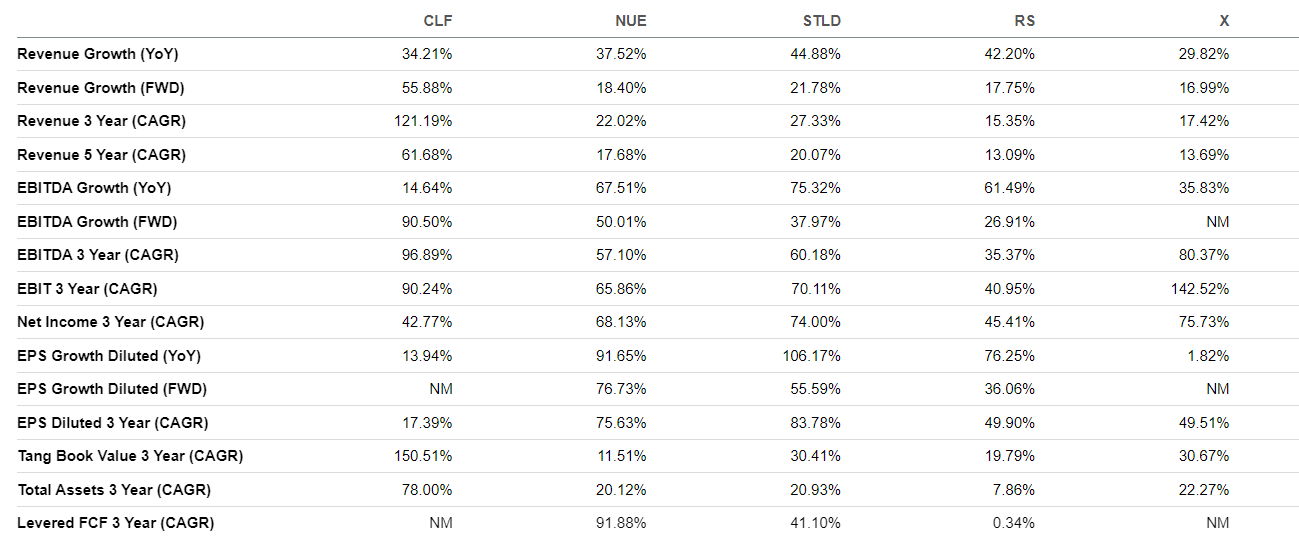

Source: Seeking Alpha Cliffs’ profitability metrics aren’t as strong as its competitors’. For example, its net income margin of 10.5% is the worst among its peers, with NUE at 19.9%, STLD at 18.9%, RS at 10.9%, and X at 15.3%. CLF’s EBIT margin of 15.2% is about the same as RS at 15.1%, but is notably lower than NUE at 27.5%, STLD at 25.3%, and X at 20.3%. CLF’s return on equity of 42.8% beats RS at 30.1% and X at 36.9%, but pales in comparison to NUE at 55.5% and STLD at 63.9%. Overall, NUE and STLD have stronger profitability metrics than CLF, RS, and X. Growth Source: Seeking Alpha These steel-related companies grew explosively compared to other sectors YoY. X’s revenue grew 29.8%, the lowest among the group. STLD had the highest at 44.9%, followed by RS at 42.2%, NUE at 37.5%, and CLF at 34.2%. But when you look at the last three years, none of the other companies above can compare to Cliffs’ 121.1% revenue growth. The closest any of them come is STLD at 27.3%, followed by NUE at 22.0%, X at 17.4%, and RS at 15.4%. These numbers include acquisitions, so take them with a grain of salt. Our Opinion 8/10 CLF has been one of the hottest stocks this month, rising more than 26%. Despite being over 175 years old, the company adjusts to market conditions as it needs to. Its acquisition of AK Steel falls into that category. The company has a strong balance sheet and is cheaper than its peers. We like the stock and would buy on any pullbacks after this recent run to above $21. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |