|

Proprietary Data Insights Financial Pros Surging Large-Cap Stocks Last Week

|

|||||||||||||||||||||

|

Industrial |

|

Advising Against This “Advisor” |

|

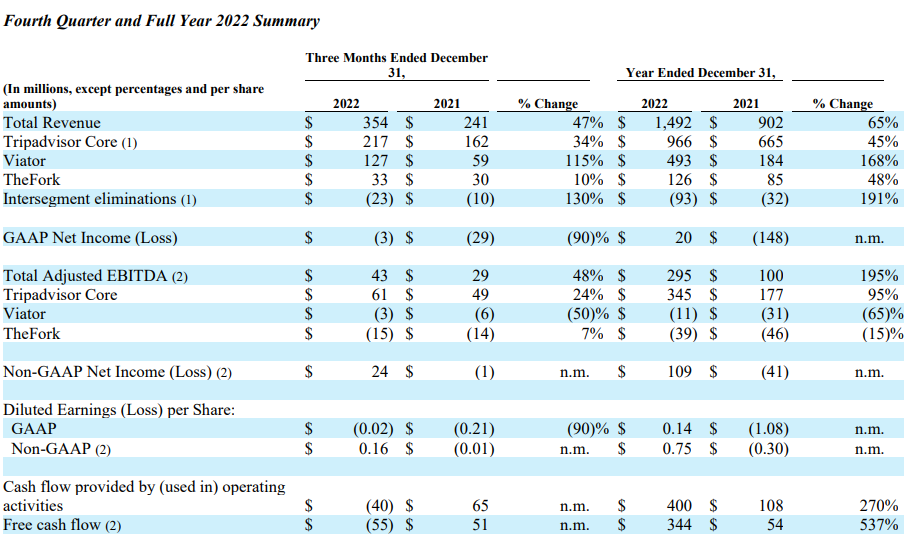

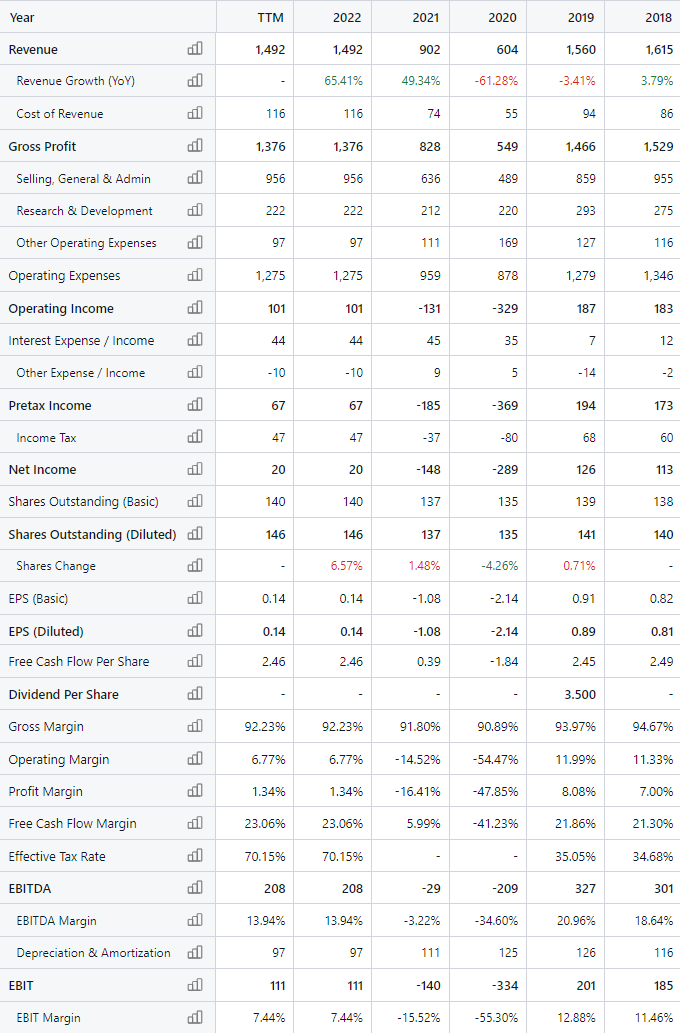

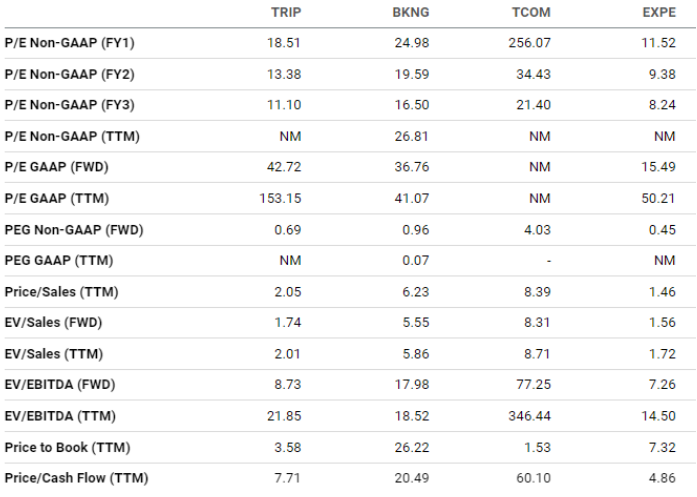

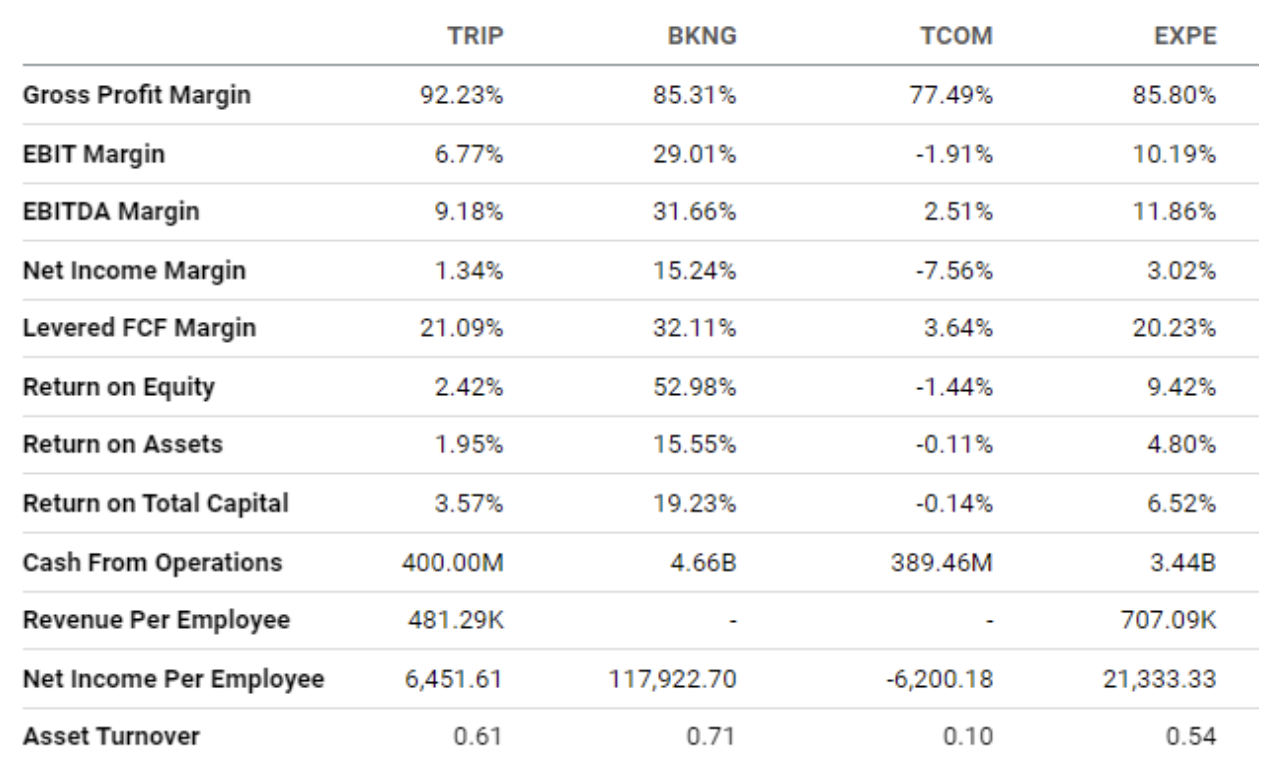

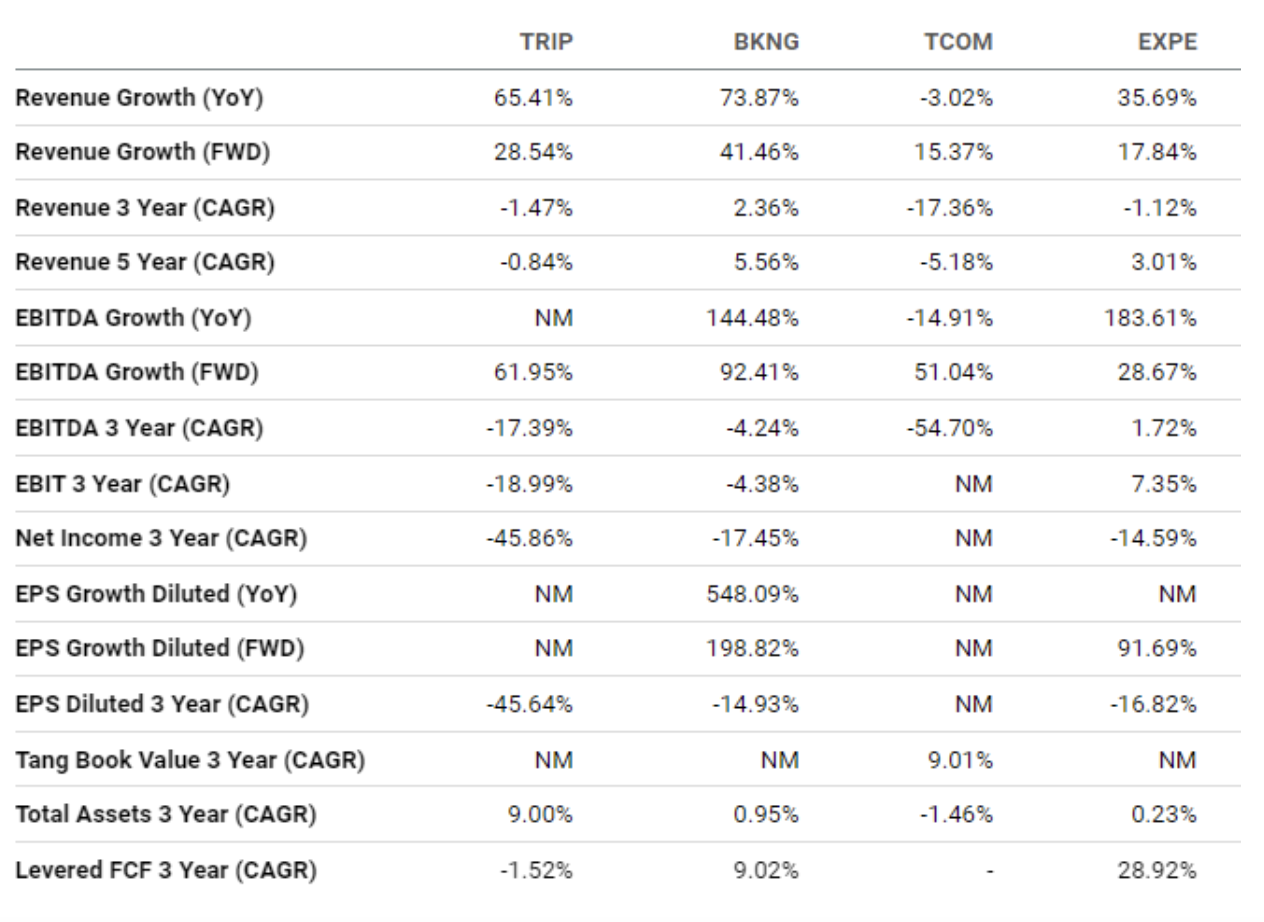

Hotel rooms are limited. Restaurant reservations are scarce. The last thing anyone wants to do is pay through the nose for a bad experience. That’s where Tripadvisor (TRIP) comes in. The company helps consumers research and book travel, leisure, and entertainment experiences. In 2014, Tripadvisor acquired both Viator, an online platform for booking tours, activities, and attractions around the world, and TheFork, an online platform for restaurant reservation and discovery. What caught our eye now was the 312% surge in searches by financial pros last week off the company’s earnings announcement. While search volume typically climbs around earnings, Tripadvisor landed in the top spot among all large-cap stocks last week. That plus a huge intraday reversal made us wonder whether this stock deserved the beating investors gave it. Turns out, it did… Tripadvisor’s Business Think of Tripadvisor as the Yelp of travel and entertainment. It’s headquartered in Needham, Massachusetts, and was founded in 2002. Users flock to Tripadvisor’s website for information and reviews on hotels, restaurants, flights, and vacation rentals. The company’s database includes more than 859 million reviews and opinions and covers more than 8.6 million accommodations, restaurants, experiences, and airlines. Tripadvisor also offers online booking for hotels, vacation rentals, flights, and restaurants. Plus, it offers a range of travel-related content and advice, including travel forums and destination guides. It generates revenues from clicks to companies that advertise on the site and from bookings users complete on the platform. The company segments its business into Tripadvisor Core, which includes Tripadvisor-branded hotels and experiences; Viator; and TheFork. Source: Tripadvisor Q4 and full-year 2022 results highlighted remarkable revenue growth of 47% and 65%, respectively. But only Tripadvisor Core was profitable. Viator and TheFork have continued their trends of operating losses since 2019. That said, Viator’s higher revenues put it just below profitability, while TheFork revenues and operating losses rose slightly. Current growth rates could make both profitable within a few years. Financials Source: Stock Analysis No one should be surprised that Tripadvisor’s revenues plunged during the pandemic. The company has since recovered more than 95% of 2019’s revenues. Unfortunately, gross margins are slightly lower, at 92.2% over the last 12 months compared to 94% in 2019. Operating margin has also taken a hit, dropping from 12.0% to 6.8%. This comes as selling, general, and administrative costs jumped from 55.0% to 63.5% of revenues, largely due to expenses related to business expansion into new markets and territories, growing Tripadvisor’s restaurant and attraction verticals, and doubling its investment in TV advertising. But we can’t deny the growth the company has achieved. And Tripadvisor exhibits economies of scale. So its growth investment might pay off sooner rather than later. The company carries $800 million in long-term debt. But that’s only 2x its current annual operating cash flow. And with TRIP’s quick and current ratios both around 2.4x, investors aren’t too concerned about liquidity or debt burdens. Valuation Source: Seeking Alpha Interestingly, Tripadvisor doesn’t have any direct competitors. In fact, Expedia Group (EXPE) and Booking Holdings (BKNG) (which owns Booking.com) are both customers of Tripadvisor. Nonetheless, along with Trip.com (TCOM), they make good peers for comparison. Notably, the trailing-12-month price-to-earnings ratios of all four companies are horrendous. TRIP at 153.2x is second-worst to TCOM, which didn’t turn a profit last year. BKNG and EXPE fared only slightly better at 41.1x and 50.2x, respectively. Next year’s forward P/E expectations don’t look that good either. EXPE is the lone exception at 15.5x. But on price-to-sales ratio, TRIP isn’t too bad at 2.1x, slightly worse than EXPE at 1.5x, but markedly better than BKNG at 6.2x and TCOM at 8.4x. Interestingly, TRIP’s price-to-cash-flow ratio is fairly cheap at 7.7x, although EXPE again comes in cheaper at 4.9x. BKNG and TCOM again don’t come anywhere close. Although EXPE is cheaper across many measures, there may be a reason investors are willing to pay a premium for TRIP… Profitability Source: Seeking Alpha TRIP has the best gross profit margin at 92.2%. But that doesn’t translate to EBIT or EBTIDA margins, where it comes in at 6.8% and 9.2%, beating only TCOM at -1.1% and 2.51%. BKNG runs an incredible EBIT margin of 29.0%, while EXPE is at a respectable 10.2%. In fact, BKNG holds the top spot for every profitability measure. But then again, it commands an incredible premium over its peers, probably why it’s trading near its all-time highs. TRIP generates $400 million in cash from operations, which is slightly better than TCOM. But BKNG and EXPE generate several billion dollars annually, making them behemoths compared to TRIP. Growth Source: Seeking Alpha Growth can make up for a lot when valuations suggest a stock is expensive. TRIP did nicely here both last year and looking forward, beating TCOM and EXPE. But even its 28.5% forward revenue growth is more than 10% lower than BKNG’s 41.5% expected growth. Our Opinion 4/10 Tripadvisor is likely to see a decent upside as the economy faces more Fed interest rate hikes. And TRIP stock is relatively cheap, trading near its all-time lows. But from a valuation standpoint, its only redeeming measure is its price-to-cash-flow ratio. Growth isn’t something to overpay for right now. TRIP is questionable as the best stock in its industry, an industry with an uncertain outlook. So we’d stay clear of this stock for now, until it either becomes cheaper or grows into its multiple. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |