|

Proprietary Data Insights Financial Pros Top Fast Food Stock Searches Last Month

|

|||||||||||||||||||||

|

Consumer Cyclical |

Arches Made of Gold or Mold? |

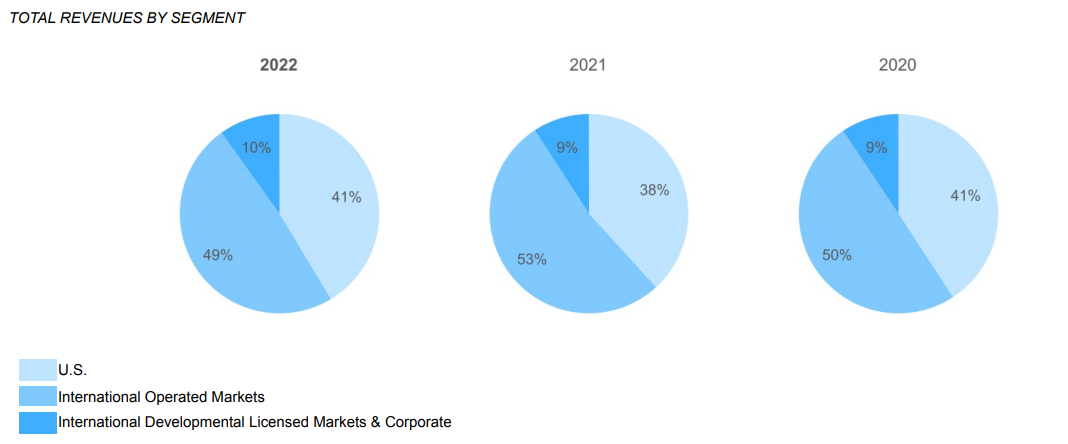

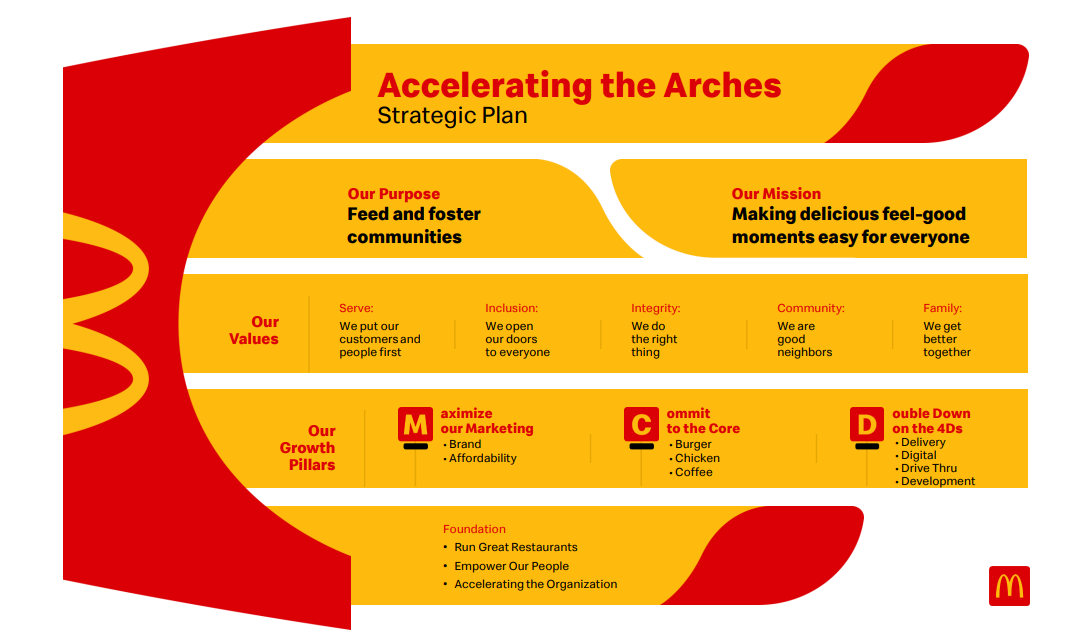

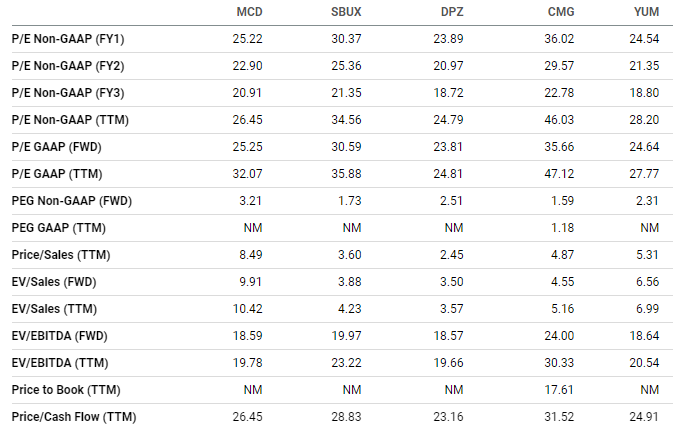

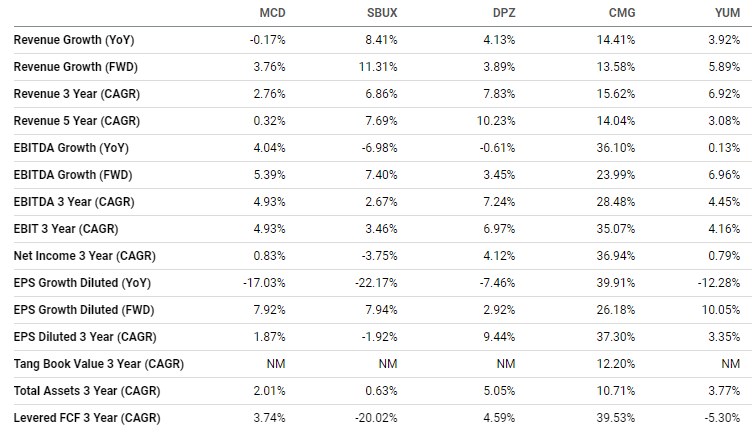

2022 wasn’t good for McDonald’s (MCD). Inflation ate into profits, and Russia’s war with Ukraine made the Golden Arches exit Russia. Yet in June, our proprietary Trackstar database highlighted financial pros’ surging searches for the stock, and we looked into the company’s business model and realized many investors were overlooking MCD’s value. We rated the stock an 8/10. About eight months later, our pick is up about 11% including dividends, nearly double the gain of the S&P 500 with dividends. Then last month, we took an updated look and lowered our rating to a 7/10. Interestingly, the company’s current valuation isn’t that different from what it was in our June evaluation nor that of last month. But the share price is 6.5% off its all-time highs, though financial pros’ searches have tanked in the past 30 days. This made us wonder if we should further update our take. McDonald’s Business 95% of McDonald’s 40,275 stores are franchises. It’s a unique strategy that helped the company navigate expansion into more than 100 countries and limit the fallout from leaving Russia. Company-operated restaurants make up 38% of sales, with franchises making up the rest. The crazy part is that its owned-and-operated restaurants run a 15.6% gross margin, while franchise restaurants are at 83.3%. However, the capital-light franchise model means no asset ownership, so most of the $38.2 billion in property, plant, and equipment (PP&E) on MCD’s balance sheet is attributable to company-operated restaurants. Most people don’t realize how global McDonald’s has become. In fact, the U.S. accounts for only 41% of its total revenues. Source: MCD 2022 Q4 earnings In 2019, the company implemented its Accelerating the Arches plan, which consists of three growth pillars: maximizing marketing, committing to core products, and doubling down on the “4Ds” – delivery, digital, drive-thru, and development. Source: McDonald’s This year, McDonald’s plans to open 100 stores in the U.S while closing 80, open 300 owned internationally while closing 90, and opening 1,500 franchised locations internationally while closing 230. That’s a total of 1,900 openings and 400 closings, a net addition of 1,500 stores. Financials Source: Stock Analysis McDonald’s has struggled to drive sales growth. Revenues slid from $27.4 billion in 2014 every year until 2019, when they grew just 0.5%. After a COVID-induced slide in 2020, revenues rebounded 20.1% in 2021, pushing the company’s sales to levels it hadn’t hit since 2016. Many investors have chided the company for a lack of innovation. Even its Accelerate the Arches strategy doesn’t inspire confidence. But McDonald’s generates a sizable amount of cash, $7.4 billion from operations and $5.3 billion in free cash flow. The company has a lot of long-term debt, $36.0 billion. But its $38.2 billion in PP&E more than matches that. With a current ratio of 1.4x and a quick ratio of 1.2x, McDonald’s has plenty of liquidity to meet its financial obligations, including its healthy 2.3% dividend yield. Valuation Source: Seeking Alpha The valuation comparisons here are fascinating because of how close many of them are. For instance, the forward-looking P/E ratio for MCD is 25.3x. Starbucks (SBUX) and Chipotle Mexican Grill (CMG) are a bit higher at 30.6x and 35.7x, respectively. Domino’s Pizza (DPZ) and Yum! Brands (YUM) are just below at 23.8x and 24.5x. The price-to-cash-flow ratios are all relatively close too. MCD is at 26.5x, CMG is on the high end at 31.5x, and DPZ rounds out the low end at 23.2x. Where we see an interesting gap is in the price-to-sales ratio. There, MCD at 8.5x is markedly higher than its peers, with YUM the second-most expensive at 5.3x. Growth Source: Seeking Alpha Unsurprisingly, CMG has the highest growth, whether you’re looking at the last year, at the last five years, or forward. MCD’s growth hasn’t been that impressive. The company expected to grow revenues 8.4% last year but came in flat. Next year’s forecast calls for 3.8% growth, which isn’t great. Its five-year average growth rate is a measly 0.3%. YUM is the second-worst at 3.1%. SBUX is more than double that at 7.7%, DPZ is at 10.2%, and CMG is at a whopping 14.0%. MCD also comes in second to last for EPS growth both last year and over the last three. Even its 4.9% EBIT growth is at the lower end. Profitability Source: Seeking Alpha Despite the growth problems, MCD smokes its peers in profitability. It beats every one in gross, EBIT, EBITDA, and net income margins. Its return on assets of 16.4% puts it in the middle of the pack, while its 14.8% return on total capital is closer to the low end. But it generates nearly twice the operational cash flow as SBUX, the closest competitor. Our Opinion 6/10 We downgraded our opinion of McDonald’s for a few reasons. First, interest rates continue to climb and are likely to keep doing so. We want a better value than last year, not the same, especially with even less growth. Second, the “growth” plan isn’t that inspiring, especially when forecasts show it’ll give the company only a 3% boost next year. Lastly, MCD has a good amount of debt coming due in the next couple of years. It’s very likely its interest expenses will climb much higher than the $1.2 billion they’re at right now. None of this is to say McDonald’s isn’t a great company. Its stock just isn’t a great value. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |