|

Proprietary Data Insights Financial Pros Fast Food Chain Stock Searches in the Last Month

|

|||||||||||||||||||||

|

Restaurants |

|

Safety and Growth Rolled Into One |

|

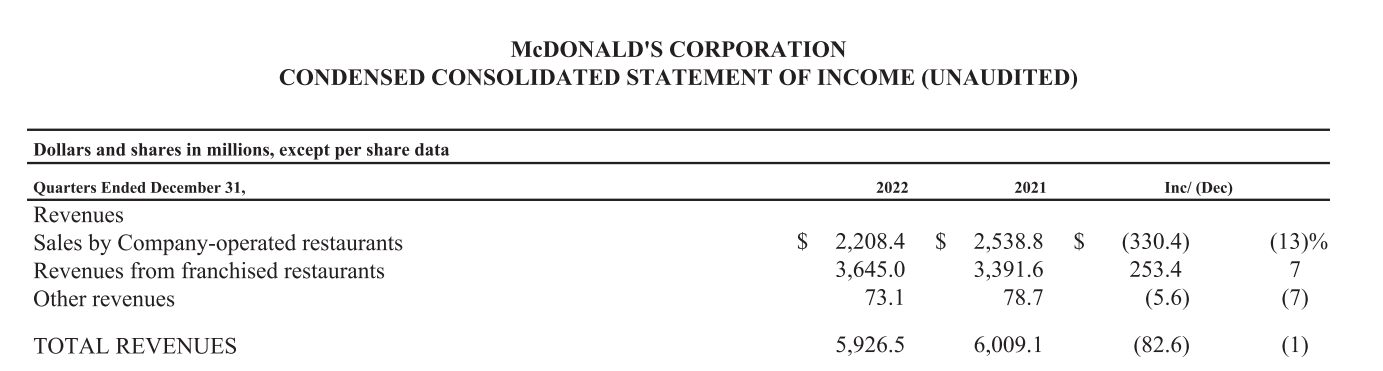

Savvy consumers are saying goodbye to overpriced restaurants and hello to better-value offerings. McDonald’s (MCD) is the big winner in this shift. The company’s latest quarterly report showed that global comparable sales increased by over 12%, and according to Trackstar’s latest search data, financial pros are taking notice. It pulled in nearly 1,000 searches over the last month, edging out Chipotle Mexican Grille (CMG), a company it owned until 2006 when it spun it off in its own IPO. McDonald’s outperformed the overall market in 2022 but has lagged so far in 2023. The home of the golden arches is largely insulated from inflationary pressure thanks to its mostly franchised business model, making it a compelling investment choice in any market environment. Yet, it faces recessionary headwinds, a complete business shutdown in Russia, and a strong dollar. However, we love the company’s strong fundamentals, clever business model, and consistent cash flow. McDonald’s Business McDonald’s is the largest publicly traded company in the restaurant sector, with a market cap of $192.7 billion. Its fast-food chains can be found worldwide in over 100 countries, with more than 40,000 restaurants. The company operates on a franchise model, meaning that most of its restaurants are owned and operated by franchisees, not the company itself. As of 2021, it is estimated that only about 10% of McDonald’s restaurants worldwide were company-owned, which comes as a surprise to most people. However, the company does own a significant amount of real estate, including the land on which many of its franchise locations are built, giving it tangible assets with paying tenants. Consequently, franchised restaurants account for more than half the company’s total revenues, and have better margins than owned locations. Source: McDonald’s The company’s digital systemwide sales were over $7 billion in its top six markets during Q4 2022, representing an increase of more than 35% of its systemwide sales. The quarter also revealed that global comparable sales increased by over 12%, with double-digit growth across all segments. McDonald’s is unique in its vertical supply chain involvement. It owns and operates several distribution centers, manufacturing facilities, and corporate offices. The exact amount of real estate owned by McDonald’s is not publicly disclosed but is considered a significant asset for the company. Plus, the company is actively involved with the farmers and companies that supply many of its products from chicken to potatoes. Financials Source: stockanalysis.com Despite uncertainty in the economy and inflationary pressures persisting in 2022, the company managed to record its highest profit margins. MCD increased its profit margins from 19.0% in 2016 to 25.4% in 2022. Meanwhile, its free cash flow margin has improved from 17.6% in 2016 to 25.4% in 2022. The company has increased its annual dividend from $4.19 in 2018 to $6.08 in 2023. While inflation is hurting most businesses, McDonald’s is bucking the trend, experiencing a spike in traffic thanks to its value proposition to consumers and continued focus on improving food quality and the customer experience. The company reported a Q4 net income of $1.9 billion, up from $1.64 billion a year earlier. It shouldn’t come as any surprise the company has plenty of cash to execute its Accelerating the Arches strategy 5 pillars:

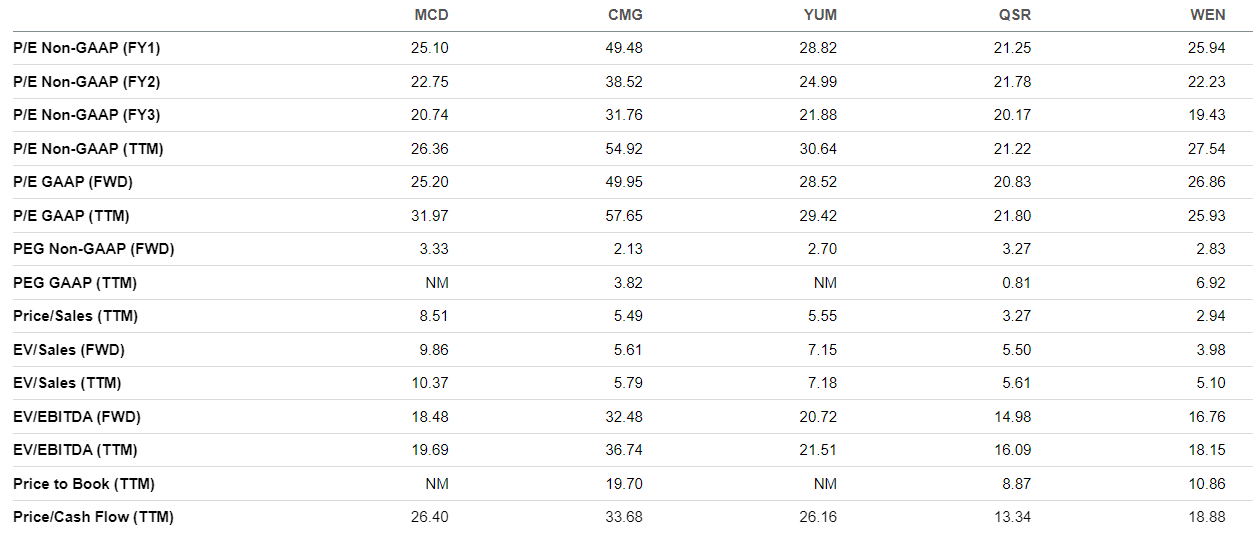

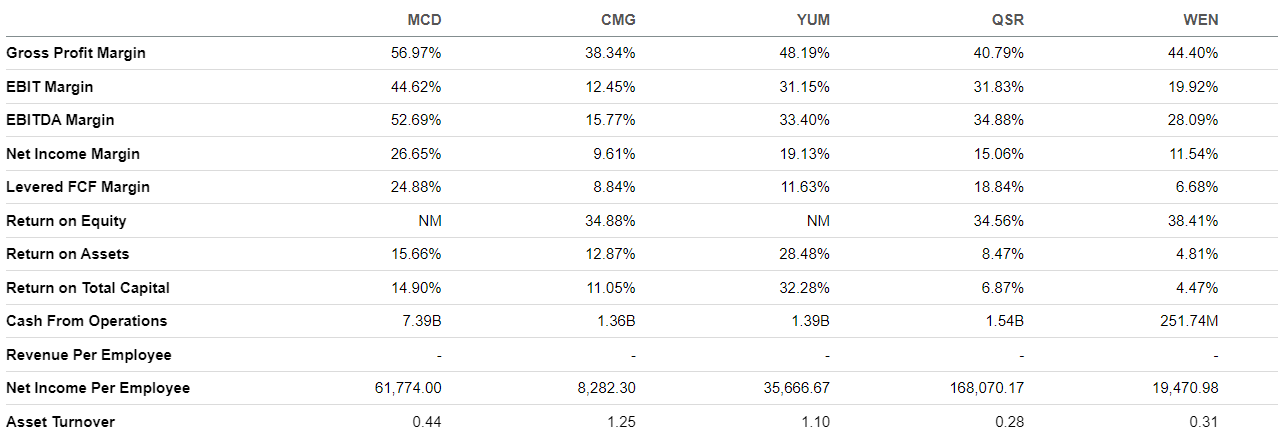

We’re excited the company isn’t resting on its laurels, instead investing its $7.4 billion in operating cash flow in its future while still paying a healthy 2.28% dividend. The 1.4x current ratio is another indicator of its financial health. The company will have no issue paying its short-term obligations. Valuation Source: Seeking Alpha MCD trades at a P/E GAAP ratio of 31.9x, slightly above its 5-year average of 28.0x. Additionally, it trades at a higher multiple than Yum! Brands (YUM) at 29.4x, Restaurant Brands International (QSR) at 21.8x, and Wendy’s (WEN) at 25.9x. However, it’s cheaper than high-growth Chipotle Mexican Grill (CMG) at 57.7x. Its price-to-sales ratio of 8.5x is also higher than its 5-year average of 7.5x and considerably higher than its peers. For example, CMG is at 5.5x, YUM is at 5.6x, QSR is at 3.3x, and WEN is at 2.9x. Investors feel comfortable paying a premium for McDonald’s, given its brand recognition, highly profitable business model, dividend payout, and management’s ability to navigate difficult economic times. Profitability Source: Seeking Alpha Comparing profitability among the group makes it clear why investors are willing to pay a premium for MCD. For example, its EBIT margin of 44.6% is head and shoulders above CMG at 12.5%, YUM at 31.2%, QSR at 31.8%, and WEN at 19.9%. But that’s not all. McDonald’s net income margin of 26.7% trounces CMG at 9.6%, YUM at 19.1%, QSR at 15.1%, and WEN at 11.5%. Moreover, McDonald’s has cash, a lot of it. The company generates $7.4 billion in cash from its operations. Unlike its peers, McDonald’s collects revenue from its franchisees and is not as greatly impacted by wage and cost inflation. Growth Source: Seeking Alpha The fast-food sector experienced several headwinds in 2022 from inflation to worker shortages. However, MCD managed to grow its EBITDA by 4%. Now, that’s not nearly as strong as CMG at 27.5% or QSR at 7.2%. But it’s not bad, considering YUM was at -2.1% and WEN was at -3.2%. The company’s revenue growth of -0.2% isn’t blowing anyone away. In fact, its peers did notably better. For example, CMG was at 16.9%, YUM was at 4.3%, QSR was at 14.6%, and WEN was at 7.6%. On the bright side, MCD is growing its dividends, as it has for decades, which is attractive to investors seeking income. Our Opinion 7/10 MCD is relatively overvalued. However, it justifies a premium. If it was cheaper, we’d likely give it a 10/10. Unlike its peers, it generates most of its revenues from franchisees, making it less vulnerable to wage and inflation shocks. We like the stock as a long-term investment and would look to accumulate shares above the 200-day moving average of $257. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |