|

Proprietary Data Insights Financial Pros Top Oil & Gas Exploration Stock Searches Last Month

|

|||||||||||||||||||||

|

Energy |

|

Buy Devon’s Pullback |

|

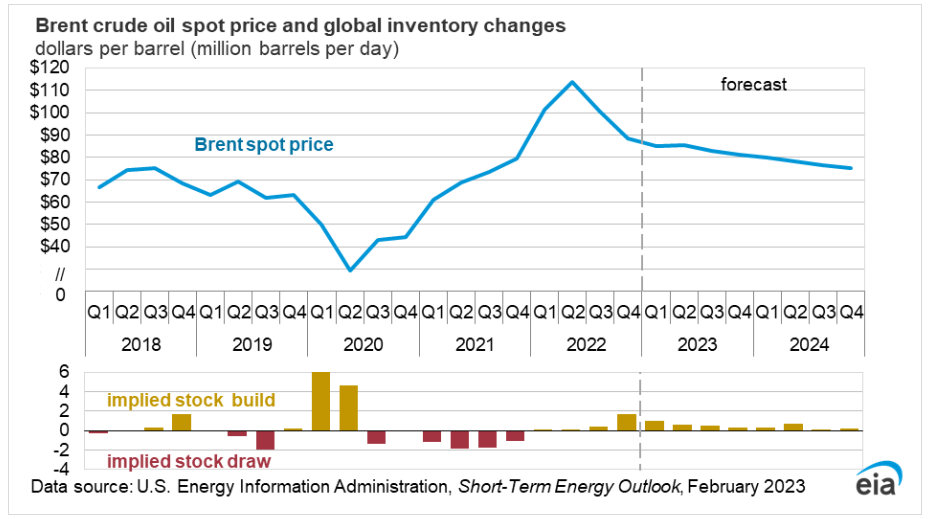

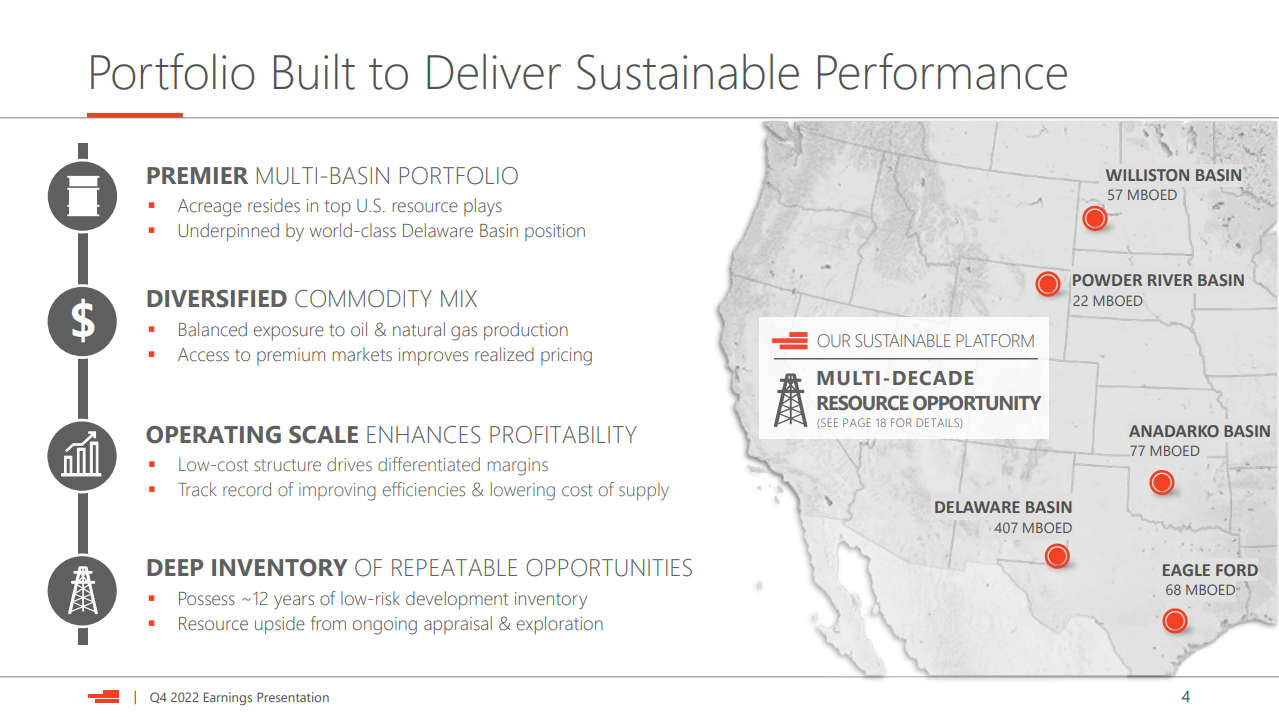

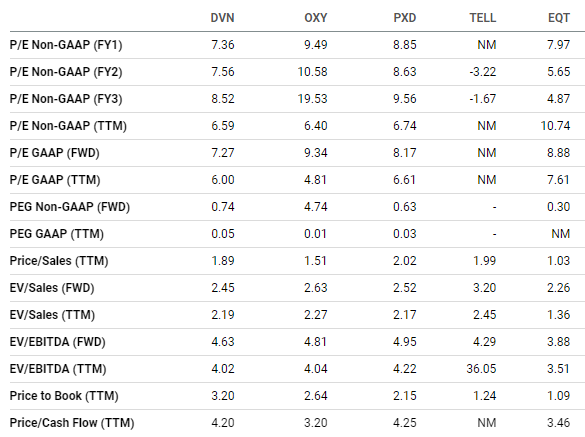

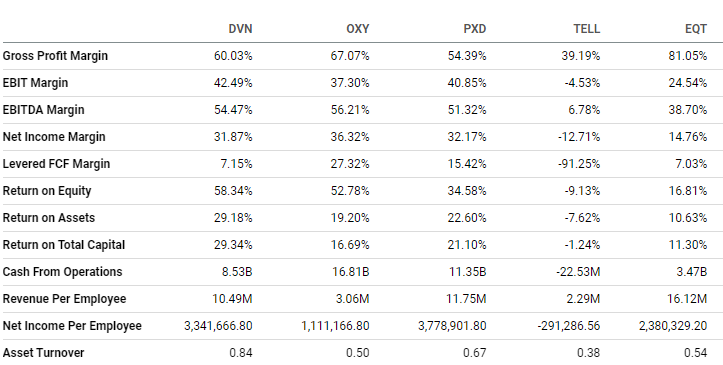

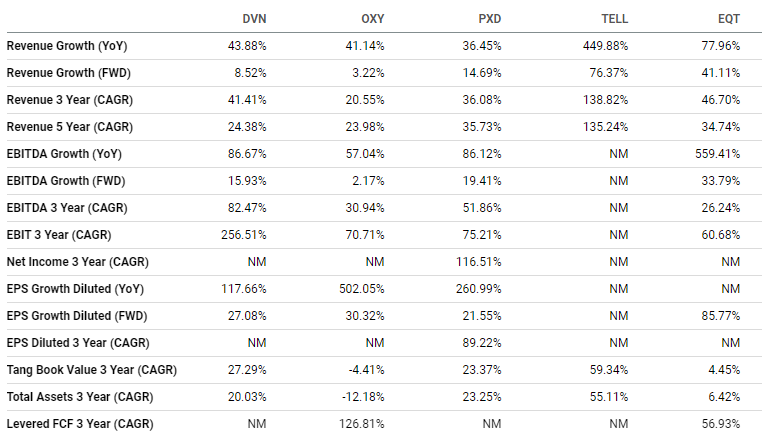

Here’s a head-scratcher… Natural gas, which last winter was so scarce Europe expected factories to shut down, is now trading at multiyear lows. Crude oil, on the other hand, is still holding well above pre-pandemic levels. It all comes down to basic economics – supply and demand. The following graphic from the U.S. Energy Information Administration (EIA) shows oil prices with implied stock builds and draws. The same agency said it expects 2023 oil demand to be 100.1 million barrels per day with supply sitting at 101.1 million per day. That’s driving the forecasted slight inventory builds on the graph. Oil and gas exploration companies like Devon Energy (DVN) have benefited from high crude prices, with DVN stock climbing to levels it hasn’t been at since 2014. Energy as a whole outperformed the general market last year and will likely do so again this year. Though DVN was financial pros’ top oil and gas exploration stock search in February, according to our proprietary Trackstar data, search volume for the stock and the industry is down overall. And DVN shares are down almost 30% from their 2022 highs. As you’ll see, this pullback could be a fantastic buying opportunity. Devon Energy’s Business Devon Energy drills oil and gas to send to refiners. That’s why around 70% of its revenues are tied to oil prices. In 2019, it sold off most of its Canadian operations. A year later, it sold all its Barnett Shale (northern Texas) assets. The company’s main footprint is in the Delaware Basin, Eagle Ford, Anadarko Basin, Williston Basin, and Powder River Basin. These spots run north from Texas to the top of the U.S. Source: Devon Energy Q4 presentation Financials Source: Stock Analysis Oil prices plummeted in 2016 as shale production took off in the U.S. Until the pandemic ended, the world was awash in oil. But lockdowns led to a huge inventory and supply shortage, sending oil prices higher than they’d been in nearly a decade. Since then, prices have stabilized, though production isn’t back at its former levels. Higher costs of investments, uncertainty around the Chinese economy, and geopolitical tensions have changed the landscape. But Devon Energy did a remarkable job of delivering profits to its shareholders. Current long-term debt sits at $6.2 billion, a modest increase from $4.3 billion in 2019. It repurchased $804 million in shares last year and $634 million in 2021. Plus, the company paid $5.17 per share in dividends last year, equivalent to a nearly 10% yield. Valuation Source: Seeking Alpha With its recent pullback, Devon Energy became even more of a value. Its forward P/E ratio of 7.27x beats all its peers, with Pioneer Natural Resources (PXD) second at 8.2x, EQT (EQT) at 8.9x, and Occidental Petroleum (OXY) at 9.3x. DVN falls a bit short in price-to-sales ratio at 1.9x. This is higher than PXD and Tellurian (TELL), which are both at 2.0x. But OXY is cheaper at 1.5x, and EQT trades at a paltry 1.0x. Interestingly, DVN trades at 4.2x cash, higher than PXD and EQT. TELL had no cash flow last year, and PXD trades at 4.3x cash. Profitability Source: Seeking Alpha DVN does well in profitability with a gross margin of 60.0%. But this can change dramatically based on oil prices and contracts. Nonetheless, DVN’s in the middle of the pack compared to its peers. We like its healthy EBIT margin of 42.5%, beating all its peers, including PXD’s respectable 40.9%. DVN also boasts the highest return on equity at 58.3%, return on assets at 29.2%, and return on total capital at 29.3%. Growth Source: Seeking Alpha DVN’s growth outlook should slow substantially in 2023. It’s expected to increase revenues only 8.5%, the second-worst to OXY at 3.2%. Its other peers are forecast to do much better, with PXD at 14.7%, TELL at 76.4%, and EQT at 46.7%. But EBIT three-year average growth for DVN is at 256.5%. None of the others come close, even with OXY, PXD, and EQT hitting an impressive 70.7%, 75.2%, and 60.7%, respectively.

Our Opinion 10/10 DVN trades at 4.5x forward operating cash flow, and we can’t overlook how cheap it is when you consider its tangible dividend payments, fantastic return on investments, and overall performance. True, oil prices might come down from current levels. But they could just as easily rise. There’s too much uncertainty to say where 2023 will land. But with oil demand rising every year and investments in supply restricted, we like Devon Energy for the long haul. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |