|

Proprietary Data Insights Financial Pros Aerospace & Defense Stock Searches in the Last Month

|

|||||||||||||||||||||

|

Aerospace & Defense |

Should You Follow the Boeing Insiders? |

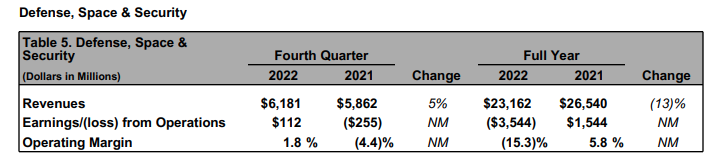

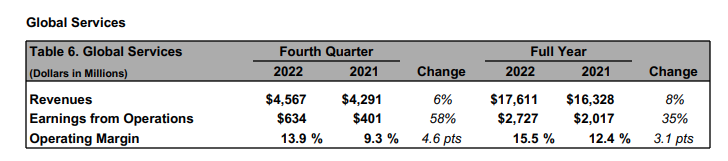

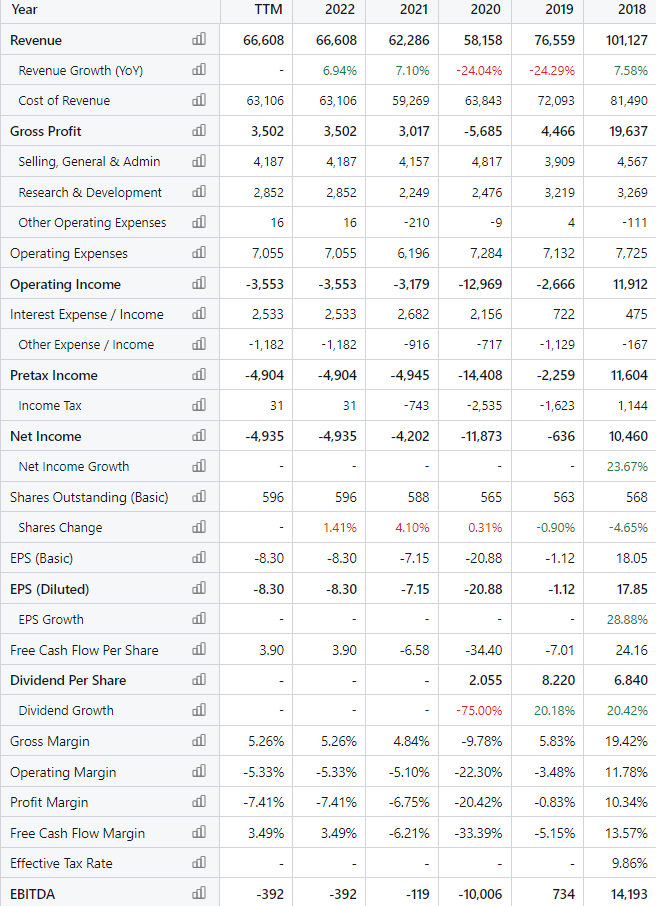

Sometimes the best indicators of a stock’s future performance aren’t analysts or hedge funds. They’re insiders of the company. We can learn a lot from their buying and selling of stock. For example, Boeing (BA) insiders have been buying shares hand over fist over the last year. They haven’t sold yet. It’s likely a big reason financial pros searched for the stock over 6,000 times in the last month and have made it their top search in aerospace and defense stocks for the past month and year. Plus, the latest data from our proprietary Trackstar sentiment indicator shows it’s one of the top 15 overall stock searches for the last month. Boeing CEO David Calhoun bought $4 million worth of stock when it traded at around $160 per share and hasn’t sold yet. Shares of the company are now at $212.89 – up over 88% from their 52-week low of $113.02. But the company faces inflationary headwinds and legacy problems from its 737 Max. Can the stock pull out of a tailspin? Boeing’s Business Chances are you’ve flown in one of Boeing’s airplanes. Boeing is a multinational aerospace and defense company that designs, manufactures, and sells airplanes, rotorcraft, rockets, satellites, telecommunications equipment, and defense security systems. It’s one of the largest global aerospace manufacturers and exporters in the United States. The company sells its advanced technologies to commercial and defense customers. Additionally, it provides support and maintenance services for its products, generating ongoing revenue streams for the company. It also offers financing and leasing solutions for its customers. It segments its business into Commercial Airplanes; Defense, Space & Security; and Global Services. Source: The Boeing Company In 2022, the company generated 38.8% of its revenues from Commercial Airplanes deliveries, 34.8% from Defense, Space & Security, and 26.4% from Global Services. Financials Source: Stock Analysis Boeing’s revenue has fallen from its 2018 peak of $101.1 billion. One of the major factors is the COVID-19 pandemic, which has significantly impacted the aviation industry. The sharp decline in air travel forced airlines to defer deliveries and cancel orders for new planes. Boeing also grounded its 737 Max aircraft following two fatal crashes, resulting in a major blow to the company’s financial performance. It struggled to deliver new planes, incurring significant costs related to designing and certifying aircraft. Budget cuts and delays in government procurement processes hurt its Defense, Space & Security business. But the company had an uptick in revenue following 2020, going from $58.1 billion to $66.6 billion in 2022. The Commercial Airplanes business revenues jumped from $19.4 billion in 2021 to $25.8 billion in 2022, with commercial plane deliveries jumping from 340 to 480. The company’s profit margins were -20.3% in 2020, but they’re improving. In 2022, they were -7.4%. Moreover, BA’s free-cash-flow margin has gone from -33.4% in 2020 to 3.5% in 2022. Boeing paid a dividend of $8.22 in 2020 before cutting it completely in 2021. The company has $17.2 billion in cash and $58.5 billion in debt. Its current ratio of 1.2x shows it has no issues paying its short-term liabilities. Valuation Source: Seeking Alpha BA isn’t profitable, and therefore has no P/E GAAP ratio. This is a more recent occurrence largely due to the pandemic and the 737 Max debacle. Typically, the company has had a P/E ratio between 15.0x and 21.0x. On a P/E basis, the company is overvalued compared to peers Lockheed Martin (LMT) at 21.7x, Raytheon Technologies (RTX) at 27.8x, Northrop Grumman (NOC) at 14.5x, and General Dynamics (GD) at 18.8x. Boeing’s enterprise-value-to-EBITDA of 102.7x also appears rich compared to LMT at 15.6x, RTX at 15.2x, NOC at 10.7x, and GD at 13.8x. BA looks more competitive with a price-to-sales ratio of 1.9x, with LMT at 1.9x, RTX at 2.2x, NOC at 2.1x, and GD at 1.9x. Profitability Source: Seeking Alpha BA has a net income margin of -7.4%, significantly better than in 2020, when it was -20.4%. But it’s weak compared to LMT at 8.7%, RTX at 7.8%, NOC at 13.4%, and GD at 8.6%. On the bright side, the company’s free-cash-flow margin went positive in 2022, at 3.5%, for the first time since 2018. In the last year, BA generated $3.5 billion in cash from its operations compared to LMT at $7.8 billion, RTX at $7.1 billion, NOC at $2.9 billion, and GD at $4.5 billion. Boeing’s EBIT margin of -0.5% is the worst among the group. LMT is at 11.3%, RTX is at 10.8%, NOC is at 17.3%, and GD is at 11.7%. Growth Source: Seeking Alpha Boeing’s Commercial Airplanes and Global Services segments’ sales popped higher in 2022. But Defense, Space & Security sales fell from 2021. Overall, the company managed to grow revenues 6.9%, more than LMT at -2.6%, RTX at 4.2%, NOC at 2.6%, and GD at 2.4%. In Q4 2022, BA delivered 152 commercial airplanes and recorded 376 net orders. The company’s backlog grew to $404 billion in 2022, including 4,500 commercial planes. Our Opinion 5/10 Boeing isn’t profitable right now, but it shows signs of improvement. Its quarterly revenue growth rose 35.1%. The company’s stock is up more than 88% from its 52-week low and is just 3% off its 52-week high. But it doesn’t appear to be out of the woods yet. The company recently announced it would cut around 2,000 jobs over the coming months in anticipation of a weaker global economy. Boeing would have to execute perfectly if you bought at these levels, and given all the uncertainty that remains in the economy, it’s a tall order. We’d hold off buying the stock until it drops to $150 to $175. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |