|

Proprietary Data Insights Financial Pros Social Media Stock Searches in the Last Month

|

|||||||||||||||||||||

|

Technology |

Is Now Still Time to Buy Meta? |

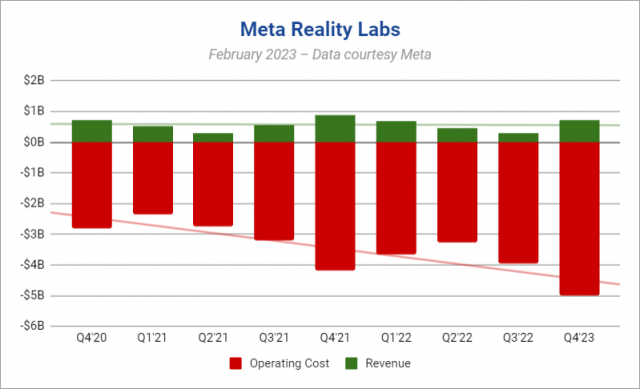

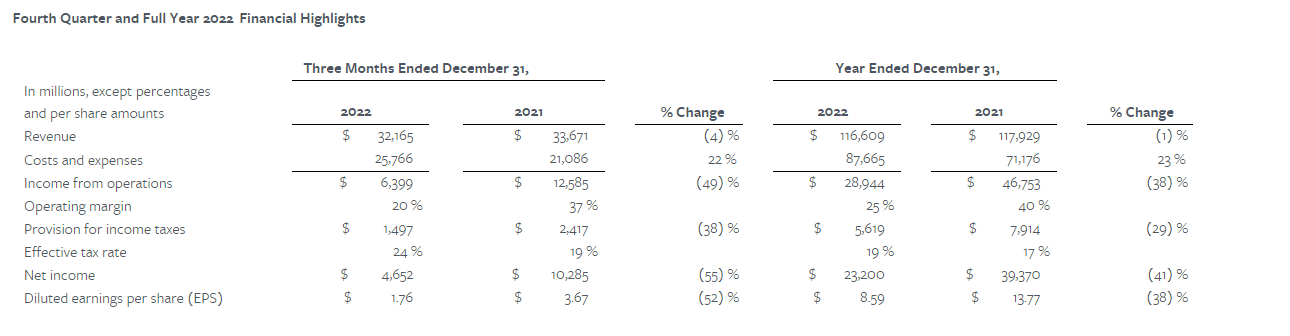

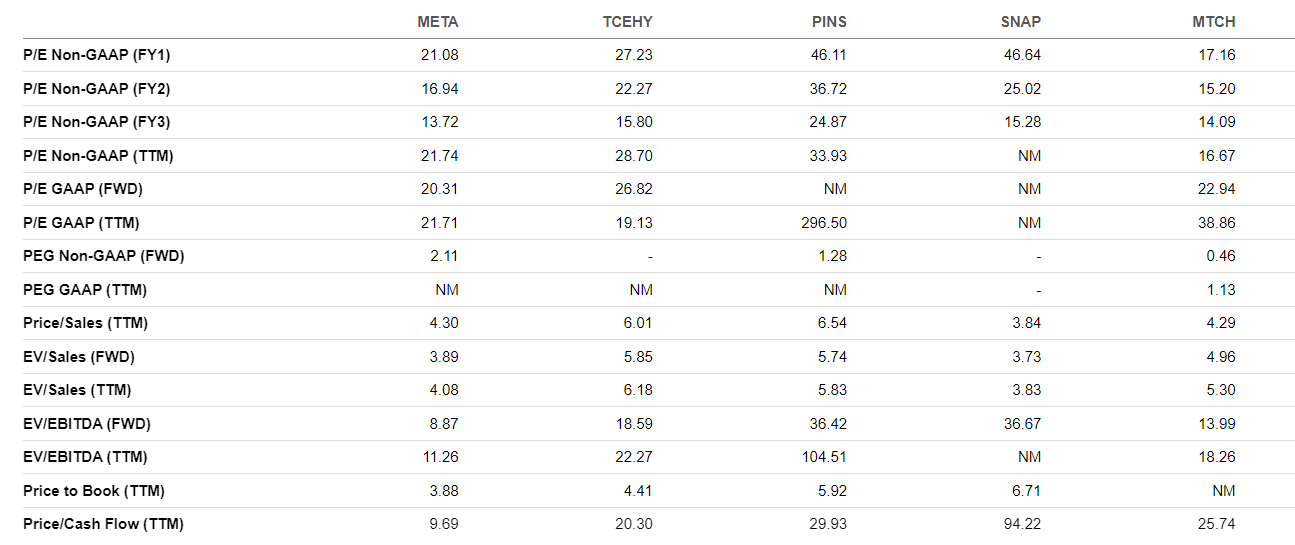

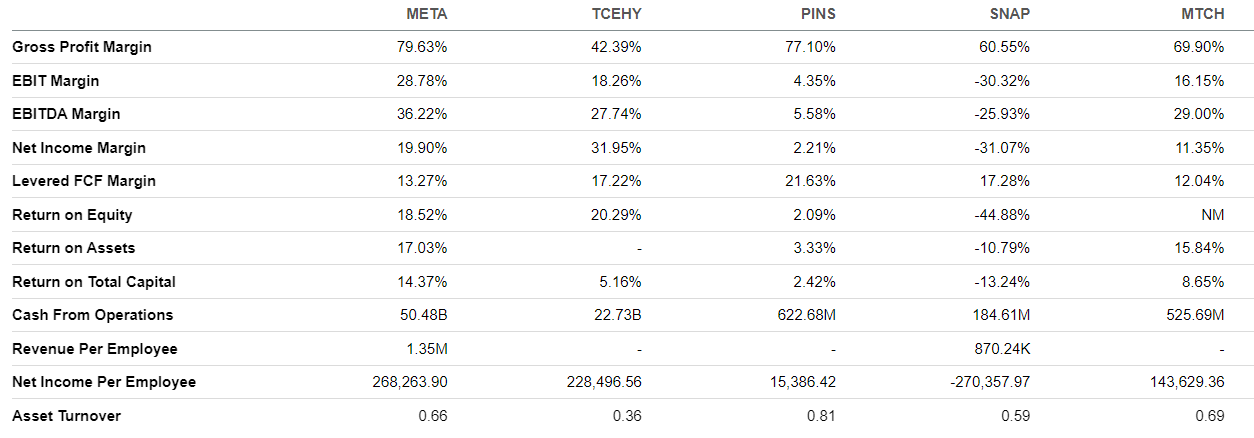

Meta Platforms (META) CEO Mark Zuckerberg lost over half his net worth in 2022. Despite record cash flow, Meta faced lower advertising spends and customer saturation. Plus, its metaverse bets came nowhere close to paying off. The company changed its name in 2021 from Facebook to Meta Platforms to reflect the company’s new focus on virtual reality and the metaverse. But things are starting to look up for Zuckerberg in 2023. In fact, after Meta’s latest earnings release, his net worth jumped $12.5 billion in one day. Meta shares have been on fire to start the year. According to our proprietary Trackstar database, financial pros made it their top social media stock search and one of their top 15 most searched stocks over the last month. We covered Meta Platforms last September, but given the stock’s rise and upbeat earnings report this month, we believe it’s worth revisiting. We wrote in September that buying META was an absolute steal, as it traded at a price-to-earnings ratio of 12.1x. But with the stock up more than 51% year to date, has that ship sailed? Meta Platforms’ Business Meta owns and operates some of the world’s largest and most successful social media platforms. They include Facebook, Instagram, Messenger, and WhatsApp. Facebook alone has nearly 3 billion active users monthly and 2 billion active users daily. Across Meta’s family of apps, there are nearly 3 billion active users daily. In addition, the company owns Oculus, a maker of virtual and augmented reality headsets and games. It’s part of Meta’s Reality Labs division, which generated $727 million in revenue in Q4 2022, a 17% drop compared to Q4 2021. Wall Street was more excited about the company’s bread and butter, ad revenue. Source: Meta Platforms CEO Zuckerberg’s enthusiasm toward the metaverse sent his stock spiraling out of control last year, to a low of $88.09 last November. But during its Q4 2022 earnings call, Meta shifted the focus from the metaverse to AI, messaging, and expenses. The company is using AI to promote engagement across Facebook and Instagram while enhancing its Reels product. Source: Meta Platforms Meta shares soared after its Q4 earnings announcement, adding $100 billion to its market cap. The company emphasized it will heavily focus on cutting expenses, which is music to Wall Street’s ears. In addition, the company will start a $40 billion share buyback program. Financials Source: Stock Analysis Meta’s revenues grew from $55.8 billion in 2018 to $116.6 billion in 2022. But they slowed from 2021 to 2022. The company is now focused on cutting expenses, as we said, and improving efficiency. Its net income fell from $39.3 billion to $23.2 billion over the last year. Operating income dropped from $47.2 billion to $28.8 billion. META’s profit margin also declined substantially, from 39.6% in 2018 to 19.9% in 2022. While Reality Labs and ad revenue are struggling, the company sees some bright spots, specifically Reels, which it believes can be profitable by the end of 2023 or early 2024. Meta laid off 11,000 employees, which will show in its headcount by the end of this quarter. The company has $40.7 billion in cash, cash equivalents, and marketable securities as of December 31, 2022, with $9.9 billion in long-term debt. Valuation Source: Seeking Alpha META trades at a P/E GAAP of 21.7x, well below its five-year average of 25.1x. Despite its stock price rising 51% YTD, it’s still relatively cheaper than Pinterest (PINS) at 296.5x, Snap (SNAP) at NM (not meaningful), and Match Group (MTCH) at 38.9x. But Tencent Holdings (TCEHY), the developer of WeChat, trades at a lower multiple at 19.1x. META trades at a price-to-cash-flow ratio of 9.7x, significantly lower than its five-year average of 16.3x and well below its peers TCEHY at 20.3x, PINS at 29.9x, SNAP at 94.2x, and MTCH at 25.7x. With an EV/sales ratio of 4.1x, META’s overall financial health appears stronger than TCEHY’s at 6.2x, PINS’ at 5.8x, and MTCH’s at 5.3x. Only SNAP is lower at 3.8x. Profitability Source: Seeking Alpha Meta’s net income margin of 19.9% is considerably lower than its five-year average of 32.9%. It’s still better than PINS at 2.2%, SNAP at -31.1%, and MTCH at 11.4%, but it can’t compete with TCEHY at 31.9%. Meta hopes it can improve its profitability and margins by cutting expenses and focusing more on efficiency. The company’s EBIT margin remains strong at 28.8%, significantly higher than TCEHY at 18.3%, PINS at 4.4%, SNAP at -30.3%, and MTCH at 16.2%. While META and TCEHY have similar market caps, META generates considerably more cash from its operations, $50.4 billion vs. $22.7 billion. Meanwhile, PINS generates $622.6 million in cash from its operations, SNAP $184.6 million, and MTCH $525.6 million. This massive cash generation gives the company flexibility to adapt to market changes. Growth Source: Seeking Alpha If META were growing revenues, it wouldn’t be as concerned about cutting expenses. But 2022 was brutal for the company, as revenue declined 1.1%. In fact, META’s revenue growth numbers are the worst among the group. TCEHY was at 0.8%, PINS at 13.8%, SNAP at 11.8%, and MTCH at 6.9%. Its EBITDA growth of -22.8% is better than SNAP and PINS, but weaker than TCEHY at -16.0% and MTCH at -0.5%. Our Opinion 7/10 When we wrote about META last September, it was trading at a P/E multiple of 12.1x. It’s currently at 21.7x. While it’s not nearly as cheap as it was back then, it’s still cheaper than tech giants Apple, Amazon, and Alphabet. We still like META. It currently trades above $188. We believe if you can get in near $150 to $160, it will bring excellent returns in the coming years. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |