|

Proprietary Data Insights Financial Pros Top Healthcare Services Stock Searches in the Last Month

|

|||||||||||||||||||||

|

Healthcare |

|

CVS Could Rule Healthcare |

|

Most Americans know CVS Health (CVS) as the drugstore chain with over 9,600 stores in the U.S., making it the largest such player in the country. But for anyone with Aetna insurance, it’s become a bigger part of their lives. That’s because CVS leapt into the broader healthcare space in December 2018, acquiring Aetna for nearly $70 billion. Since then, the company added Signify Health to its portfolio for $8 billion in September 2022, expanding its reach into managed service organizations and home health. According to Signify, it’s a healthcare platform that “leverages advanced analytics, technology, and nationwide healthcare provider networks to create and power value-based payment programs.” More recently, CVS announced plans to acquire Oak Street Health, a primary care provider, for $10.6 billion as it looks to integrate its business vertically. The problem is Oak Street isn’t profitable. And CVS’ long-term debt ballooned from $11.6 billion in 2014 to $26.2 billion the following year and $70.8 billion by 2017 before dropping to $49.1 billion today. Yet its interest expenses are expected to hit $2.2 billion against $13 billion in operational cash flow this year. It all boils down to a difficult question: Can CVS add value with its acquisitions? This is a question on many investors’ minds. According to our proprietary Trackstar database, financial pros searched for the stock 4x more than they searched for Walgreens Boot Alliance (WBA) and just less than UnitedHealth Group (UNH). CVS stock is down almost 25% from its all-time highs in early 2022. It currently trades at just 10.9x forward earnings and 8.5x forward cash. Plus, it pays a nice 2.7% dividend yield. So we figured it’s worth digging into. CVS’ Business The smallest state in the union, Rhode Island, is the headquarters of CVS Health (formerly CVS Caremark), one of the largest companies in the U.S. Now considered a “pharmacy innovation” company, CVS is more than a drug retailer. Its purchase of Aetna started it on its way to being a healthcare behemoth. Today, the company reports in three distinct segments:

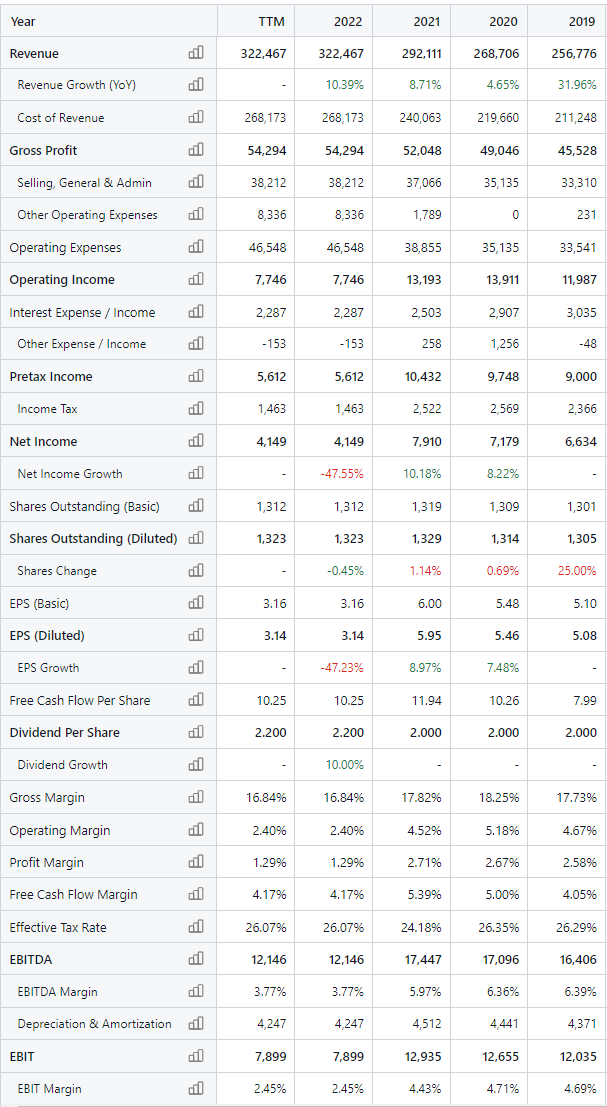

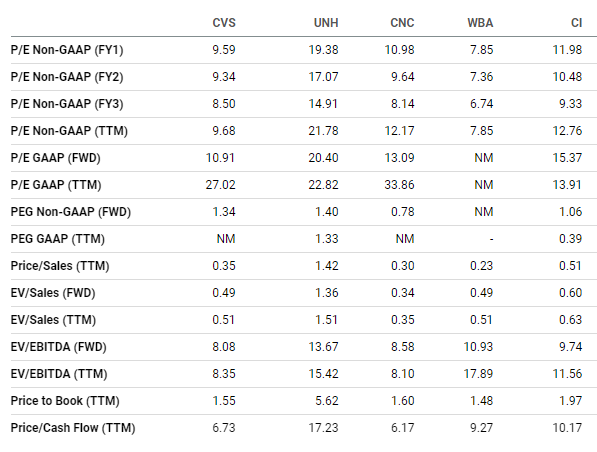

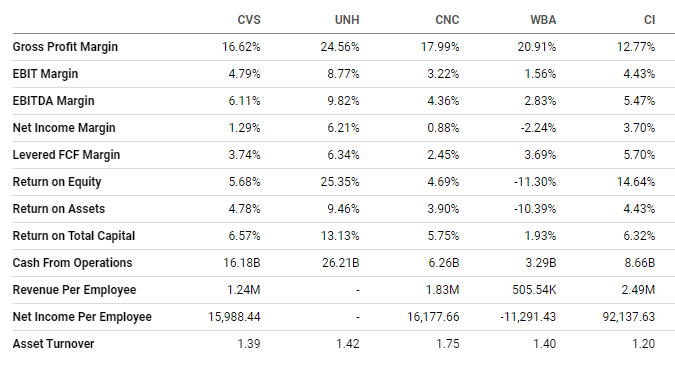

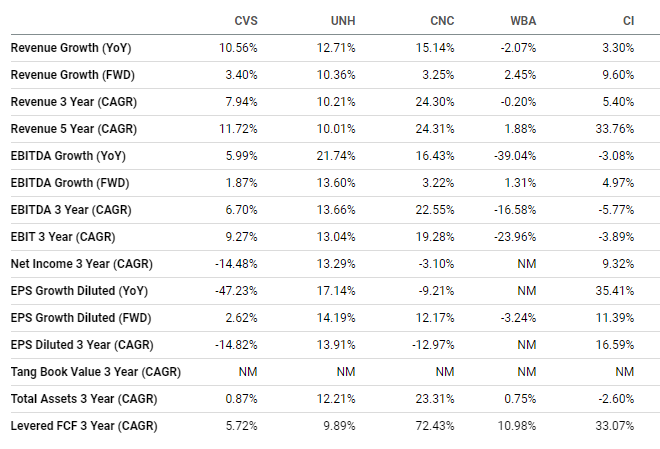

In CVS’ latest quarterly report, management said it expects 2023 earnings per share to land at $8.70 to $8.90 compared to $8.69 in 2022, with single-digit growth across its segments. Management forecasts $12.5 to $13.5 billion in operational cash flow with capital expenditures between $2.8 and $3.0 billion. The company’s focus on Medicare patients is in a high-growth area. CVS operates 169 clinics in 21 states, and by 2026, it expects to reach 300 sites, with each clinic generating about $7 million of EBITDA, generating a combined $2 billion annual EBITDA. Not bad for a three-year payback. The problem is Oak Street’s 2021 operating income was -$411 million, and its adjusted EBITDA is expected to be -$290 million. Plus, Signify Health reported a net loss of $540 million across the first nine months of last year. Nonetheless, CVS has shown a remarkable ability to deliver on its vision. And while these acquisitions may be a bit risky, the potential payouts are huge. Financials Source: Stock Analysis CVS revenues exploded upon the Aetna acquisition. Interestingly, margins have been fairly stable, with gross margin at 16.6% today versus 16.3% in 2016, and operating margin at 4.8% today versus 6.0% in 2016. The company holds a massive $15.7 billion in cash with $27.3 billion in other receivables along with $19.1 billion in inventory, with total current assets at $65.7 billion. Long-term assets we’d classify as tangible (investments and property, plant, and equipment) amount to $40 billion . That compares to $69.8 billion in current liabilities and $50.5 billion in long-term debt. On balance, that’s not terrible. And with net free cash flow of about $10 billion each year, CVS has a good chunk to pay down its debt. Its current ratio of 0.9x is adequate. But its quick ratio of 0.6x is concerning. Valuation Source: Seeking Alpha CVS straddles the line between insurer and drug store. To that end, we can’t create an apples-to-apples comparison. But it’s worth highlighting a few key points based on its closest peers. CVS’ 10.9x forward P/E is leaps and bounds better than every company we put it up against. And its price-to-cash-flow ratio of 6.7x is fantastic, second to Centene (CNC) at 6.2x. Keep in mind CVS trades at just 8.5x this year’s projected operating cash flow. Profitability Source: Seeking Alpha It was interesting to see that CVS’ 16.6% gross profit margin was actually lowest after Cigna (CI) at 12.8%. But CVS’ EBITDA margin of 6.1% was the second-highest, behind only UNH at 9.8%, as was its 4.8% EBIT margin compared to UNH’s 8.8%. CVS’ net income margin was pretty low at 1.3%, putting it in the middle of the pack. WBA was at -2.2%, CNC 0.9%, UNH 6.2%, and CI 3.7%. Interestingly, CVS’ return on equity of 5.7%, return on assets of 4.8%, and return on total capital of 6.6% each landed in the middle of the group. Growth Source: Seeking Alpha CVS managed healthy growth in 2022, though it still landed in the middle of the pack. It’s in the same spot for this year’s projected growth. It still had a respectable three-year 7.9% average annual growth. Our Opinion 10/10 There’s a lot that could go wrong with CVS’ recent acquisitions. But we don’t see a huge downside. At worst, the companies never become profitable, and CVS limps along at $10 billion in operating cash flow assuming no changes. That pays for the debt in less than a decade. The upside potential, though, could add another $2 billion to the company’s bottom line, which is nothing to sneeze at. And there’s a moonshot that could turn CVS into the largest integrated healthcare provider in the U.S. with a business model that dominates the marketplace. For these reasons, we rate this stock a great buy now. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |