Editor’s Note: |

It’s Friday. Time to give you a stock pick from our sister newsletter, The Spill, so you can think about it over the weekend and maybe make a move Monday morning. While The Juice helps you be better with money across the board, The Spill focuses on stocks financial pros are researching and judges how good of buys they are. If you’re already sold, you can sign up for The Spill – for free – here. |

|

Proprietary Data Insights Financial Pros Software Stock Searches in the Last Month

|

|||||||||||||||||||||

|

Software |

Google May Not Be King Much Longer |

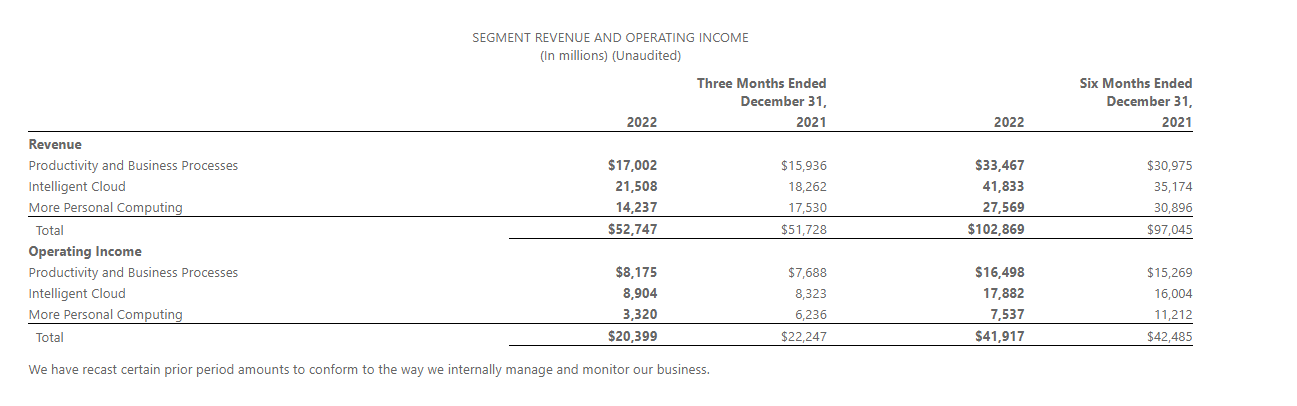

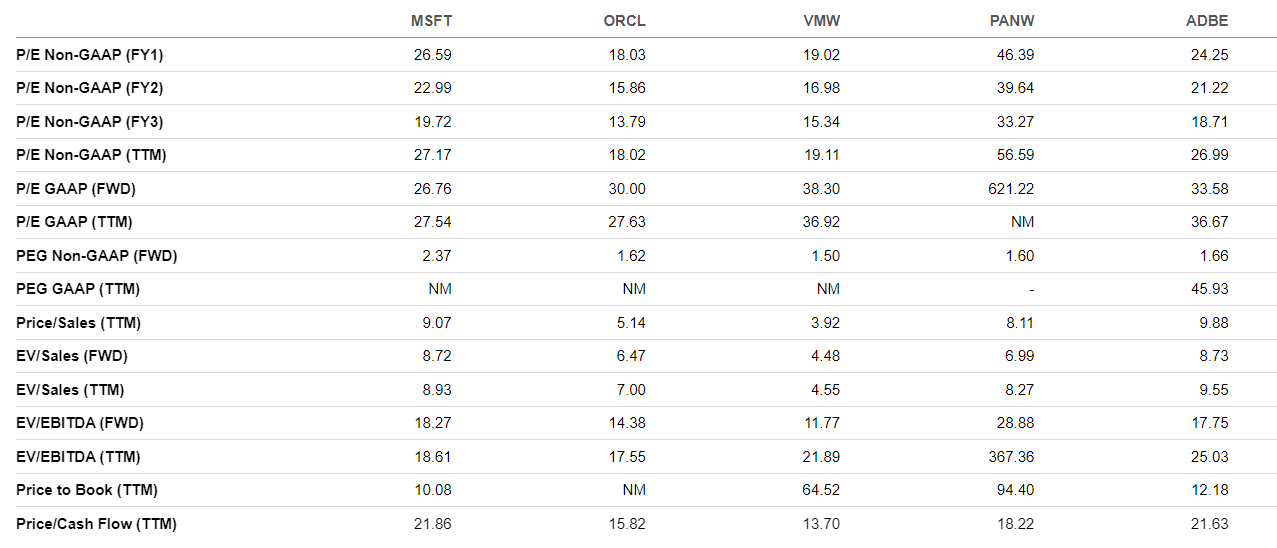

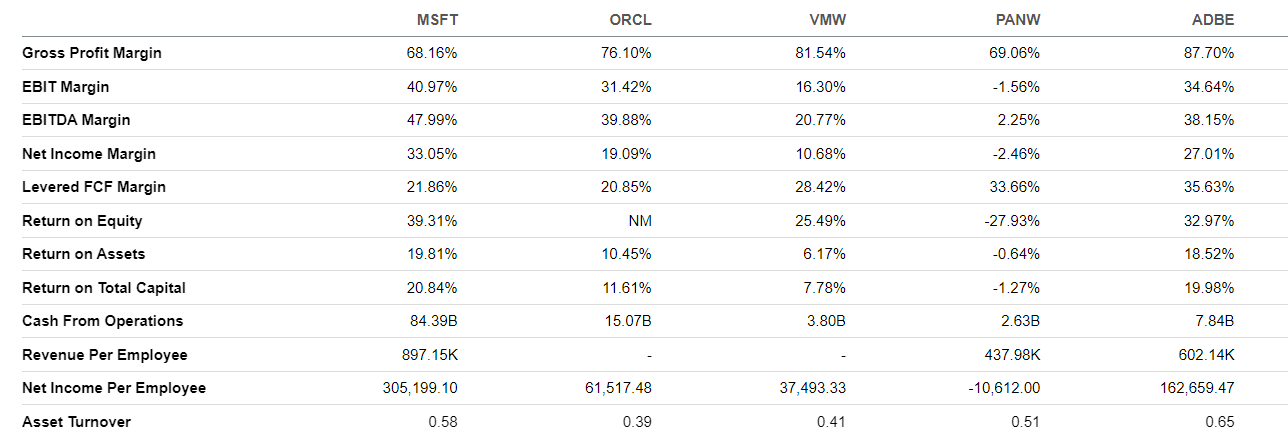

Google has dominated search for more than two decades. But that may change very soon thanks to Microsoft (MSFT)’s potential deal with OpenAI, which would give it a 49% stake in the company that owns ChatGPT. Microsoft plans to implement ChatGPT in its Bing search engine sometime in March. According to the latest data from our proprietary Trackstar sentiment indicator, Microsoft tripled in search volume from financial pros in a matter of weeks, making it one of the most popular stocks over the last month – more popular than all but three stocks. Financial pros were ecstatic about the company’s latest earnings report, which showed its new developments in the AI sector and that Microsoft Azure grew 38%. Yet the stock has underperformed the Nasdaq year to date. Does that make this company a bargain or another busted tech stock? Mircosoft’s Business Legendary software developer Bill Gates founded Microsoft in 1975, when he was just 20. But it wasn’t until it landed a deal with IBM to supply it with an operating system in 1980 that things really took off. With the release of the game-changing Windows operating system in 1983, Microsoft exploded onto the scene. It soon became the largest company in the world, and Gates the richest man on the planet. Today, Microsoft is a tech powerhouse, selling everything from PCs to cloud systems, software, and gaming platforms. The company’s empire includes LinkedIn, Skype, Nuance Communications, GitHub, and likely Activision Blizzard (pending deal). Microsoft smoothly and impressively transitioned from traditional software to the cloud. And now, Microsoft Cloud is set to turn the world’s most advanced AI models into a new computing platform. Microsoft breaks its revenue into three segments: Productivity and Business Processes, Intelligent Cloud, and More Personal Computing. Source: Microsoft In late January, the company announced it would slash 10,000 jobs to adjust to a broad tech-industry slowdown that has led customers to spend cautiously. Yesterday, news hit that Microsoft would include fast-growing tech platform ChatGPT in its Bing search engine in the coming weeks. The company has invested $10 billion in OpenAI, which owns ChatGPT. Techies and analysts hail ChatGPT as the next wave in AI technology. The natural-language interface allows users to type questions as they would speak them to a person. The system then responds remarkably fluently and comprehensibly. If you haven’t seen demonstrations, we recommend checking out some YouTube videos that show off the potential. Microsoft believes ChatGPT could revolutionize search, eclipsing Google by making it easier to access and retrieve relevant information. Furthermore, there’s talk the program’s ability to produce well-written content could replace human-written SEO articles. Financials Source: Stock Analysis Microsoft’s Azure cloud computing platform is one of the top cloud service providers in the world. It enabled MSFT to reach new heights, taking revenues from $91.1 billion in 2016 to $198.2 billion in 2022. The transition to the cloud has also boosted profit margins from 22.5% in 2016 to 36.7% in 2022. Additionally, MSFT’s net income margin exploded from $20.5 billion in 2016 to $72.7 billion in 2022. The firm is in an excellent financial position, with $99.5 billion in total cash and $77.9 billion in total debt. Its 1.9x current ratio (current assets divided by current liabilities; the higher the ratio, the better financial position a company is in) is another strong indication of the company’s financial health. Valuation Source: Seeking Alpha MSFT trades at a P/E GAAP (price-to-earnings generally accepted accounting principles) ratio of 27.5x, notably lower than its five-year average of 30.8x. Some of its peers, like Oracle (ORCL), VMWare (VMW), and Adobe (ADBE), trade at lower multiples but aren’t as diversified and don’t have such booming cloud businesses. Microsoft’s price-to-sales ratio of 9.1x is lower than ADBE’s 9.9x but significantly higher than ORCL’s 5.1x, VMW’s 3.9x, and Palo Alto Networks (PANW)’s 8.1x. But MSFT’s is still below its five-year average of 9.8x. In Q2 2023 (what MSFT calls last quarter), Microsoft reported cloud revenue of $27.1 billion, up 22% YoY. Revenue from Azure and other cloud services grew 31%. It helped counter the 39% drop in OEM (original equipment manufacturer) Windows revenue and another 39% drop in devices revenue. It appears Wall Street is willing to pay a premium for cloud and AI companies, two areas Microsoft is focused heavily on. Profitability Source: Seeking Alpha Microsoft’s cloud business has made the company more profitable over the years. MSFT’s net income margin of 33.1% is unmatched compared to peers ORCL at 19.1%, VMW at 20.8%, PANW at -2.5%, and ADBE at 27.0%. In addition, MSFT boasts an incredibly high EBIT margin of 40.9%. ADBE is at 34.6%, VMW is at 16.3%, ORCL is at 31.4%, and PANW is at -1.6%. Microsoft’s $10 billion investment in ChatGPT is just a drop in the bucket for it. The company generates $84.3 billion in cash from operations every year, significantly higher than ORCL at $15.0 billion, VMW at $3.8 billion, PANW at $2.6 billion, and ADBE at $7.8 billion. Growth Source: Seeking Alpha When the global economy sneezes, it’s hard for Microsoft not to catch a cold. The company decided to lay off 10,000 employees as uncertainty around the economy persists. Despite a difficult 2022, the company grew revenues 10.4%. That’s better than VMW at 4.4%, but not as good as ORCL at 11.3%, PANW at 27.7%, and ADBE at 11.5%. Management believes the future is in AI, and it’s committed to doubling down on its cloud and AI business, which should help bolster growth in the coming years. Our Opinion 7/10 So far in 2023, Microsoft has underperformed the Nasdaq-100. The company’s valuation is a bit rich, especially with many other tech stocks trading at huge discounts. But if you’re a long-term investor, you should be excited about Azure’s 38% growth and Microsoft’s focus on AI. Though we believe prices may dip back down to $230-$240, we’d begin establishing a position here. It’s hard to go wrong with Microsoft. To get content like this daily, sign up for The Spill for free here |

|

News & Insights |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |