A brief excerpt:

In 2021, I pointed out that with the end of the foreclosure moratoriums, combined with the expiration of a large number of forbearance plans, we would see an increase in REOs in late 2022 and into 2023. However, this would NOT lead to a surge in foreclosures and significantly impact house prices (as happened following the housing bubble) since lending has been solid and most homeowners have substantial equity in their homes.

Last week, CoreLogic reported on homeowner equity: US Annual Home Equity Gains Cool Again in Q4 2022, CoreLogic Reports

The report shows that U.S. homeowners with mortgages (which account for roughly 63% of all properties) saw equity increase by 7.3% year over year, representing a collective gain of $1 trillion, for an average of $14,300 per borrower, since the fourth quarter of 2021.

With substantial equity, and low mortgage rates (mostly at a fixed rates), few homeowners will have financial difficulties.

…

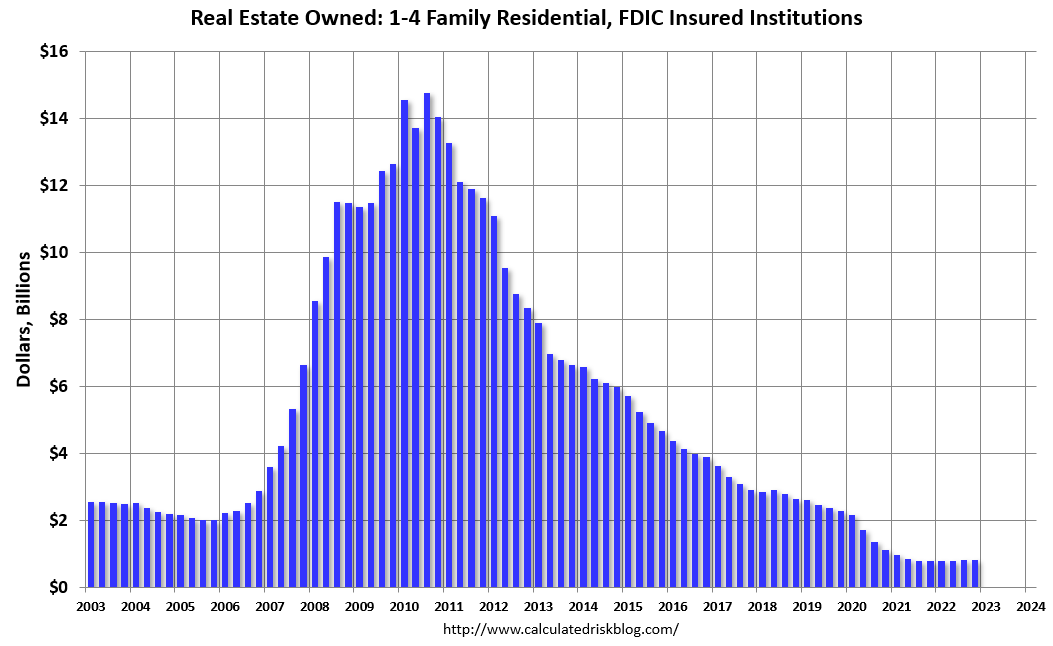

Here is some data on REOs through Q4 2022 …

…This graph shows the nominal dollar value of Residential REO for FDIC insured institutions. Note: The FDIC reports the dollar value and not the total number of REOs.

The dollar value of 1-4 family residential Real Estate Owned (REOs, foreclosure houses) increased from $818 million in Q3 2022 to $829 million in Q4 2022. This is increasing, but still very low.

…

The bottom line is there will be an increase in foreclosures in 2023 (from record low levels), but it will not be a huge wave of foreclosures as happened following the housing bubble. The distressed sales during the housing bust led to cascading price declines, and that will not happen this time.

There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/