|

Proprietary Data Insights Top Tech Stock Searches This Month

|

|||||||||||||||||||||

|

Suddenly, everybody from CNN to The Today Show is sounding the alarm on the divergence between personal savings and consumer debt, particularly credit card balances. Where were they last spring? At The Juice, we rarely congratulate ourselves. But if we may bask in our prescience for a second, we’ll follow the self-congratulations with good news amid the little-too-late hysteria, plus how to handle scary macroeconomic headlines in your personal finance and as an investor. The comparison between last spring and today is stark. On April 19, 2022, we said:

On May 9, 2022, we followed up:

Here’s the government’s latest on Americans’ credit card debt:

Amid this bad news on debt, there might be some good news on savings. Scroll with us for that good news and how to consider your specific situation. |

|||||||||||||||||||||

|

Debt Versus Savings |

Don’t Say The Juice Didn’t Warn You |

Key Takeaways:

One reason we called out the mainstream media on their crisis call is they’re late to the party. Then, when they finally show up (without a bottle of wine!), they rarely, if ever, report the glimmer of hope alongside the hysteria. But here’s that good news: As credit card debt climbs, personal savings has actually improved in recent months. Personal savings refers to how much people save as a percentage of their disposable income. Here’s the U.S.’ trend on that figure since summer:

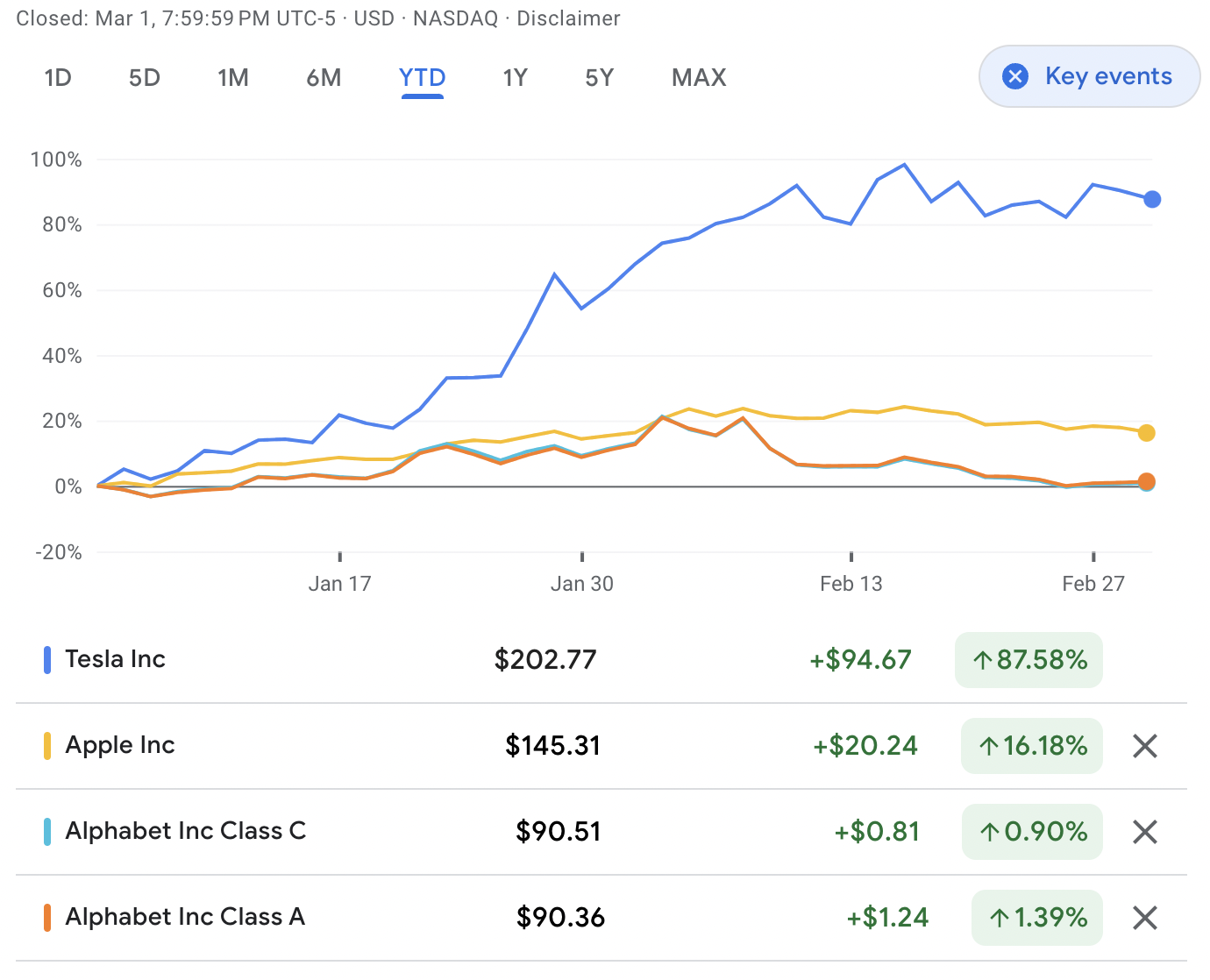

While still below the pandemic highs by a relative mile, this is encouraging. The overall amount of money people have saved has also increased, from $506.3 billion in June 2022 to $918.8 billion in January 2023. For the record, The Juice has been using data from the Bureau of Economic Analysis all along. What does this all mean for you? The continued upsurge in debt coupled with an apparent rebound in savings could mean some households are tightening things up. Stockpiling cash to keep credit card balances in check. Maybe more likely, it means some households are hurting as others thrive. A thesis we’ve floated regularly over the past year. The thriving households have relatively high earnings, with cash to save and spend. They help drive consumer spending, not to mention inflation. If you’re among those struggling, the remedy to your situation is equally as obvious as it is painful. Cut out unnecessary spending, work to pay down high-interest credit card debt first, and keep enough savings on hand to cover an emergency and/or loss of income. If you’re among those crushing it, continue to pad your savings and seek opportunities in the stock market. Speaking of… Remember how down everybody was last year as Elon Musk was losing money? While Tesla (TSLA) is down roughly 31% over the last year, it’s up more than 87% in 2023. That opportunity might be ongoing. Rest assured, Musk is – once again – the richest person in the world. If you’re not into TSLA, consider poor Google (GOOG, GOOGL) as it stagnates relative to TSLA and Apple (AAPL). Source: Google Finance But before you dive into Google, consider a blue-chip alternative our sister newsletter, The Spill, recently wrote about. It could also be the case that you’re doing super well financially but still internalize the broad headlines. You worry the bottom might fall out on your situation. So you hunker down. There’s probably never anything wrong with this, whether you’re building a nest egg to eventually spend or send into the stock market. The Bottom Line: To each their own. Nobody can or should judge you for how you manage your money, particularly during especially uncertain times with seemingly contradictory information. However it goes down, The Juice is here with nuggets of personal finance advice and investing ideas you can adapt to your circumstances. |

|

News & Insights |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |