Editor’s Note |

It’s Friday. Time to give you a stock pick (or three, this time!) from our sister newsletter, The Spill, so you can think about it over the weekend and maybe make a move Monday morning. While The Juice helps you be better with money across the board, The Spill focuses on stocks financial pros are researching and judges how good of buys they are. If you’re already sold, you can sign up for The Spill – for free – here. |

|

Proprietary Data Insights Financial Pros’ Top Regional Bank Stock Searches Last Month

|

|||||||||||||||||||||

3 Banks With More Than Luck on Their Side |

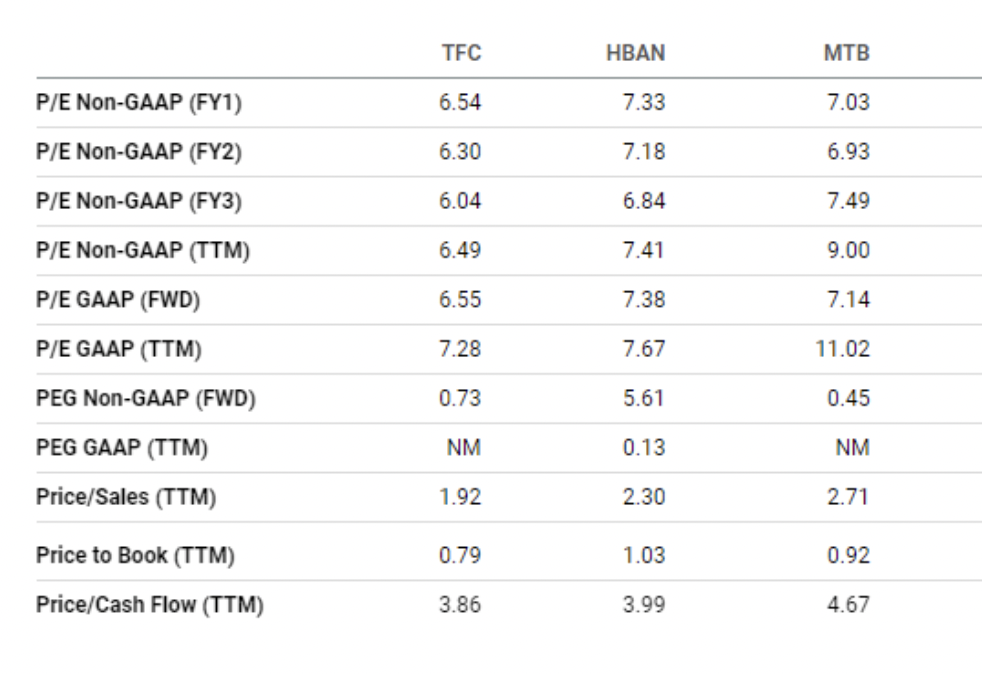

Banks are all anyone talks about these days. Rather than fight the trend, we’re giving you a trio of quality regional bank picks. We used our proprietary Trackstar data to find financial pros’ top regional bank stock searches last month. From that list, we came up with three with a lot of value that appear much safer than the rest: Truist Financial (TFC), M&T Bank (MTB), and Huntington Bancshares (HBAN). Why We Chose Them SVB Financial failed for three main reasons:

To combat the first point, we looked for banks with a larger percentage of deposits below the $250,000 FDIC-insured amount. SVB had 2.7% because most of its depositors were tech startups. M&T, Truist, and Huntington all do way better with 46.4%, 42.8%, and 41.1%, respectively. To address the second problem, we looked at the percentage of assets each bank has in securities. SVB had 55.4% of its assets in securities. M&T, Truist, and Huntington again are more conservative, with 12.2%, 23.5%, and 22.2%, respectively. They put much of their depositors’ money to work through loans. M&T favors commercial finance and commercial real estate loans, with around $42 billion in each, while it has roughly half the amount in consumer real estate and consumer loans, at $21 billion each. Truist holds $165 billion in loans for commercial clients, of which only a small portion is tied to real estate. Its consumer loans total $117 billion. Huntington is evenly split, with $42 billion in commercial loans, only $7 billion of which is tied to real estate, and another $38 billion in consumer loans, of which $12 billion is mortgage-related. And without getting into the nitty-gritty, all three banks do a fine job hedging to mitigate the effects of price movement. Truist has a market cap of $43 billion, M&T’s is $21.4 billion, and Huntington’s is $16.1 billion. Growth Source: Seeking Alpha Huntington and M&T grew year over year. And forecasts say both will do well next year. Truist didn’t grow YoY. But over the last five years, it had better average growth. Valuation Source: Seeking Alpha All three banks are cheap on a price-to-earnings basis. But Truist and M&T trade below book value (a company’s assets minus liabilities), which could be a better deal for investors. Of the three, Truist has the best price-to-cash-flow ratio. Profitability Source: Seeking Alpha Huntington had the best net income margin and return on equity. And even though it’s smaller, its cash flows were similar to M&T’s. Our Opinion 10/10 We expect TFC, HBAN, and MTB to survive and thrive. Each offers slightly different ways to play the sell-off in banks. Plus, they all have forward dividend yields over 4%, and in Truist’s case, 6%. Just let the dust settle for a few weeks before hopping into these names. To get content like this daily, sign up for The Spill for free here. |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |