|

Proprietary Data Insights Financial Pros Top Industrial Conglomerates Stock Searches Last Month

|

|||||||||||||||||||||

|

Industrials |

What’s Left of GE Isn’t Great |

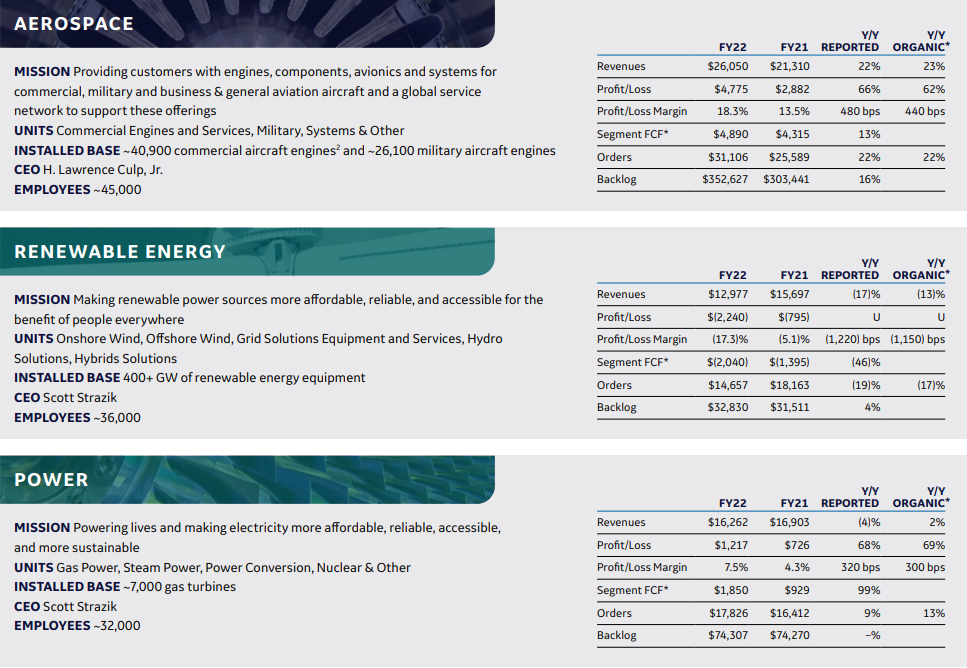

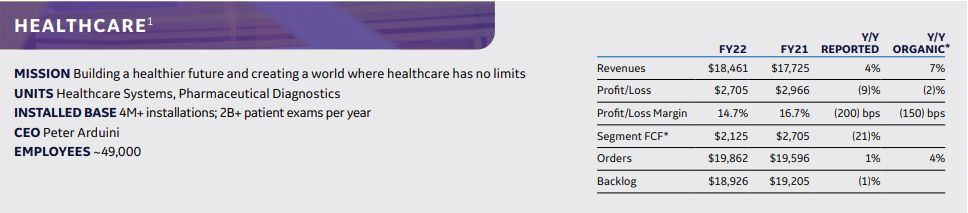

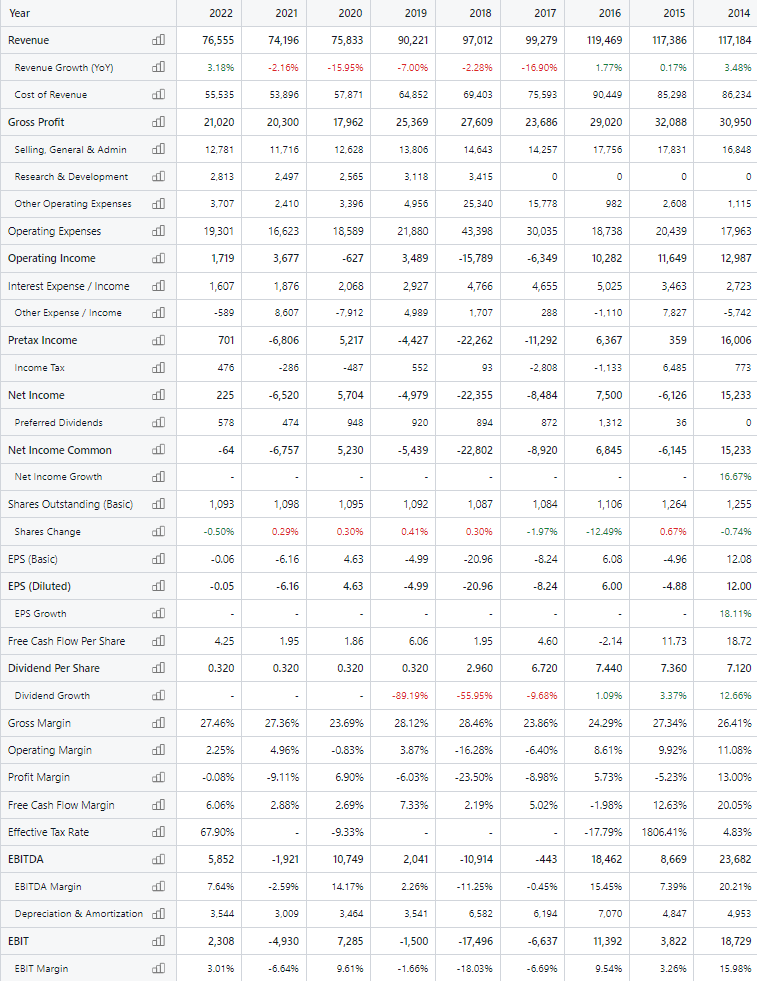

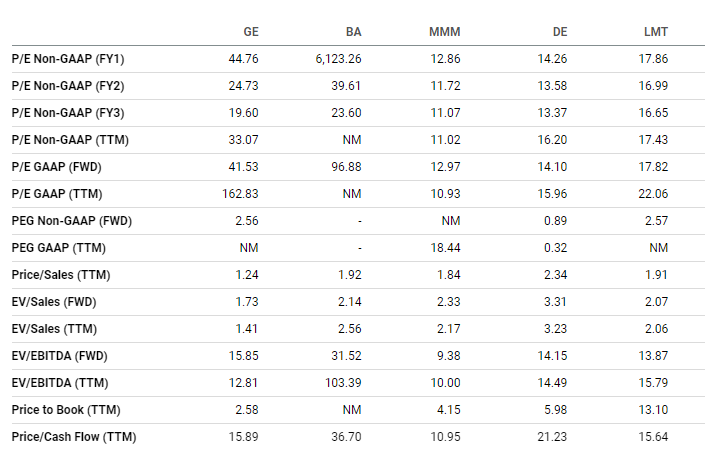

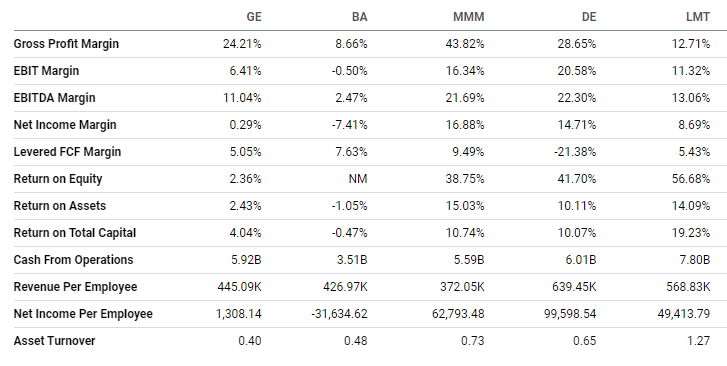

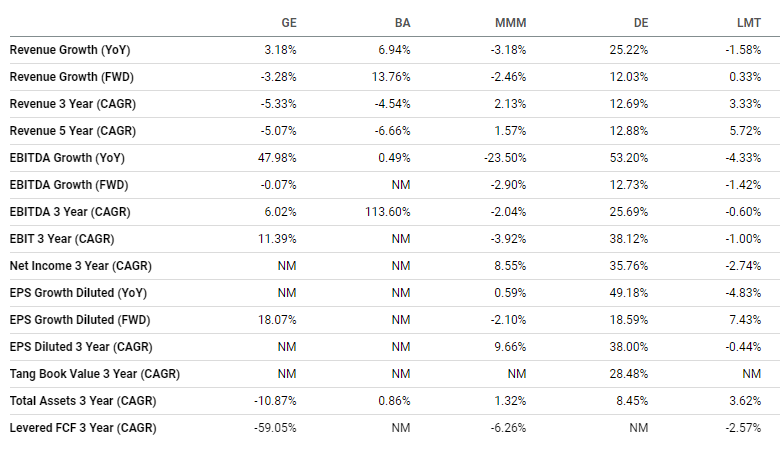

General Electric (GE) spun off its profitable and growing healthcare division, GE HealthCare Technologies (GEHC), in January. That leaves GE with a burgeoning aerospace segment at the mercy of airline travel, an adequate power business, and a poor-performing renewable energy segment. When we saw GE at the top of financial pros’ February conglomerate stock searches in our proprietary Trackstar database, we were surprised to say the least. The company looked overvalued and seemed to lack good prospects. Did these financial pros know something we didn’t? General Electric’s Business For over 100 years, GE has been a recognized leader in the industrial sector. From light bulbs to energy production, aircraft engines, and healthcare, GE is a manufacturing powerhouse. CEO Jack Welch took the helm from 1981 to 2001, transforming the company into a global conglomerate. During his tenure, GE’s share price went from below $20 to over $360 in 2000. His foray into financial products under GE Finance was profitable and dangerous, leading to the company’s downfall during the 2008 financial crisis. While GE survived, it never fully recovered. Today, the company has three units: aerospace, renewable energy, and power. Source: GE 2022 Annual Report In January, its healthcare division spun off into a separate company. GE will retain 19.9% of GEHC stock. Source: GE 2022 Annual Report Financials Source: Stock Analysis Removing GE Healthcare from the financials leaves GE with annual revenues of $58.1 billion and an operating loss of $1.3 billion. While aerospace and power did nicely, renewable energy saw a sizable increase in losses, while free cash flow eroded from -$1.4 billion in 2021 to -$2.0 billion last year. Fortunately, Q3’s Inflation Reduction Act introduces and extends renewable energy tax credits for 10 years. GE’s wind business took a significant hit as competition increased in 2022. In Europe, the company is falling further behind despite heavy demand. All segments, including renewables, are fighting inflationary pressures. It’s worth noting the best-performing segment, aerospace, is riding on the back of a revitalized air travel industry. Many don’t expect this vitality to continue much longer. GE HealthCare’s spinoff pulled away $4.0 billion in pension liabilities while adding $1.5 billion in cash to GE. Prior to the split, the current ratio was 1.2x and the quick ratio 0.8x. The additional cash will help improve both metrics. Free cash flow (after capital expenditures) is $2.6 billion without HealthCare. Valuation Source: Seeking Alpha It’s hard to precisely determine the effect of the healthcare divestiture on valuation, profitability, and growth. We do know it boosted every category. So when we see a P/E GAAP forward ratio of 41.5x, we know that without healthcare, it’ll be worse. While Boeing (BA) isn’t any better, 3M (MMM), Deere (DE), and Lockheed Martin (LMT) are more attractive, with forward P/E ratios of 13.0x, 14.1x, and 17.8x, respectively. Interestingly, GE’s price-to-cash-flow ratio isn’t bad at 15.9x. But we know operating cash flow will drop by at least healthcare’s free cash flow. That puts the adjusted price-to-cash-flow ratio at 16.9x, in the middle of GE’s peers. Profitability Source: Seeking Alpha We expect GE’s profitability to decline without healthcare in its reporting. But we can’t yet calculate all the profitability metrics. Nonetheless, it’s worth noting that except for BA, GE’s peers had better gross and EBIT margins. Growth Source: Seeking Alpha Similarly, we know GE’s growth won’t be as robust without the healthcare segment. And with next year’s outlook expecting a revenue decline of 3.3%, GE is in the worst position among its peers. Our Opinion 2/10 GEHC may be a great stock. GE is not. GE is far too expensive for a company that’s unable to capitalize on megatrends like renewable energy. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |