Editor’s Note |

It’s Friday. Time to give you a stock pick from our sister newsletter, The Spill, so you can think about it over the weekend and maybe make a move Monday morning. While The Juice helps you be better with money across the board, The Spill focuses on stocks financial pros are researching and judges how good of buys they are. If you’re already sold, you can sign up for The Spill – for free – here. |

|

Proprietary Data Insights Financial Pros’ Top Engineering & Construction Stock Searches Last Month

|

|||||||||||||||||||||

|

Industrials |

PoWeR |

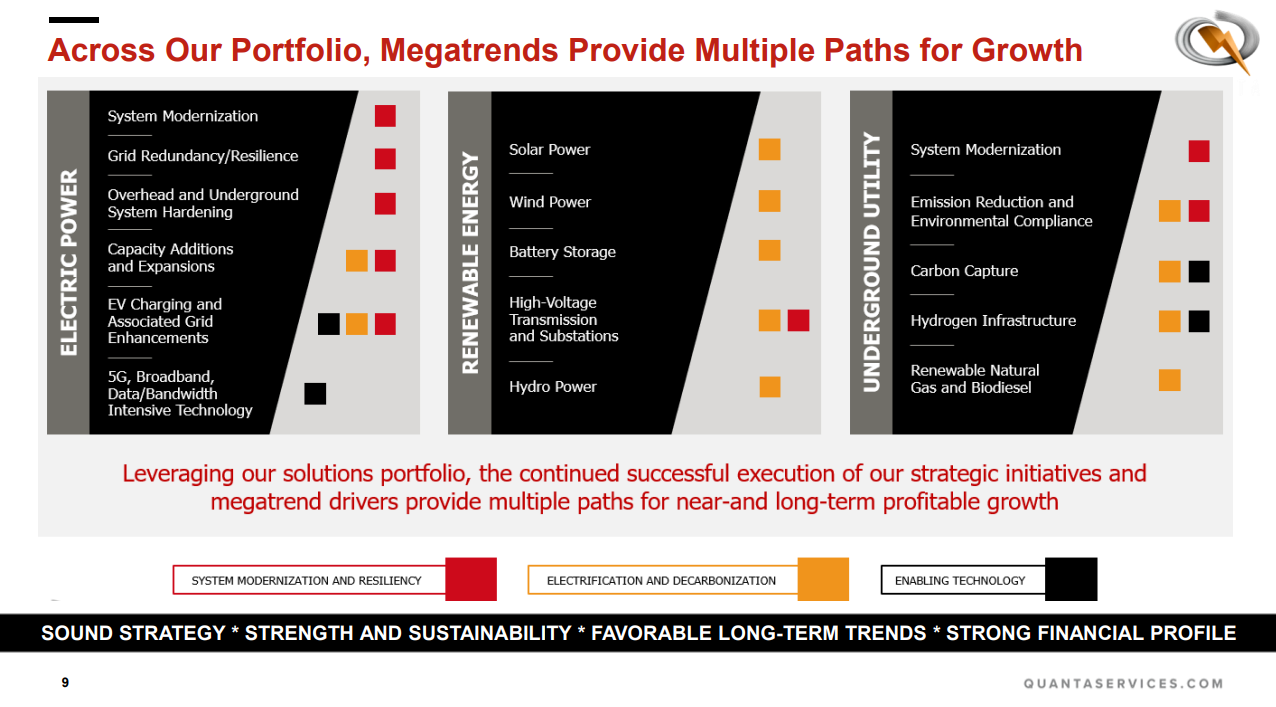

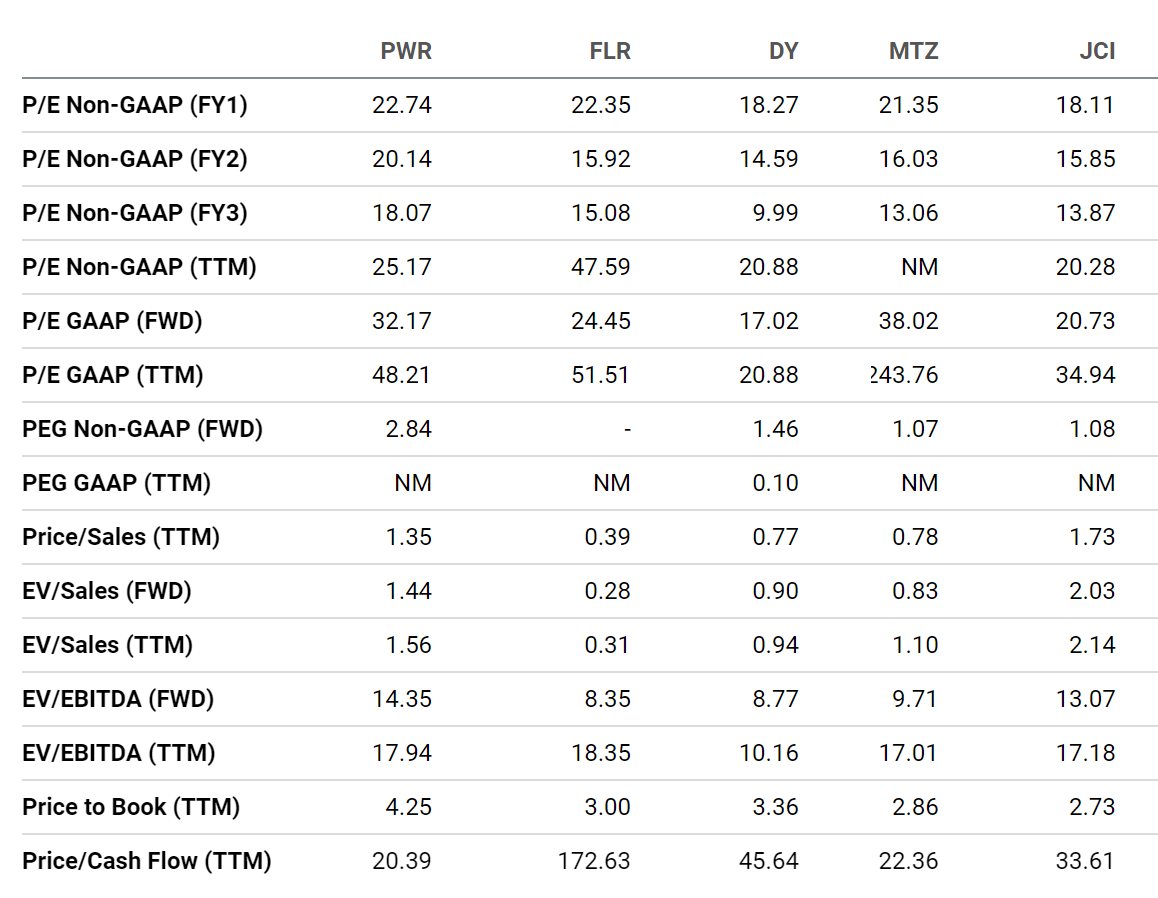

When Quanta Services (PWR) reported earnings on February 23, not many people were paying attention. According to our proprietary Trackstar database, financial pros’ searches for the engineering and construction stock were minimal. But when shares surged nearly 20%, folks noticed. The stock quickly became financial pros’ top search in its industry, with more than 6x the searches of the runner-up. Shares currently trade at $160, near their all-time highs. Demand for the electrical grid engineering group’s work has never been higher. Is that enough to make this stock worth your while? Quanta Services’ Business Quanta Services is one of the largest contractors serving the transmission and distribution sector of the North American electric utility industry. The company provides specialty contracting services to customers in the U.S., Canada, Australia, and other select international markets. It breaks its revenues into three segments that align with its customers: electric power, renewable energy, and underground utility. Source: Quanta Services 2023 presentation According to its latest earnings report, Quanta Services generated $6.34 per share on revenues of $17.1 billion for 2022, beating estimates of $6.33 and $16.9 billion, respectively. Plus, the company forecasted revenues of $18.4 to $18.9 billion for 2023. More importantly, cash from operations hit $1.13 billion in 2022, and Quanta expects this to rise to $1.20 to $1.40 billion in 2023. Financials Source: Stock Analysis Quanta Services’ revenues exploded last year as demand for its services skyrocketed a staggering 31.5%. While most margins remained largely intact, profit margins steadily dropped. Interest expenses jumped from $45.0 million in 2020 to $124.4 million in 2022. That’s when the company’s long-term debt climbed from $1.2 billion to $3.6 billion. Quanta used this money for a total of $2.5 billion in acquisitions it completed in 2021 to support its growing workload. While the debt is somewhat concerning, the company pays it off with its steadily growing cash from operations. A capital expenditure forecast of $400 million for 2023 and $588 million in acquisitions already this year might concern investors about liquidity. But a current ratio (current assets divided by current liabilities; the higher the ratio, the better financial position a company is in) of 1.6x should alleviate those concerns. Valuation Source: Seeking Alpha We weren’t surprised that PWR had a high forward price-to-earnings (P/E) ratio at 32.2x, especially given its acquisition-heavy strategy. What was unusual was seeing many of its peers with high P/E ratios. The lowest of the group in the table above, Dycom Industries (DY), a key player in undergrounding fiber optic and telecommunications cable, was still high at 17.0x. Yet except for PWR and Johnson Controls (JCI), all the companies have price-to-sales ratios below 1.0x. And PWR’s 1.4x and JCI’s 1.7x aren’t too bad. Importantly, PWR has the best price-to-cash-flow ratio, an important metric given the heavy debt these companies tend to take on to fund expansion. Profitability Source: Seeking Alpha Gross margins varied wildly, with PWR in the middle at 14.8%. We like the strong performance across the board for PWR on returns on equity, assets, and total capital. Only DY and JCI have similar performance. Growth Source: Seeking Alpha PWR stands out from its peers with above-average growth. Its 31.5% year-over-year (YoY) revenue growth dominated. MasTec (MTZ) was the closest at 23.0%. Even PWR’s three- and five-year average growth beat its peers’. The stock dominated on nearly every metric. And with the exception of YoY earnings-per-share growth, its metrics were respectable. Our Opinion 9/10 PWR stock has been going straight up since its 2020 lows. And those lows weren’t all that bad. Quanta Services is making multiple smaller acquisitions and doing fantastic at making them profitable. We’d buy here. But save some powder for if the stock has a healthy pullback. Recessionary talk could send it as low as $100. But that’s a great spot, in our opinion. To get content like this daily, sign up for The Spill for free here. |

|

News & Insights |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |